Are you an agent in Portland and wonder why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Oregon’s 2026 rent cap is set at 9.5%. See the key details and implications of this policy for Portland metro rental valuations, property owners, and investment strategies.

The Oregon Department of Administrative Services (DAS) has released the official rent stabilization percentages for 2026, offering clarity for landlords, tenants, and housing professionals statewide. As a certified residential appraiser serving the Portland metro area, I track these updates closely because they influence rental market dynamics, which in turn affect property valuations for homeowners, lenders, realtors, estate planners, and attorneys.

This annual adjustment, governed by ORS 90.323 (maximum rent increase) and ORS 90.324 (calculation and publication), ensures rent increases align with inflation while offering predictability in a volatile housing market. Published on September 30, 2025, the announcement ties directly to the state’s rent control measures enacted to protect tenants from excessive hikes.

For most residential tenancies in the Portland region, the maximum allowable rent increase will be 9.5% starting January 1, 2026. This figure represents the lesser of 10% or 7% plus the Consumer Price Index for All Urban Consumers (CPI‑U) for the West Region, All Items, based on data from the previous 12 months. The calculation reflects a measured response to rising living costs, down slightly from the 10.0% cap in 2025.

Key Details on the 2026 Rent Cap

Understanding the nuances of this cap is essential for anyone involved in residential leasing or valuation in Oregon. The 9.5% limit applies broadly to tenancies under ORS 90.323, which covers most single‑family homes, apartments, and multifamily units in the region. Landlords must provide at least 90 days’ written notice for any increase up to this threshold, and the cap applies per 12-month period and increases may only be given once in any 12-month period.

Exemptions and special cases:

Smaller facilities (≤30 spaces): Manufactured dwelling parks or marinas follow the same formula—10% or 7% + CPI (9.5% in 2026).

Larger facilities (>30 spaces): Parks or marinas face a stricter 6% maximum increase under ORS 90.600.

Exclusions: New tenancies in the first year, fixed‑term leases without renewal, and exempt properties (e.g., subsidized housing). Utilities and fees may rise separately from base rent.

These provisions help maintain stability in the Portland metro area’s rental landscape, where median asking rents have hovered near $1,987 for a two‑bedroom unit according to RentCafe’s Portland rental market report (Nov 2025). Zillow places the overall average asking rent across unit types at $1,772 (Zillow Portland Rental Market; snapshot date 11/28/2025). Neighborhood‑level data shows two‑bedroom rents ranging from $1,800 to $2,400, underscoring the variability across the metro.

For appraisers, knowing the precise rent cap helps model the timeline required to bring a property or multifamily project back to market rents, especially when current leases are below prevailing rates. This allows for more accurate income projections.

Implications for Portland Metro Property Owners and Professionals

Homeowners: Must factor the 9.5% ceiling into rental conversion ROI, especially when evaluating single‑family properties for lease. The cap limits upside potential in a demand‑heavy market and affects long‑term income projections.

Realtors: Benefit from being able to project realistic rental growth figures in listings, particularly for multifamily properties (2+ units). The cap provides a clear ceiling for annual rent increases, which helps set buyer expectations and avoid overpromising future income.

Lenders: Gain greater clarity into a property’s income potential, allowing for more accurate underwriting and valuation.

Investors: Stay aligned with prevailing market rates while complying with legal pacing. For multifamily portfolios, knowing the exact rent cap helps plan staggered increases and avoid underperformance due to below-market rents.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Question: Do you think the annual cap will ever drop significantly, or will persistent inflation keep the annual increase at about 10%?

CODA

Are you an agent in Portland and wonder why appraisers always do “x”?

A homeowner with questions about multifamily income properties, GRMs, or income calculations?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

FHFA Q3 2025 HPI: U.S. +2.2% YoY, Oregon +0.31%, Portland MSA +1.51% — appraisal insights and practical implications for Portland appraisers and lenders.

National Overview & Oregon Statewide Performance

On November 25th, the Federal Housing Finance Agency (FHFA) released its Q3 2025 House Price Index (HPI). Nationally, home prices rose 0.2% quarter‑over‑quarter, and 2.2% year‑over‑year, reflecting a cooling but still positive trajectory across most regions.

Oregon posted +0.31% annual appreciation, ranking 45th nationally, with a –0.16% quarterly decline. These subdued figures mirror the broader West Coast trend: Washington registered +1.37% YoY, while California slipped –0.62% YoY. Oregon’s modest growth reflects a market in balance—neither surging nor contracting sharply.

Portland-Vancouver-Hillsboro MSA

In the “Purchase-only” FHFA index, the seven‑county Portland‑Vancouver‑Hillsboro MSA outperformed the statewide average slightly, recording +0.16% quarterly growth and +1.51% annual appreciation (” Seasonally Adjusted, Nominal” category). This MSA includes:

Oregon counties: Clackamas, Columbia, Multnomah, Washington, and Yamhill.

