Real Estate Appraisal Blog Covering the Residential Market in Portland, Oregon & Surrounding Areas

Author: Abdur Abdul-Malik, SRA, ASA

Certified residential appraiser licensed in Oregon and Washington, serving the Portland and Vancouver areas. I extensively serve—and blog about—Clackamas, Columbia, Hood River, Multnomah, Washington, and Yamhill counties in Oregon, as well as Clark, Cowlitz, Klickitat, and Skamania counties in Washington.

Portland’s Home‑Sharing Pilot pays homeowners $200/week to rent spare bedrooms, but appraisers see a valuation blind spot: the income is real to owners yet largely invisible to lenders, GSEs, FHA, and most VA underwriting.

A classic pre-1940 home in the Portland region—the type of property often structurally suited for multi-room sharing arrangements. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Portland’s Quiet Experiment: Turning Spare Rooms into Distributed SROs

Portland is running a quiet housing experiment in 2026, and it requires no new construction, no zoning fights, and no multimillion‑dollar bond measures. The city is simply trying to activate something already sitting inside thousands of local homes: the spare bedrooms.

Launched in February 2026, the Portland Home‑Sharing Pilot Program offers owner‑occupants a one‑time grant—$1,000 for the first room and $500 for each additional room—to make at least one bedroom available for rent at a capped rate of $200 per week, utilities included. Homeowners must live on site, commit to keeping the room(s) available for 12 months, and work through approved providers (currently PadSplit and Ecumenical Ministries of Oregon). Rooms must meet basic habitability standards under ORS 90.320 and be registered under Portland’s Rental Registration Program. Because the tenant must live inside the same dwelling unit as the homeowner, renters share the home’s kitchen and bathroom facilities in virtually all cases.

This is not short‑term rental housing like Airbnb, nor is it a traditional apartment or ADU. It is something different: an informal, distributed form of single‑room occupancy (SRO) housing.

Oregon’s 2023 statewide SRO legalization (ORS 197A.430) laid the legal groundwork. The pilot operationalizes the same concept—private rooms with shared facilities—without requiring new buildings. A purpose‑built SRO like the Alder House in the Pearl District features small private rooms, shared kitchens and baths, and centralized management. The pilot recreates that basic form, but scatters it across hundreds of existing single‑family homes.

The Sam Galbreath Alder House in Portland’s Pearl District—a purpose-built single-room occupancy (SRO) building featuring centralized management and shared facilities. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Portland’s housing stock is unusually well‑suited for this model. Many early‑1900s homes contain four, five, or six bedrooms spread across three levels, often with basements that provide natural separation between owner and boarder. Few West Coast cities of similar size have this volume of large, compartmentalized older homes, and that architectural quirk gives the pilot room to function.

Portland is joining a growing list of cities experimenting with room‑rental models as a tool for housing availability. The logic is pragmatic: constructing new deeply affordable units is slow and expensive, while spare bedrooms represent low‑cost “latent capacity.” By requiring owner occupancy, rent caps, and habitability checks, the city hopes to expand housing options without fostering unsafe or absentee‑landlord situations.

It is a creative policy experiment. Yet turning spare rooms into housing supply is not the same as convincing homeowners to participate. The economics, risks, and valuation implications are substantial—and that is where the story becomes especially relevant for appraisers.

Why Homeowners Might Hesitate: Practical, Financial, and Interpersonal Friction

If unlocking spare bedrooms were simply a matter of latent capacity, participation would be straightforward. In reality, those bedrooms sit inside someone’s primary residence. Converting them into rental space introduces proximity, financial, and lifestyle trade‑offs that most homeowners have never faced.

Unlike renting a self‑contained ADU or a fully independent basement apartment, this arrangement means sharing circulation paths, noise, kitchen, and bathroom facilities with a stranger. Even in large early‑1900s Portland homes with three levels and partial separation, daily life overlaps—cooking smells, laundry schedules, late‑night activity, and visitors. For many households, the loss of privacy and control is a significant deterrent.

Financially, the upside is modest. The program caps rent at $200 per week—about $867 per month or $10,400 per year. After increased wear‑and‑tear, higher utility costs, management time, and potential vacancy between tenants, net income for a single room often falls to $500–$650 per month. The one‑time grant ($1,000 for the first room, $500 thereafter) helps with setup but does little for the long‑term picture. Only when homeowners rent multiple rooms does the supplemental income become more meaningful—and at that point, the arrangement begins to resemble a small, owner‑occupied micro‑SRO with all the operational complexity that implies.

A commenter in Willamette Week’s coverage of the pilot captured the prevailing sentiment:

“The potential economic liabilities of participating in this program far outweigh the economic benefits.”

Many Portland homes already use their bedrooms intensively—for children, multigenerational living, home offices, or simply as flexible guest space. A “spare” bedroom is not always functionally spare. Adding a tenant can disrupt household dynamics in ways that are difficult to quantify.

These frictions matter beyond participation rates. They directly influence how appraisers evaluate highest and best use, potential functional obsolescence from increased wear or altered circulation, and long‑term marketability. A home that operates comfortably with one or two boarders may appeal to a narrower pool of future buyers, even if the rental income itself is largely ignored in the appraisal.

The pilot’s success will ultimately hinge on whether enough homeowners decide the trade‑offs are worth it. For appraisers and market participants, that uncertainty is precisely what makes the program worth watching.

Structural Capacity vs. Market Reality

While the previous section outlined why many homeowners may hesitate, the pilot’s very existence rests on a simple fact: Portland’s detached housing stock contains an unusually high number of homes that are structurally well‑suited for room‑rental arrangements. The city’s early‑1900s building patterns, three‑level layouts, and prevalence of basements create a natural foundation for shared‑housing models—at least on paper.

Bedroom Distribution: Portland Has More Large Homes Than People Assume

Detached home sales in 2025 skewed larger than many expect. Nearly 36% of sales had four or more bedrooms, and almost 10% had five or more—precisely the segment most compatible with renting multiple rooms. Since the pilot’s economics only begin to feel meaningful when a homeowner rents two or more bedrooms, this upper tier of the housing stock is where most of the structural feasibility lives.

Bedrooms

No. Sales

% of Total

2 BR

957

17.2%

3 BR

2,580

46.3%

4 BR

1,466

26.3%

5 BR

430

7.7%

6+ BR

87

1.6%

Note: Figures are based on all Multnomah County sales with a Portland city address that sold on the open market in 2025. There were a total of 5,570 sales in 2025. Single-Family Detached Residential | 2025 Data: RMLS | PortlandAppraisalBlog.com

These larger homes are the natural candidates for the pilot’s model. A homeowner with four, five, or six bedrooms has the physical inventory to rent multiple rooms without displacing household needs—a key distinction from smaller homes where “spare” bedrooms are often functionally occupied.

Basements and Separation: Where Feasibility Improves

Basements are not required for participation, but they meaningfully reduce friction. They create partial separation, allow quieter circulation, and soften the proximity concerns described earlier. Portland’s older housing stock delivers here as well: basement prevalence rises sharply with bedroom count.

For appraisers, this matters because basements influence functional utility. A compartmentalized three‑level home with a basement offers natural circulation paths that can reduce (but not eliminate) the friction of shared living. At the same time, these same layouts can signal potential functional obsolescence if the home is modified for multiple tenants—keyed bedroom doors, partitioned spaces, mini‑fridges, or heavier wear patterns that diverge from typical single‑family use.

Structural Capacity Does Not Equal Market Acceptance

Portland’s early‑1900s Craftsman, Foursquare, and bungalow stock—with its compartmentalized floor plans rather than open‑concept designs—creates more “latent capacity” for distributed SRO‑style use than is typical in newer, ranch‑heavy suburbs. But structural suitability is only half the equation. A home that functions well for an owner with two or three boarders may appeal to a narrower pool of future buyers, affecting marketability, comparable selection, and the interpretation of contributory value.

This is where the appraisal lens becomes essential. The housing stock provides the physical opportunity, but the market ultimately determines whether that opportunity translates into value, neutrality, or even a discount.

In short, Portland has the physical inventory. The real question—and the one that matters most for appraisers—is how the market treats homes that participate in the pilot. That requires looking beyond structural feasibility and into the valuation mechanics: GRMs, Fannie Mae’s treatment of boarder income, highest and best use, and the limits of value‑in‑use.

That’s where the next section picks up.

The Valuation Blind Spot: Why Room‑Rental Income Rarely Translates Into Market Value

At first glance, the valuation question appears straightforward: if a homeowner rents out one or more bedrooms in their primary residence under the pilot, does the property become an income‑producing asset? Under conventional GSE guidelines and most VA loans, the answer is generally no. FHA is more flexible, but even there the income must be well‑documented and capped. For the overwhelming majority of transactions, the income generated is treated as value‑in‑use for the current owner rather than market value recognizable by buyers and lenders. That distinction is fundamental.

Why the Income Approach Does Not Apply

The pilot’s temporary 12‑month structure alone prevents capitalization. GRM or income‑approach analysis requires a revenue stream that is durable, predictable, and market‑supported. A pilot program—by definition experimental—does not meet that test. Even if the income were otherwise eligible, appraisers cannot assume it will continue beyond the pilot window.

Fannie Mae’s Selling Guide (B3‑3.8‑01) is clear: “generally, rental income from the borrower’s principal residence…cannot be used to qualify the borrower,” and any qualifying rental income must come from a unit that is separate from the primary residence. A bedroom does not meet that standard—it lacks independent living facilities, so the income it produces is not considered rental income for qualifying or valuation purposes. Limited exceptions exist, such as boarder income with a documented 12‑month history or rental income from a true ADU, but neither applies to a bedroom within the primary dwelling.

Freddie Mac’s guidance (Section 5306.1) follows the same logic. Room‑rental income inside the primary residence is treated as boarder income and is ineligible for qualification except under narrow Home Possible exceptions, which cap boarder income at 30% of qualifying income with a 12‑month history.

FHA is more flexible. Mortgagee Letter 2025‑04 allows boarder income with a 12‑month history (at least 9 of the most recent 12 months documented), capped at 30% of effective income, and supported by bank statements, canceled checks, tax returns, shared‑address documentation, and a written agreement. Even so, the income must be stable, well‑documented, and clearly likely to continue.

VA’s treatment is similarly restrictive, though for different reasons. VA does allow temporary boarder income, but only with two years of signed tax returns showing the income, and only when the rental does not impair the residential character of the property or exceed 25% of the total floor area. The underwriter must also determine that the income has a reasonable likelihood of continued success and justify its inclusion on VA Form 26‑6393. In practice, residual‑income requirements and lender overlays mean many VA lenders exclude boarder income entirely unless it has a long, well‑documented history.

Across all major lending frameworks, the conclusion is consistent: room‑rental income under this pilot is not considered stable rental income. It cannot be capitalized, and it carries no weight in the income approach.

Highest and Best Use Implications

For the vast majority of participating homes, highest and best use remains single‑family residential. Renting bedrooms may provide supplemental cash flow for the current owner, but it does not create a new, financially feasible use that changes the legally permissible or maximally productive use of the property.

There are limited exceptions at the margins. In transitional RM1–RM2 zones—where older single‑family homes sit on land with redevelopment potential—stable boarder income could theoretically support an interim highest and best use if the program persists beyond the pilot window. For aging owners, modest supplemental income may extend the economic life of a marginal property. These situations remain rare and highly property‑specific.

Functional Utility and Marketability

Shared‑living arrangements can also affect functional utility. Homes with multiple boarders frequently show keyed bedroom doors, partitioned spaces, additional refrigerators or mini‑kitchens, heavier wear on shared bathrooms, and circulation patterns that feel more communal than private. While most modifications are reversible, they introduce functional obsolescence relative to typical single‑family buyers and often require additional expense or concessions to restore the home to standard configuration.

Marketability can suffer in subtler ways: more vehicles, increased activity, reduced privacy, and access issues during showings. Sellers may also need to vacate the home before listing, and because these occupants are tenants—not ADU tenants, but tenants under Portland’s relocation‑assistance rules—relocation payments may be required. We covered these rules in detail in our November 2025 post on Portland’s tenant protections.

True SRO vs. Distributed Room Rental

Some homeowners may perceive their property as operating like a micro‑SRO, especially when renting two or three rooms. The comparison does not hold for valuation purposes. Legitimate SROs feature separate leases, independent facilities, and regulatory treatment as income properties. A single‑family home with rented bedrooms may have partial separation—some SFRs do have ADU‑like lower levels with their own kitchens, bathrooms, and entrances—but unless the space meets the definition of a separate dwelling unit, the market continues to value it as a standard single‑family residence.

Bottom Line for Appraisers

The income is real to the participating owner, and in isolated cases a niche buyer may pay a modest premium to continue the arrangement. Unpermitted SRO‑style use already exists quietly in some Portland neighborhoods. If the pilot persists and scales, subtle patterns may eventually emerge in comp selection or marketability adjustments.

Under current rules and market evidence, however, room‑rental income from this program does not contribute meaningfully to market value in typical single‑family transactions. For appraisers, the real blind spot is not ambiguity in the guidelines—it is the gap between public perception and how the lending and valuation system actually treats these arrangements.

Portland’s “Noodles on the Wall” Housing Strategy

The Home‑Sharing Pilot is not an isolated policy experiment. It is one piece of Portland’s broader pattern of trying every available tool to address a persistent housing shortage—from large‑scale capital projects to low‑cost, homeowner‑driven solutions.

The city’s current approach runs on two distinct tracks. The first is the traditional capital‑intensive path: supportive housing, regulated affordable multifamily developments, and publicly funded projects that require years of entitlement, bonding, and construction. These are essential but slow and expensive. The second track is distributed and incremental—ADUs, accessory conversions, and programs like home‑sharing that seek to activate capacity already embedded in the existing housing stock. These approaches rely heavily on voluntary homeowner participation and can scale more quickly when incentives align.

The pilot clearly belongs to the second track. It is inexpensive to launch, fast to implement, and attractive because it demonstrates action without massive upfront capital. Yet its success hinges on the same variable that has challenged similar distributed efforts in Portland: homeowner willingness. ADUs took years of code changes, fee reductions, and cultural normalization before meaningful uptake occurred. Inviting a vetted tenant into one’s primary residence through a city program may require an even larger shift in comfort and risk tolerance.

From an appraisal perspective, this dual‑track reality intersects with a deeper structural issue. Portland’s affordability constraints remain severe. The latest Portland Appraisal Blog Affordability Index (PABAI) reading for detached homes stands at 79.2—firmly in the “severely constrained” range. Median‑income households cannot qualify for the typical detached home under standard lending assumptions, so they remain renters longer. That downstream pressure tightens the rental market for the very individuals the home‑sharing pilot hopes to serve as tenants.

Even if participation grows, the valuation and lending system largely ignores the resulting room‑rental income. As detailed earlier, GSE guidelines, FHA flexibilities, and VA restrictions treat most boarder income as non‑qualifying or incidental. This disconnect means the pilot may expand functional housing supply without meaningfully affecting how properties are financed or valued in the marketplace.

Whether the pilot becomes a meaningful contributor to supply or remains a modest experiment will ultimately depend on participation rates, program durability, and homeowner comfort with shared‑living arrangements. For appraisers, the real takeaway is not the program’s potential scale, but what it reveals about the limits of distributed solutions in a market where income from spare bedrooms still does not reliably translate into recognized market value.

Readers interested in how this fits into Portland’s larger affordability efforts can explore our ongoing series on affordable housing and related policy shifts.

Conclusion

Portland deserves credit for experimentation. The Home‑Sharing Pilot represents a low‑cost, low‑friction attempt to activate latent capacity already embedded in the city’s existing housing stock. At the individual level, it may create workable arrangements for both homeowners and renters while revealing how people actually use their homes under sustained affordability pressure.

Yet the pilot also underscores a structural reality that appraisers see every day: the valuation and lending system ultimately sets the practical ceiling for distributed housing solutions. Room‑rental income inside a primary residence is not treated as qualifying rental income by Fannie Mae, Freddie Mac, FHA, or most VA lenders. The result is a meaningful disconnect—the program can improve lived experience for participants without materially changing how properties are financed, underwritten, or valued in the marketplace.

Whether home‑sharing evolves into a meaningful contributor to supply or remains a modest, low‑uptake experiment will depend on participation rates, program durability, and broader cultural comfort with shared‑living arrangements. For appraisers and market participants, the key takeaway is straightforward: watch closely how—and if—these arrangements begin appearing in listings, seller disclosures, and comparable sales. The policy may change over time, but the valuation framework will continue to define its real‑world impact.