Washington counties: Clark and Skamania.

The inclusion of Clark County (Vancouver metro) is significant. Its size and activity often moderate or amplify Oregon‑centric trends, making the FHFA MSA lens broader than the Oregon‑only focus used in our local reporting.

In the “All-transactions” FHFA index, the values are similar but slightly different, recording -0.36% quarterly decline and +1.91% annual appreciation. This places the Portland‑Vancouver‑Hillsboro MSA 167th among all reporting MSAs.

Cumulative days on market up to 52 (a 13%+ increase).

Sales volume essentially unchanged.

The FHFA’s +1.51% YoY for the seven‑county MSA aligns directionally with this stability but reflects slightly stronger performance due to Clark County’s contribution. When Clark and Skamania are excluded, the Oregon counties track closely with our reported flat medians and lengthening market times.

Repeat-Sales Index: FHFA tracks the same property across multiple transactions to measure price changes over time.

Purchase Transactions: Use the sales price recorded in the mortgage data.

Refinance Transactions: Use the appraised value reported at the time of refinance (if an appraisal was ordered). Automated Valuation Models (AVMs) are not used.

Coverage: Only conforming conventional mortgages purchased or guaranteed by Fannie Mae and Freddie Mac are included.

New Construction: A new home enters the dataset when financed with a conforming mortgage, but it only contributes to the repeat-sales index once a second transaction occurs (sale or refinance).

This methodology ensures consistency and reliability, but it also means the index can lag in capturing brand‑new construction markets.

A Shoutout to Appraisers

Appraisers play a critical role in the FHFA dataset. Every time a refinance transaction includes an appraisal, that value becomes part of the HPI’s foundation. In other words:

Appraisal values anchor the index when no new sale price exists.

Consistency in appraisal practice ensures the HPI remains credible and defensible.

Local expertise matters: Appraisers’ ability to interpret market conditions, select comps, and apply adjustments directly influences the quality of the data feeding into national housing benchmarks.

Without appraisers, the FHFA’s “all‑transactions” index would be incomplete. Their work provides the bridge between raw market activity and standardized national reporting.

Appraisal Implications

Residential Valuations (1–4 Units):

Within Oregon counties, the FHFA’s +0.16% quarterly change supports only minimal positive time adjustments in paired‑sales analysis.

Of course, submarkets and particular neighborhoods may diverge from the broader trend. Appraisers must carefully define the competitive submarket for each property and measure market‑condition changes within that context.

Flat medians and longer days on market suggest no broad market‑condition adjustments are warranted for most single‑family assignments, but localized dynamics can still justify nuanced treatment.

Cross‑Border and Portfolio Work:

For assignments involving Clark or Skamania counties, or when lenders request regional context, the FHFA MSA index provides an authoritative benchmark.

The modest +1.51% annual growth reinforces conservative expectations for refinance, purchase, and estate‑planning valuations across the full seven‑county footprint.

Why This Matters

Homeowners, lenders, realtors, estate planners, and attorneys benefit from seeing both perspectives:

FHFA’s broader MSA view (slightly stronger due to Clark County)

Together, they provide a fuller picture of market stability and cross‑border dynamics in the Portland metro.

Frequently Asked Questions (FAQ)

What is the FHFA House Price Index (HPI)?

The FHFA HPI is a repeat‑sales index that measures changes in single‑family home values using data from Fannie Mae and Freddie Mac mortgages. It tracks the same property across multiple transactions to calculate price changes over time.

Does the HPI measure home prices directly?

No. The HPI does not report the median or average home price in dollars. Instead, it measures the percentage change in value between two transactions of the same property.

Example: If a home sold for $300,000 in 2015 and then $360,000 in 2025, the HPI records a 20% increase.

The index is built entirely from these changes, not from raw price levels. This makes the HPI excellent for tracking market movement, while MLS data is better for reporting actual price levels.

How does the repeat‑sales methodology work?

The index only includes properties with at least two transactions (purchase or refinance).

It measures the change in value between those two points, not the absolute level of prices.

This approach reduces noise from property differences and focuses on market movement.

What about new construction?

A new construction sale enters the dataset when financed with a conforming conventional mortgage.

However, it does not contribute to the repeat‑sales index until a subsequent transaction occurs (another sale or a refinance with an appraisal).

In other words, the first sale is logged, but the property only becomes “active” in the index once there’s a second data point.

What are the implications of this approach?

Coverage bias: The HPI does not immediately reflect brand‑new construction markets.

Lag effect: It takes time for new construction to show up in the index, often when owners refinance or resell.

Complementary data: FHFA also publishes purchase‑only indices (sales prices only) and expanded‑data indices (including FHA and county recorder data) to capture broader market activity.

Do refinances count in the FHFA HPI?