Sources & Further Reading

City of Portland Launches Home Sharing Pilot Program: Announcement

Portland Affordability Index – PABAI: A Realistic Housing Qualification Metric for the Portland Region: Portland Appraisal Blog

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

The Strong Family Apartments transform an underutilized 0.96‑acre site into 75 long‑term affordable family units in Humboldt. With plottage‑enabled density, CM2 zoning, and a 99‑year covenant, the project fills a critical gap in a corridor where only 1%–3% of recent sales were affordable to 60% AMI households.

The Strong Family Apartments at N Alberta St & N Williams Ave in Humboldt, viewed from the intersection. The 4-story building maximizes the assembled 0.96-acre site for 75 restricted affordable family units. Photo: Abdur Abdul-Malik (March 2026), Portland Appraisal Blog

The Strong Family Apartments rise at the corner of N Alberta Street and N Williams Avenue in North Portland’s Humboldt neighborhood—a site long held by the Strong family, whose roots reflect the deep history of Black homeownership and community life in N/NE Portland. For decades, the property remained a modest home surrounded by open grassy land across multiple tax lots. In 2019, the Portland Housing Bureau acquired the site for land banking, and in 2024 transferred title to Strong AA Limited Partnership—a partnership led by Community Development Partners and Self Enhancement, Inc.—to deliver a 75‑unit affordable multifamily community.

True to the project’s name, the development is intentionally family‑oriented and contains no studios. The unit mix includes 21 one‑bedrooms, 32 two‑bedrooms, and 22 three‑bedrooms, with rents restricted at 30% and 60% of area median income. Eleven units are deeply affordable at ≤30% AMI, and the project prioritizes the City’s N/NE Preference Policy for households displaced by past urban renewal and gentrification in North and Northeast Portland. With 54 family‑sized units, the building fills a gap in a neighborhood where market‑rate options have become increasingly out of reach for moderate‑income families.

From an appraisal perspective, the site tells a clear story. Assemblage of multiple parcels into a unified 0.96‑acre lot unlocked plottage value and enabled a highest‑and‑best‑use shift to family‑oriented multifamily housing in the CM2 zone—a designation with no parking minimums and incentives for dense, transit‑supported development along key corridors. The redevelopment transforms a historically underutilized corner into a long‑term community asset governed by a 99‑year affordability agreement.

This post examines the project through that lens: how zoning, public‑private tools, and assemblage shaped feasibility; how restricted‑use valuation differs from market‑rate ownership in Humboldt; and what the Strong Family Apartments reveal about affordability, displacement, and redevelopment in Portland’s evolving N/NE housing landscape.

Site History, Project Details & Zoning

The Strong Family Apartments occupy a prominent corner at N Alberta Street and N Williams Avenue in North Portland’s Humboldt neighborhood. For decades, the property remained under long‑term ownership by the Strong family, whose generational roots reflect the deep history of Black families in N/NE Portland. Prior to redevelopment, the site consisted of multiple smaller tax lots totaling nearly one acre, largely underutilized as open grassy land surrounding a modest single‑family home—clearly visible in 2019 archival Street View and aerial imagery. In CM2 zoning, a medium‑scale commercial mixed‑use designation intended for transit‑served corridors, a single‑family home on such a large combined parcel represented significant underutilization. The zone supports mid‑rise multifamily buildings rather than detached homes, with no parking minimums and height allowances of 45 feet (up to 75 feet with bonuses).

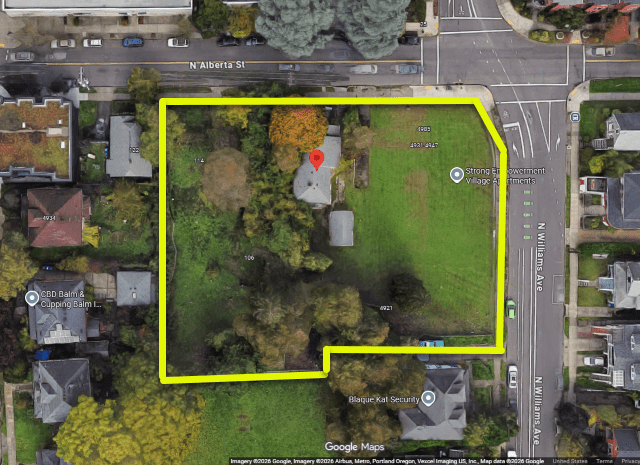

Archival Google Street View from July 2019 showing the site prior to redevelopment: a modest home surrounded by open grassy land across multiple tax lots. Source: Google Street ViewAerial view of the Strong Family Apartments site pre-redevelopment, with the yellow outline highlighting the approximate assembled 0.96-acre footprint across multiple tax lots. The modest home and open grassy areas were underutilized prior to unification, enabling the shift to highest and best use as 75 family affordable units. Source: Google Maps

In 2019, the Strong family privately sold the property to the Portland Housing Bureau (PHB) for land banking, bypassing any open‑market listing. This acquisition aligned with PHB’s strategy to preserve sites for community‑benefit affordable housing in historically impacted N/NE neighborhoods. The property remained in land bank status until 2024, when City Council Ordinance 191817 authorized transfer of the site to Strong AA Limited Partnership, a private ownership entity formed by Community Development Partners (CDP), the project’s developer, and Self Enhancement, Inc. (SEI), the nonprofit service partner. In this structure, an SEI affiliate serves as the Managing General Partner, a CDP affiliate serves as the Administrative General Partner, and a private tax‑credit investor holds the Limited Partner interest (approximately 99.99%). This arrangement is typical for Low‑Income Housing Tax Credit (LIHTC) developments, the federal program that finances most affordable rental housing in the United States. Under LIHTC, private investors receive a dollar‑for‑dollar reduction in federal tax liability in exchange for investing equity into qualified affordable housing projects, which allows units to rent below market rates. In this structure, the investor provides equity, Community Development Partners oversees development and compliance, and Self Enhancement, Inc. leads resident services and long‑term community engagement.

The project’s financing layers reflect the complexity typical of affordable multifamily development. Approximately $14.2 million came from PHB (including a $11.4 million cash-flow share loan from the 2023 Metro Housing Bond allocation and Interstate Corridor Urban Renewal Area tax-increment financing), supplemented by Portland Clean Energy Fund grants, Oregon Housing and Community Services low-income housing tax credits, and additional contributions. The development remains privately owned and operated, with Guardian Management overseeing leasing and SEI providing resident services. A 99‑year regulatory agreement with PHB mandates long‑term affordability, adherence to the N/NE Preference Policy, and other public‑benefit requirements.

The development delivers 75 rental units across one‑, two‑, and three‑bedroom floor plans, with all rents restricted for households earning 30% or 60% of area median income (AMI). Eleven units are deeply affordable at ≤30% AMI, prioritizing families with the highest need. The table below summarizes the mix and representative rent levels.

Bedrooms

Number of Units

AMI Level

Estimated Rent Range

1 Bedroom

21

≤30% and ≤60% AMI

~$656 (30% AMI 1BR example)

2 Bedroom

32

≤30% and ≤60% AMI

~$1,195–$1,215 (45% AMI 2BR example)

3 Bedroom

22

≤30% and ≤60% AMI

~$905 (30% AMI 3BR example)

Rents are not subsidized (no project‑based vouchers); residents pay the full restricted amount plus electricity, while the landlord covers water and trash. The mix emphasizes family households, with the N/NE Preference Policy prioritizing those displaced from the area.

Amenities include a large central courtyard with a private playground and nature‑inspired play features, indoor bike parking and storage, on‑site laundry, a community room and kitchen, and resident services focused on youth education, employment support, and family stability. The building targets Earth Advantage Platinum certification for energy efficiency, solar readiness, and a tight building envelope.

Central courtyard during final construction, prepped for family playground and nature play features. Photo: Abdur Abdul-Malik (March 2026), Portland Appraisal Blog

Construction began in late 2024 after financing closed in August 2024. Completion is expected in Spring 2026, with leasing to follow. The timeline—from 2019 acquisition through multiple funding layers, permitting, and construction—reflects the typical duration and complexity of affordable multifamily development in Portland.

The CM2 zoning directly supported the site’s highest and best use. Multifamily residential is a primary permitted use on transit‑served corridors, with no parking requirement and incentives for density. Assemblage of the multiple lots into a single 0.96‑acre parcel enabled the scale, layout, and family‑oriented amenities that a single‑family home on fragmented parcels could never achieve.

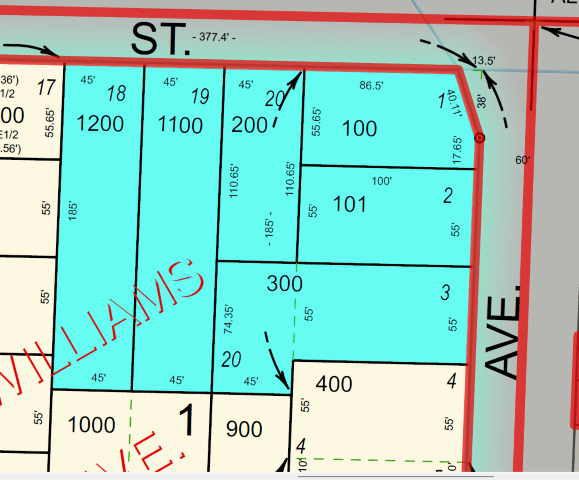

Portland Maps tax lot overlay showing the multiple original parcels assembled into a single 0.96‑acre unified lot. The combined footprint that enabled density and family amenities. Source: Portland Maps

Humboldt is a compact, vibrant inner North/Northeast Portland neighborhood centered around the Alberta–Williams corridor. With a Walk Score of 89 (“Very Walkable”) and a Bike Score of 100 (“Biker’s Paradise”), most daily needs can be met on foot or by bike, supported by a Transit Score of 53 and frequent bus service along N Williams, N Vancouver, and N Killingsworth, plus proximity to the MAX Yellow Line. The area blends long‑standing community roots with ongoing revitalization, anchored by the Alberta Arts District’s murals, galleries, indie shops, cafés, restaurants, and the long‑running Last Thursday street events.

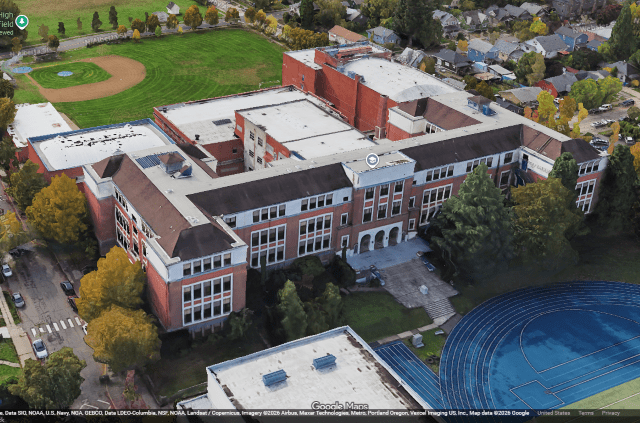

Education and youth resources form a strong neighborhood backbone. Jefferson High School—with its full‑size football field, track, and community programming—sits within Humboldt boundaries and is walkable or bikeable from the Strong site. Nearby KairosPDX, a public charter school focused on culturally responsive education, and Portland Community College Cascade, just north of the neighborhood, add depth through early‑learning programs, K–8 support, and college‑level career and transfer pathways. Together, these institutions reinforce the project’s family‑oriented design and align with the N/NE Preference Policy’s emphasis on retaining generational ties for households with a historical connection to the area.

Jefferson High School in the Humboldt neighborhood, shown with its athletic fields and campus layout as seen in Google Earth. The school sits within walking and biking distance of the Strong Family Apartments. Source: Google MapsKairosPDX, a public charter school in Humboldt, serves as a key family and education resource. Its proximity to the Strong Family Apartments supports the project’s family‑oriented design and 54 two‑ and three‑bedroom units, providing walkable access for residents with children. Photo: Abdur Abdul-Malik (March 2026), Portland Appraisal Blog

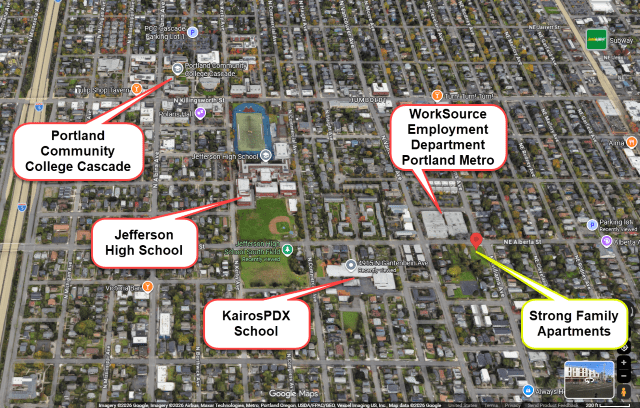

Employment access is unusually strong for a neighborhood‑scale project. The WorkSource Oregon center (State of Oregon Employment Department Portland Metro office) sits directly across N Williams Avenue from the Strong site. The facility provides job search assistance, training referrals, career counseling, unemployment support, and connections to workforce programs—resources that complement SEI’s on‑site youth and employment services and enhance the project’s location externalities for income‑restricted families.

WorkSource Oregon center (State of Oregon Employment Department facility) directly across N Williams Avenue from the Strong Family Apartments site. This proximity to state‑supported job search, training, and employment resources enhances location externalities for residents, particularly families prioritized under the N/NE Preference Policy. Photo: Abdur Abdul-Malik (March 2026), Portland Appraisal Blog

Grocery access is a modest tradeoff. Unlike some recent Portland affordable developments with immediate adjacency to major grocers (e.g., Trader Joe’s at HollywoodHUB or Safeway at Barbur Apartments), Humboldt lacks a full‑service chain supermarket within its boundaries or within a short walk of the Strong site. The nearest practical options are New Seasons Market on N Williams Avenue (~0.8 miles south, 15–20 minute walk or 5-minute bike ride along protected lanes) and Safeway (~0.8 miles northeast). Delivery services (Instacart, New Seasons own platform, etc.) are widely available, and insulated bags, cargo bikes, or e-assist options mitigate summer heat or load-carrying challenges. The Safeway route involves crossing the major arterial NE Martin Luther King Jr Blvd, making it less preferable for walking. This pattern aligns with the corridor’s multimodal design and the project’s minimal parking program (15 EV-ready shared spaces).

The neighborhood reflects a long history of community change, with significant gentrification pressures, a high renter share (49% per the City of Portland’s 2023 neighborhood demographic profile), and rising ownership costs. These dynamics underscore the importance of restricted affordable family housing in a corridor where market‑rate ownership has become increasingly out of reach for moderate‑income households.

Labeled aerial map (Google Maps) of the Strong Family Apartments site (red pin) and surrounding Humboldt neighborhood amenities. Key resources include WorkSource Oregon, Jefferson High School, KairosPDX, and Portland Community College Cascade—all within a short walk or bike ride. This cluster strengthens the project’s location advantages for income‑restricted families. Source: Google Maps

Data & Analysis — Humboldt’s Owned Market in Contrast

Understanding the context for the Strong Family Apartments requires examining Humboldt’s recent open‑market ownership landscape. This analysis uses RMLS data for 1–3 bedroom SFR‑class transactions (detached, condo, and attached) from 2024 through year‑to‑date 2026—the period that best reflects current market conditions. All figures represent descriptive statistics from the full set of qualifying sales; no sampling or modeling is involved.

The Portland Appraisal Blog Affordability Index (PABAI) measures how the average home close price compares to what a household at a given income level can qualify for under standard lending assumptions (HUD median MSA income, 20% down payment, and a 28% debt‑to‑income ratio for principal, interest, taxes, and insurance). A PABAI of 100 means the market is exactly affordable at that income level (current HUD median MSA income is $124,100 for a family of four in the Portland metro area) . Values above 100 indicate excess qualifying capacity (more affordable), while values below 100 indicate a shortfall (strained affordability). Full methodology and the interpretation scale are available on the PABAI explainer page.

PABAI Range

Interpretation

120+

Strongly Affordable

100–119

Moderately Affordable

80–99

Strained

Below 80

Severely Constrained

The PABAI is recalibrated here to a 60% AMI benchmark ($74,460 maximum income for a four‑person household), aligning with the majority of Strong’s units.

Humboldt 1–3 Bedroom Sales by Property Type (60% AMI Benchmark)

Property Type

Avg Beds

Avg Close Price

Avg PABAI (60% AMI)

Affordable Sales (out of total)

Detached

2.74

$533,738

55.20

0 / 38

Condo

1.98

$387,939

70.28

1 / 49*

Attached

2.57

$488,357

56.97

0 / 7

*Note: Including 0‑bedroom studio condos (outside the 1–3 bedroom focus) adds two additional qualifying sales, bringing the total to three affordable transactions across the full condo dataset. All three were small 0–1 bedroom units (381–510 SF, no garages, prices $165,000–$237,999). No qualifying sales occurred in any 2–3 bedroom units across any property type.