Yes. When a refinance includes an appraisal, the appraised value is used as the second transaction point. Automated Valuation Models (AVMs) are not used. This makes appraisers’ work central to the dataset.

Which counties are included in the Portland‑Vancouver‑Hillsboro MSA?

The FHFA defines the Portland MSA as seven counties:

This differs from our six‑county Oregon‑only focus, which includes Hood River but excludes Clark and Skamania.

How does FHFA data differ from RMLS or local MLS data?

FHFA data is based on conforming conventional mortgage transactions purchased or guaranteed by Fannie Mae and Freddie Mac. It provides a broad index of price changes, useful for regional benchmarking.

By contrast, RMLS (and other local MLS systems) reflect all listing and sales activity, regardless of financing type. This includes transactions financed with FHA, VA, jumbo loans, private financing, and even cash sales. RMLS also reports granular metrics such as median prices, days on market, and sales volume.

👉 In short: FHFA offers a standardized, mortgage‑based view of price movement, while RMLS captures the full spectrum of market activity, making it indispensable for appraisers and analysts who need transaction‑level detail.

Sources & Further Reading

FHFA House Price Index Quarterly Report 2025Q3 (full report)

For current market context on inventory and pricing trends in the Portland region, see our Q3 2025 Market Update.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Question: Do you think Q4 2025 will be flat in Oregon, or will see some significant price movement?

CODA

Are you an agent in Portland and wonder why appraisers always do “x”?

A homeowner with questions about appraisal contingencies, comp selection, or reconsiderations of value?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Oregon and eight other states filed a proposed $7M settlement with Greystar, affecting ~19,000 Portland apartments. Appraisers and buyers are watching for 2026 rent softening and cap rate shifts.

A coalition of nine states led by Oregon and California has filed a proposed $7 million settlement with Greystar Management Services — the nation’s largest rental housing operator — over allegations that Greystar used RealPage software to illegally coordinate rent pricing across competing properties.

The settlement, if approved by a federal court, would permanently bar Greystar from sharing non-public rent and occupancy data with competitors and from using RealPage’s hyper-local pricing recommendations. A separate DOJ consent decree filed against RealPage itself imposes similar behavioral restrictions and a three-year independent monitor.

Greystar manages approximately 19,000 apartment units in the Portland metro area — roughly 10 % of the region’s multifamily inventory. State investigators have estimated that RealPage-enabled pricing affected roughly one in five multifamily units statewide.

For homeowners, buyers, agents, and lenders, the most immediate question is whether these enforcement actions will translate into meaningful rent relief in 2026 and beyond.

The Direct Impact on Purchasing Power

A renter currently paying a $200 “algorithm premium” (the difference between market rent and coordinated rent loses $2,400 annually that could otherwise go toward a down payment.

Even a modest 5–8 % softening in rents after these settlements would return $110–$176 per month to the typical household, equating to $4,000–$10,600 in additional savings over three to five years.

What Appraisers Are Watching in 2026

Cap rate movement on institutional-grade (50+ unit) apartment buildings

Total scheduled gross revenue trends at properties previously managed with revenue-management software

If rents soften and risk premiums rise, cap rates will widen first on larger assets. That pressure eventually flows through to gross rent multipliers (GRMs) on 1–4 unit residential income properties — either compressing GRMs if sale prices adjust faster than rents, or temporarily expanding them if prices lag.

We likely won’t see clear signals until mid-2026, but the direction of travel will matter for every appraisal involving the income approach in the region.

Bottom Line

Combined with new multifamily supply now entering the pipeline, these twin enforcement actions represent the strongest downward pressure on algorithmic rent growth Portland has seen since the pandemic began.

Sources & Further Reading

Beaverton Valley Times coverage of the Greystar settlement

For broader quarterly context on inventory, pricing, and market segmentation trends in the Portland region, see our most recent Q3 2025 Market Update.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Question: Do you think we’ll see any meaningful slowdown in rent increases in the Portland area?

CODA

Are you an agent in Portland and wonder why appraisers always do “x”?

A homeowner with questions about appraisal contingencies, GRMs, or valuation delays?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

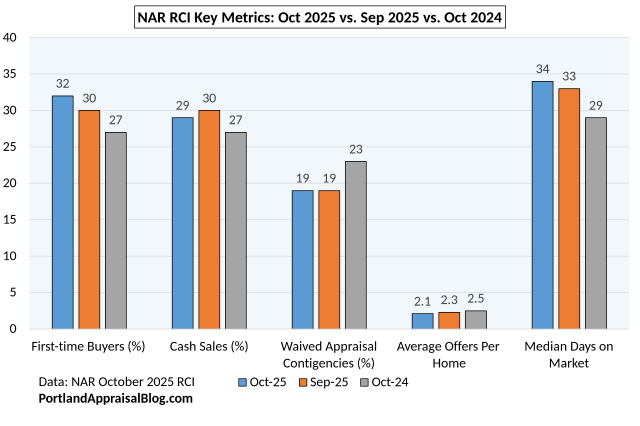

NAR October 2025 RCI: First-time buyers at 32%, DOM at 34 days, and 19% waived appraisals in Portland metro. Insights for realtors and homeowners on comp stability and market shifts.