Detached Homes: The Traditional Family Segment

Detached homes—typically older (average build year 1940), larger (1,933 SF average), and more likely to include garages (0.61 average spaces)—represent the traditional family‑oriented housing stock most comparable to Strong’s 2–3 bedroom units. In this segment, the PABAI falls to a severely constrained 55.20, with zero of the 38 transactions qualifying as affordable for a 60% AMI household. This reflects the substantial income gap required to purchase family‑sized homes in Humboldt under standard qualification criteria.

Condos: Relatively Less Constrained, but Not for Families

Newer condos (average build year 2010, 1,006 SF average, minimal garage access) show a higher average PABAI of 70.28, indicating somewhat less affordability pressure relative to detached homes. However, the coverage is extremely limited: only one qualifying sale in the 1–3 bedroom range, plus two additional qualifying studio units when the dataset is expanded. All three affordable transactions were 0–1 bedroom units—none were family‑sized.

Attached Homes: Low Volume, Same Constraints

The attached segment contains only seven transactions, which reflects the full universe of attached 1–3 bedroom sales in Humboldt during this period. While the volume is low, these are all open‑market transactions, and the affordability pattern mirrors the broader constraints seen in the detached and condo segments. The average PABAI of 56.97 and zero qualifying sales reinforce the limited feasibility of ownership for 60% AMI households in this format.

Affordability Coverage and Market Implications

Across the full set of 94 open‑market 1–3 bedroom transactions in Humboldt, only one sale qualified as affordable at the 60% AMI benchmark—a coverage rate of 1.06%. Expanding the dataset to include studio condos increases the total to 96 transactions and three qualifying sales, raising the coverage rate to roughly 3%. All three affordable units were 0–1 bedroom condos; none were in the 2–3 bedroom range that aligns with Strong’s 54 family‑sized units. This pattern highlights a structural mismatch between Humboldt’s ownership inventory and the needs of 60% AMI households. Family‑sized homes—whether detached, attached, or larger condos—are effectively absent from the affordable ownership landscape, and even the most attainable options are limited to small, entry‑level condos. In this context, the Strong Family Apartments fill a critical gap by providing long‑term, income‑restricted, family‑oriented housing in a corridor where market‑rate ownership has become unattainable for moderate‑income households.

Plottage, Highest and Best Use, and Long‑Term Stability

Plottage and Assemblage Value

The site’s primary value driver is plottage—the incremental value created by combining multiple smaller tax lots into a single unified 0.96‑acre parcel. Prior to redevelopment, the Strong family’s holdings consisted of several fragmented lots occupied by a modest single‑family home and large areas of open grass, a clear underutilization in CM2 zoning, which is intended for medium‑scale mixed‑use and multifamily development along transit corridors.

Assemblage into one unified tax lot unlocked the development potential that individual parcels could not support. The combined footprint enabled a 75‑unit building with a central courtyard, family‑oriented amenities, on‑site services, and efficient circulation—elements that would have been infeasible or uneconomic on scattered lots. This is a textbook example of how public‑private coordination (PHB land banking and subsequent transfer) and zoning incentives (no parking minimums, height and floor-area ratio allowances) convert fragmented, low‑intensity land into a higher and better use.

Highest and Best Use Shift

Before redevelopment, the site’s highest and best use was not continued single‑family residential. While CM2 permits residential uses, the zone’s intent and incentives clearly favor denser multifamily or mixed‑use development on corridors like N Williams Avenue. Maintaining a single‑family home on nearly one acre represented a substantial underutilization of land value in an area with strong multimodal access and ongoing reinvestment.

The realized use—75 income‑restricted family units with courtyard amenities, bike parking, and resident services—aligns directly with CM2’s purpose. The project maximizes allowable density while securing long‑term affordability through a 99‑year regulatory agreement with PHB. The shift from low‑intensity residential to medium‑scale multifamily was made possible by assemblage, zoning compliance, and layered public financing.

Location Externalities

The Alberta/Williams corridor provides unusually strong positive externalities for income‑restricted households. WorkSource Oregon sits directly across N Williams Avenue, offering employment services, training referrals, and career support. Jefferson High School, KairosPDX, and PCC Cascade are all within a short walk or bike ride, creating a cluster of educational and youth‑focused resources. The corridor’s multimodal strengths—protected bike lanes, frequent transit, and walkable amenities—reinforce the project’s feasibility and support absorption for the target demographic.

Income Growth Retention and Long‑Term Stability

A defining feature of the project is tenant stability. Under federal LIHTC rules (the Next Available Unit Rule), households are not required to move out if their income rises after initial qualification. The 99‑year PHB regulatory agreement further ensures long‑term affordability, compliance, and adherence to the N/NE Preference Policy.

This structure supports upward mobility without displacement, stabilizes families over time, and aligns with anti‑displacement goals in N/NE Portland. By allowing residents to remain as their incomes grow, the project promotes continuity rather than churn—an important distinction in a corridor where market‑rate rents and ownership costs have escalated beyond reach for many moderate‑income households.

Takeaways

The Strong Family Apartments illustrate how targeted redevelopment can convert long‑term underutilization into meaningful community benefit. Through assemblage of multiple tax lots into a unified 0.96‑acre parcel, the site shifted from a modest single‑family home with expansive open space to a 75‑unit, family‑oriented affordable multifamily community. The project prioritizes the N/NE Preference Policy and incorporates a central courtyard, playground space, and SEI‑led youth, employment, and family‑stability services.

From an appraisal perspective, the development underscores the role of plottage in unlocking highest and best use. Combining fragmented parcels enabled the scale, density, and site planning required for medium‑scale multifamily in CM2 zoning, where incentives favor transit‑supported housing over low‑intensity residential. The result is a long‑term community asset serving moderate‑income families in a corridor where market‑rate ownership remains unattainable for many.

Long‑term stability is reinforced through the 99‑year affordability covenant and LIHTC’s income‑growth retention rules, which allow households to remain in place as earnings rise. This structure supports upward mobility without displacement and aligns with anti‑displacement goals in N/NE Portland.

In a neighborhood shaped by historical and ongoing pressures on housing access, the Strong Family Apartments demonstrate how zoning, public‑private coordination, and intentional design can preserve community ties while delivering durable affordability.

The Portland Appraisal Blog Affordability Index: PABAI

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

In 2025, Portland Region manufactured homes on owned land rebounded with 315 sales (+14.13%), $148.4M volume (+16.25%), average price $471,014 (+1.86%), and median $435,000 (+3.82%). Rural counties dominated, land value drove stability, and PABAI ranked it the second-most affordable housing segment (111.67).

The Portland White Stag sign. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

The manufactured‑home market in 2025 moved through a year defined by steadier demand, uneven inventory, and a noticeable shift in how long homes took to find the right buyer in some counties. Manufactured homes remain the second most affordable ownership segment in the Portland Region, right after condominiums. Yet the contrast between the two couldn’t be more stark: a condominium typically offers an apartment in an urban core with monthly dues and shared maintenance, while a manufactured home often delivers acreage in rural or pastoral settings—sometimes in remote locales.

Across the Portland Region, roughly 21,400 homes sold in 2025 across the four major residential segments. Manufactured homes accounted for less than 1.5% of that activity, but they continued to play a meaningful role in the market—often representing one of the few affordable paths to owning acreage.

The Portland Region in this update comprises the six Oregon counties of Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill. These counties form a contiguous housing ecosystem centered on Portland—Multnomah as the core home county, with the others tightly integrated through commuting patterns, economic ties, and shared market dynamics (e.g., Yamhill’s strong connection via Highway 99W and wine-country adjacency). Beyond Yamhill, the MLS system changes, further distinguishing this six-county area from broader geographic aggregations. For a detailed overview—including county profiles, population data, key value influencers, and why this definition differs from the official seven-county Portland–Vancouver–Hillsboro MSA—see our dedicated page: The Portland Region – Six-County Market Area Overview.

All data is sourced from RMLS and reflects open-market manufactured residential sales (excluding condominiums, attached homes, and site-built detached homes). SNL (“Sold Not Listed”) entries—off-market transactions entered retroactively—have been excluded to preserve consistency with true market activity.

All figures have undergone our standard cleaning process to address common RMLS accuracy challenges, including misclassifications (e.g. manufactured homes hiding in other categories, such as the detached category), square footage/price typos, incomplete fields, status/date mismatches, and non-representative entries. For a detailed overview of these issues, their impact on market analysis, and how we mitigate them through automated flagging, cross-verification, and manual review, see the dedicated page: RMLS Data Accuracy Challenges.

It is important to note that this review focuses on manufactured homes permanently affixed to land that is also owned by the same party. This means we are excluding classic mobile home parks where the owner of the mobile home must pay a lease/lot rental fee.

Portland Region 2025 Overview

Overall Regional Trends

The table below summarizes key metrics for attached single-family manufactured residential sales in the Portland Region (Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill counties) for 2025 compared with 2024.

Category

2024

2025

% Change

Total $ Volume

$127.6 Million

$148.4 Million

+16.25%

Average Price

$462,411

$471,014

+1.86%

Median Price

$419,000

$435,000

+3.82%

Avg SP/OLP

96.69%

96.14%

-0.57%

Avg PPSF (TSF)

$295.71

$299.03

+1.12%

Avg HOA Dues

$74.61

$72.60

-2.69%

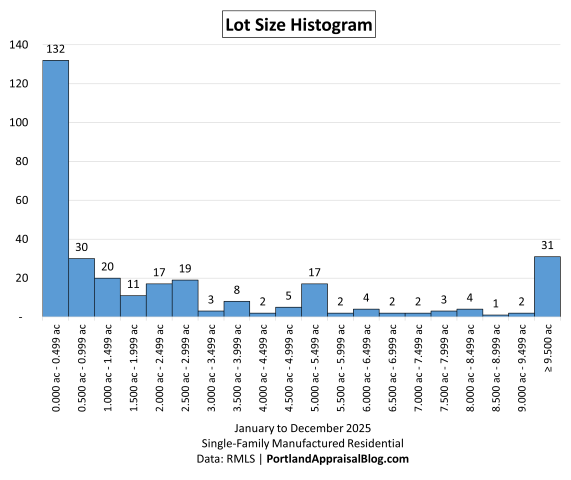

Avg Lot Size (ac)

3.48

3.44

-1.15%

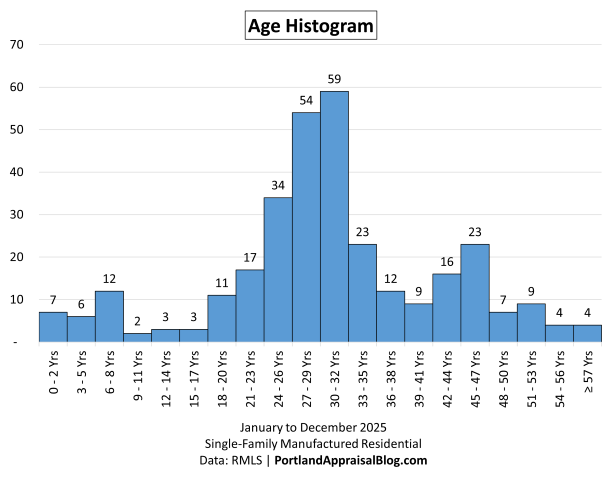

Avg Age (Yrs)

28.20

30.50

+8.14%

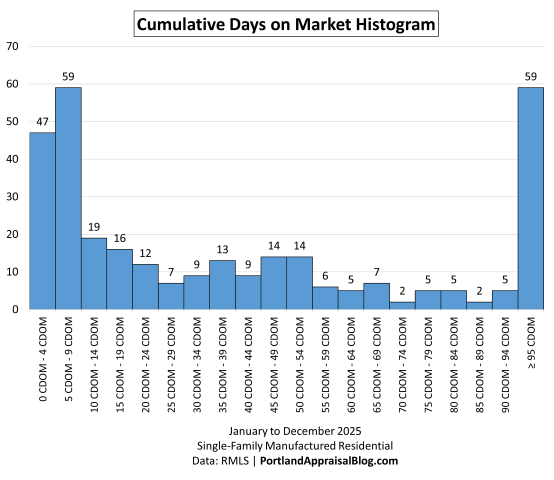

Avg CDOM

60.55

61.03

+0.79%

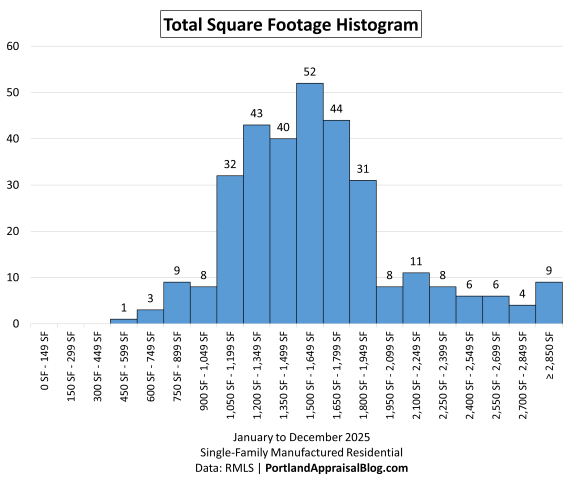

Avg Total SF

1,609

1,629

+1.24%

Total # of Sales

276

315

+14.13%

# of New Constr.

3

4

+33.33%

Avg Supply (Mos.)

4.34

4.09

-5.75%

# of REOs

7

4

-42.86%

# of Short Sales

0

0

—

Note: The calculated average HOA dues is for units reporting HOA dues (27 sales for 2025). All other metrics use the full dataset (315 sales for 2025). Single-Family Manufactured Residential | 2024 & 2025 Data: RMLS | PortlandAppraisalBlog.com

Key Observations From the Aggregate Data

Manufactured homes posted the strongest price gains of the four major housing segments, with both the average and median rising more than any other category in 2025. What makes this notable is that the segment didn’t rely on a shift toward larger homes or larger parcels; the underlying composition stayed remarkably stable, which means the appreciation reflects genuine demand strength rather than mix effects.

Sales activity expanded sharply, marking one of the largest year‑over‑year increases in the region. The rise in closed sales outpaced the modest changes in size, acreage, and days on market, signaling that more buyers were willing to engage with the segment even as inventory remained thin and the stock continued to age. This represented a return to form as 2023 had 310 sales and 2025 closed 5 additional sales.

County‑level performance was uneven but ultimately supportive of regional growth. Washington, Multnomah, and Hood River delivered clear price strength, each contributing meaningful upward pressure to the regional averages. Clackamas—by far the largest county by sales count—did not appreciate, but it held close to parity with 2024, providing the stability needed for the stronger counties to carry the region forward.

The segment’s physical profile barely changed, with total square footage and acreage holding near 2024 levels and the average home age increasing. In most years, an older stock profile would exert downward pressure on pricing; the fact that prices rose anyway reinforces that the appreciation was demand‑driven rather than structural.

Negotiation patterns and market pace remained steady, with only slight softening in sale‑to‑list ratios and days on market. Buyers were selective, but not disengaged; well‑prepared homes in desirable settings continued to attract firm pricing, while more remote or older properties required patience without signaling a broader slowdown.

Distressed activity stayed low, continuing a multi‑year trend of stability in the manufactured‑home segment. Even with an aging stock and a wide range of property conditions, bank‑owned and short‑sale activity remained minimal, underscoring the segment’s resilience.