The National Association of REALTORS® (NAR) has released its October 2025 REALTORS® Confidence Index (RCI), revealing a market with subtle shifts that Portland metro real estate professionals should monitor closely. First-time buyers climbed to 32% of transactions, supported by growing inventory and modestly lower rates, though overall confidence dipped—with only 17% of REALTORS® expecting year-over-year buyer traffic increases in the next three months, and 16% for sellers. Cash sales remained steady at 29%, while homes received an average of 2.1 offers, and 19% sold above list price.

For appraisers in the Portland area, these trends suggest more stable comparable sales (comps), but they also highlight persistent risks from contingencies, with 19% of buyers waiving appraisals and 6% of delayed settlements linked to valuation issues. This creates opportunities for thorough, defensible reports that address local market segmentation.

The RCI: A National Pulse with Local Relevance

The RCI draws from a survey of approximately 1,800 REALTORS® conducted November 1–16, 2025, focusing on buyer and seller activity, financing, contingencies, and sentiment. Unlike local MLS data such as RMLS, which tracks completed transactions, the RCI captures forward-looking expectations. In the Portland metro, including Vancouver, WA, combining these insights ensures appraisals reflect both anticipated trends and on-the-ground realities, particularly in cross-border markets.

Key Market Indicators Shaping Appraisals

October’s data points to a gradual easing:

Median Days on Market (DOM): 34 days (up from 33 in September 2025 and 29 in October 2024).

First-Time Buyers: 32% of transactions (up from 30% in September 2025 and 27% in October 2024), signaling stronger entry-level demand.

Cash Sales: 29% (down slightly from 30% in September 2025, up from 27% in October 2024).

Distressed Sales: 2% (unchanged from prior months).

While days on market are up year over year, the time homes are spending on market is not excessive. There is a bit more time for negotiations. I go into detail about rising days on market in my Portland Region Q3 2025 Market Update.

Buyer Shifts and Contingency Considerations

Buyers are navigating a slightly less competitive landscape, which influences appraisal timelines and risks:

20% waived inspection contingencies (flat from September 2025).

19% waived appraisal contingencies (flat from September 2025, down from 23% in October 2024)—a trend that eases renegotiation pressures for Portland appraisers.

5% completed purchases via virtual tours only (unchanged).

82% of purchases occurred in suburban, small town, rural, or resort areas (down from 87% in September 2025).

In Multnomah County and Vancouver, WA, this suburban preference reshapes comp pools, emphasizing the need for carefully defined competitive areas—location matters!

Seller Dynamics: Fewer Offers, More Scrutiny

Sellers are adjusting to softer demand, with implications for pricing and close processes:

Average offers per home: 2.1 (down from 2.3 in September 2025 and 2.5 in October 2024).

19% sold above list price (down from 21% in September 2025, flat from October 2024).

2% sold to iBuyers (up from 1% in September 2025).

Median time to close: 30 days (unchanged).

7% of contracts terminated (up from 6% in September 2025).

14% experienced delayed settlements (unchanged).

For realtors and lenders in the Portland metro, rising terminations underscore the importance of appraisals backed by solid, verifiable comps. As I detailed in my Portland Region Q3 2025 Market Update, the sales price to original list price ratio has been declining.

Outlook: Tempered Optimism and Suburban Focus

REALTOR® confidence softened amid these changes:

17% anticipate buyer traffic growth year over year in the next three months (down from 20% in September 2025).

16% expect seller traffic increases (down from 19% in September 2025).

29% of buyers prioritized work-from-home features (down from 34% in September 2025).

This aligns with the Portland Region’s ongoing suburban migration, impacting comp selection in Clackamas and Washington Counties. Homeowners and attorneys preparing for transactions should carefully read reports to verify they incorporate these broader sentiment shifts.

Implications for Portland Metro Valuations

The RCI’s blend of buyer gains and fading enthusiasm points to a transitional market: enhanced first-time activity promotes equitable pricing, but elevated terminations (7%) reveal gaps in expectations. For further details, explore the full report here, the main RCI page, or the existing-home sales tie-in. See also my Portland Region Q3 2025 Market Update.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Question: Do you think lower mortgage rates will propel the market to new heights?

CODA

Are you an agent in Portland or Clackamas County and wonder why appraisers always do “x”?

A homeowner in Lake Oswego with questions about appraisal contingencies or valuation delays?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or Clackamas County, we’d be glad to assist.