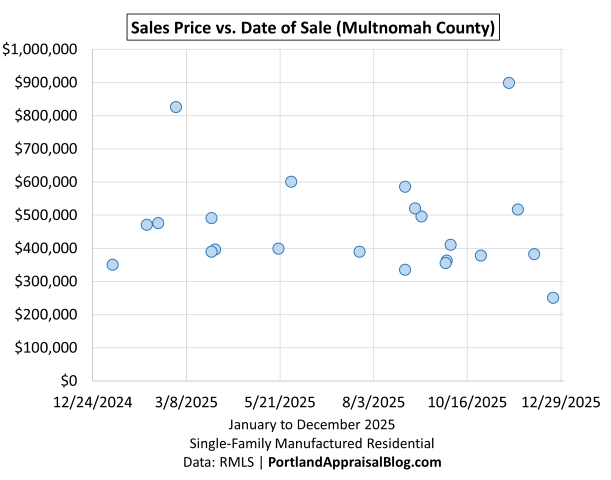

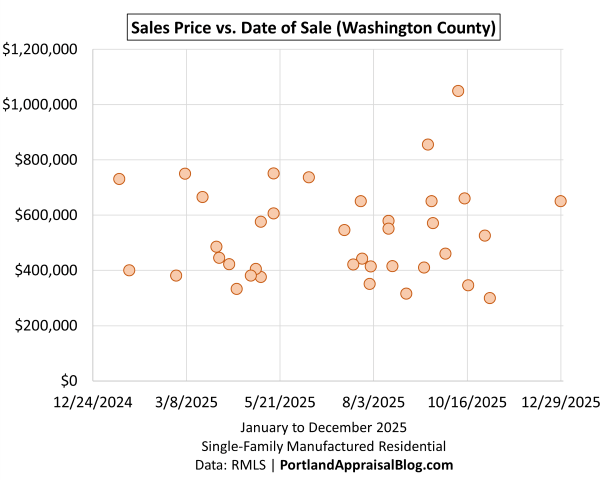

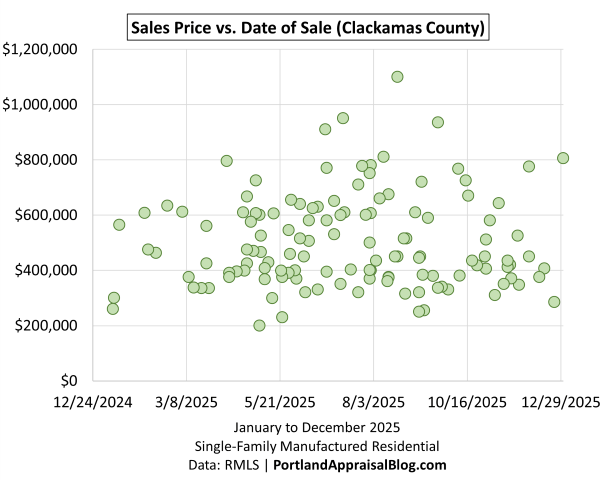

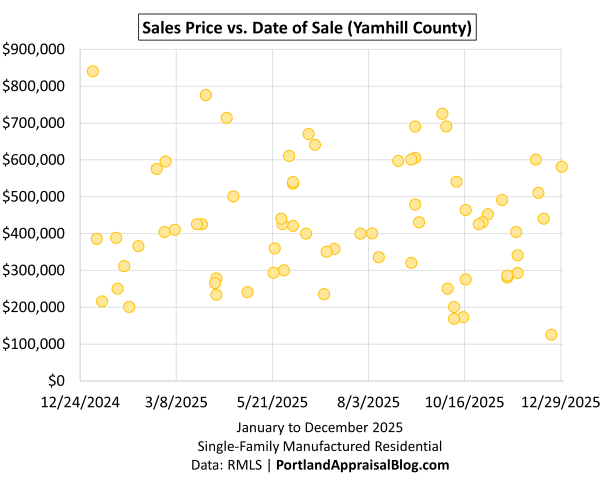

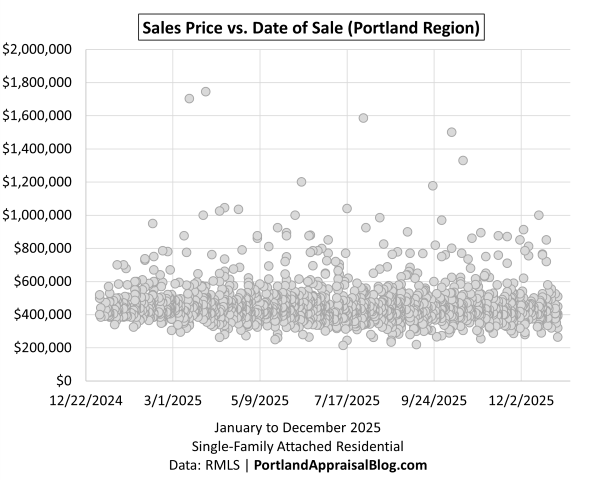

Portland Region Scatter Plots

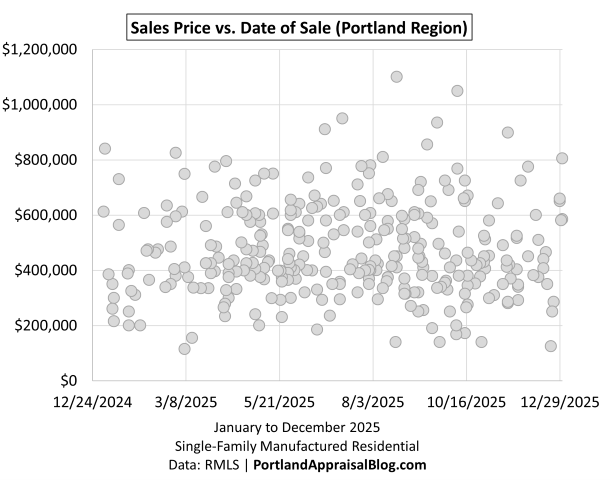

To visualize the distribution of individual manufactured homes sales prices across 2025, the following scatter plots show sales price against date of sale:

The 2025 sales‑price‑versus‑date scatter shows a remarkably steady rhythm for a segment as small and diverse as manufactured homes. Instead of the sharp seasonal swings that often appear in niche markets, the year unfolds as a consistent band of activity, with sales distributed evenly across all twelve months and no visible collapse in the early winter or late fall. The mid‑range of the market remains especially stable, forming a dense horizontal band that anchors the chart and reflects a year in which buyers and sellers were able to find agreement without dramatic shifts in pricing.

A subtle compression appears from late summer through the end of the year, with fewer low‑end outliers and a tighter clustering around the middle of the price distribution. This narrowing is not a sign of weakening; rather, it reflects a firmer pricing floor and a more consistent mix of properties entering the market in the second half of the year. The upper end of the market continues to register throughout this period, with several higher‑priced sales in the fall and early winter preventing the trendline from flattening and reinforcing the sense of a market that remained confident even as the year wound down.

Taken together, the scatter presents a picture of a segment that moved with calm, steady momentum. The absence of volatility, the persistence of a stable mid‑band, the tightening of the lower range, and the presence of late‑year upper‑band sales all point to a market supported by genuine demand rather than mix‑driven noise. The regional pattern is coherent and balanced, and the underlying county‑level dynamics that shaped this composite view become even clearer when examined individually in the latter sections.

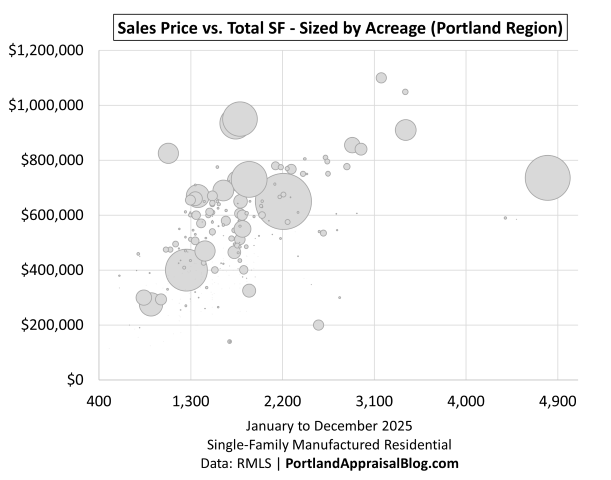

To visualize three important variables at one, the following scatter plot shows sales price versus total square footage with each dot sized by acreage (lot size):

The 2025 size‑based scatter shows a manufactured‑home market that organized itself with unusual clarity. Across the full range of square footage, the points form a coherent upward pattern: larger homes generally commanded higher prices, and the relationship holds consistently enough that the trendline is visible even without drawing it. This is not always the case in the MFH segment, where condition, setting, and acreage can create wide vertical dispersion. In 2025, the market behaved with a steadiness that mirrors the tempo seen in the sales‑price‑vs‑date-of-sale scatter.

Acreage adds a second layer of structure. Larger parcels appear as noticeably larger bubbles, and they tend to sit above the main body of the scatter. This is the classic manufactured‑home dynamic: land can elevate a property well beyond what its square footage alone would suggest. But the acreage premium shows up in a controlled, predictable way. The largest bubbles cluster in the upper half of the chart, but they do not distort the overall shape. Instead, they reinforce the idea that land remains a meaningful value driver without overwhelming the distribution.

The middle of the market—roughly 1,200 to 1,800 square feet and $300K to $600K—forms a dense, stable band that anchors the entire chart. This is where most of the region’s manufactured‑home stock lives, and the consistency of this band supports the conclusion that 2025 was a balanced, demand‑supported year. There is no hollowing out, no thinning, and no sign of a collapsing floor. The lower band remains present across the full range of square footage, but it does not expand downward or show distress. Older homes, modest parcels, and properties needing work appear where expected, but they do not dominate the distribution.

One of the more interesting features of the scatter is the presence of larger parcels at lower price points. Several sizable bubbles sit below the main trendline, showing that an eagle‑eyed and patient buyer can still acquire meaningful acreage at a reasonable price—especially when the home is older, dated, or in need of repair. This is a uniquely manufactured‑home phenomenon and one of the few remaining pathways to acreage ownership at accessible price levels.

A closer look at the three largest‑SF outliers: Three points sit well to the right of the main cluster. Yes, there are three, one is on a small lot and is nearly invisible! These three sales are the largest homes in the dataset and each has a clear, logical explanation once examined:

A 42.62‑acre North Plains fixer (cash) sits far below the trendline because the home contributed little value and the buyer was effectively purchasing the land. Its position reflects a classic land‑first MFH transaction.

A 0.64‑acre Multnomah sale (FHA) is nearly invisible on the scatter plot. The home is 4,495 SF and was designed for high‑occupancy use, with seven bedrooms, three bathrooms, dual entrances, and a layout suitable for care‑facility, sober‑living, or multigenerational configurations. Despite its size, the home sits on just over half an acre and sold with FHA financing. Its position on the scatter reflects the market’s tendency to discount institutional or cash‑flow‑oriented layouts, which offer utility but do not command the same price premium as conventional single‑family square footage.

A 2.5‑acre cash sale falls between the other two. This home is 4,385‑SF and combines a 2004 manufactured home with a 2006 stick‑built addition, creating a dual‑living layout. The home sold for cash and includes a barn, shop, multiple utility rooms, and extensive outdoor improvements. Its position on the scatter reflects the market’s tendency to discount unconventional or hybrid layouts, even when the overall utility and acreage are significant.

Bottom-line Summary

Taken together, the aggregate tables and the two regional scatter plots point to a manufactured‑home market that moved with steady, internally consistent momentum throughout 2025. Sales volume was up and prices held firm across the full range of the segment, with a stable mid‑band anchoring the year and no evidence of a collapsing floor or late‑year volatility. The sales‑price‑versus‑date scatter shows a smooth seasonal rhythm with a mild tightening in the second half of the year, while the size‑and‑acreage scatter reveals a market that valued square footage and land in predictable ways, even as it produced the occasional outlier that is characteristic of this segment.

The overall picture is one of broad‑based stability: genuine demand, a coherent price structure, and a distribution shaped more by steady buyer behavior than by mix shifts or one‑off anomalies. The county‑level sections that follow show how each sub‑market contributed to this regional pattern, and why the composite view looks as orderly as it does. But before we examine the individual counties let’s consider a variety of graphs to illuminate the regional data.

Sales Volume

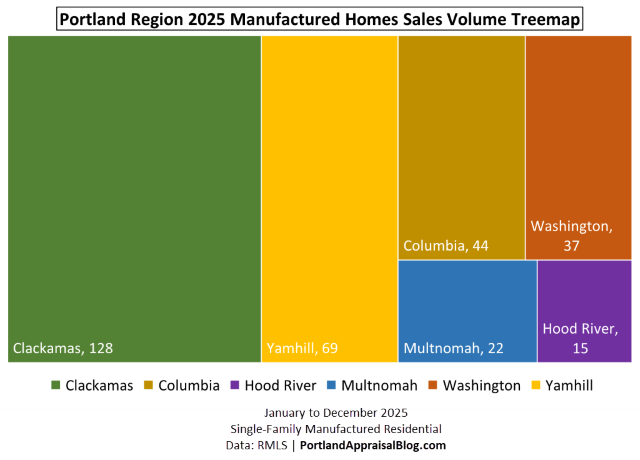

A treemap visualizing the distribution of manufactured homes sales by county in 2025 clearly illustrates the market’s geographic dispersion in this housing segment.

Manufactured‑home activity in 2025 followed a geographic pattern that is completely different from every other housing segment in the Portland region. In detached, attached, and condominium housing, the Big Three counties—Clackamas, Washington, and Multnomah—account for 90% to 99% of all sales. Manufactured homes break that rule entirely. The outlying counties carry a disproportionate share of the activity, and the market’s center of gravity shifts decisively away from the urban core.

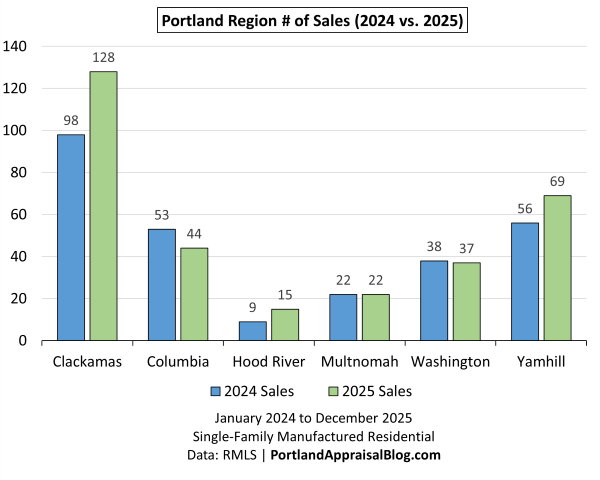

Clackamas led the region with 128 sales, forming the largest block of activity and anchoring the year’s volume. But the next‑largest contributor was not Washington or Multnomah—it was Yamhill, with 69 sales. Columbia followed with 44, and only then do Washington (37) and Multnomah (22) appear. Hood River, with 15 sales, rounded out the region. This distribution is not an anomaly; it reflects the structural reality of the segment. Manufactured homes are more common in rural and semi‑rural settings, where larger parcels, lower land costs, and flexible siting options support a broader range of housing stock.

Year‑over‑year changes reinforce the same pattern:

Clackamas and Yamhill both posted meaningful increases in 2025, Hood River grew from a small base, Columbia softened slightly, and Washington and Multnomah held steady. The uneven movement across counties is another way this segment diverges from the rest of the housing market, where the Big Three typically move in near‑unison and dominate the regional totals.

Despite the differences in scale, no county experienced a collapse in activity, and the overall regional volume increased from the prior year. This stability in the volume distribution is one of the reasons the 2025 scatter plots appear so orderly: the market was active, balanced, and supported by steady buyer participation across all twelve months.

This volume structure sets the stage for the analyses that follow. The counties with the largest footprints shape the regional trendlines, while the smaller counties introduce the nuances, acreage dynamics, and outliers that give the manufactured‑home segment its distinctive character.

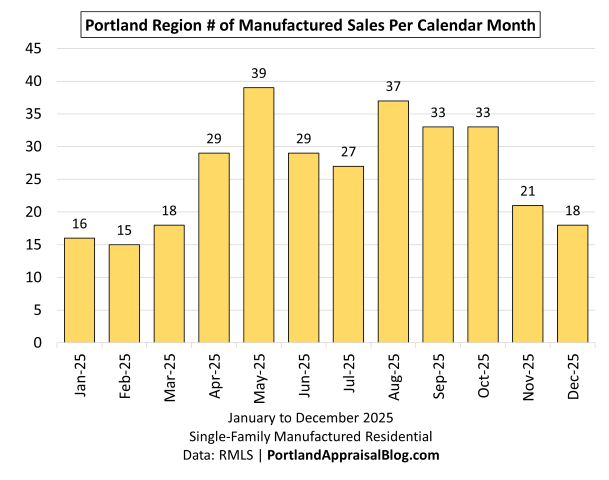

The following bar chart shows monthly sales volume for 2025:

The 2025 manufactured‑home market followed a classic seasonal pattern, with a slow winter start, a strong spring buildup, and a broad summer plateau that carried through early fall. January, February, and March posted modest activity, each in the mid‑teens to high‑teens, which is typical for this segment and reflects both weather constraints and the slower pace of rural and semi‑rural transactions. Activity accelerated sharply in April and peaked in May at 39 sales—the high point of the year and the moment when all counties were contributing meaningful volume.

The summer months held that momentum. June, July, August, September, and October all posted between 27 and 37 sales, forming a stable mid‑year band that kept the regional scatter plots well‑populated and prevented the kind of thin‑data volatility that can appear in smaller segments. This broad plateau is one of the reasons the 2025 price‑versus‑date scatter reads as smooth and orderly: the market had consistent participation across the warm months.

Volume tapered in November and December, returning to the high‑teens and low‑twenties. This decline mirrors the seasonal slowdown seen in detached and attached housing, but the manufactured‑home segment tends to soften a bit earlier and more noticeably because rural and acreage‑oriented transactions are more sensitive to weather, daylight, and site‑access conditions.

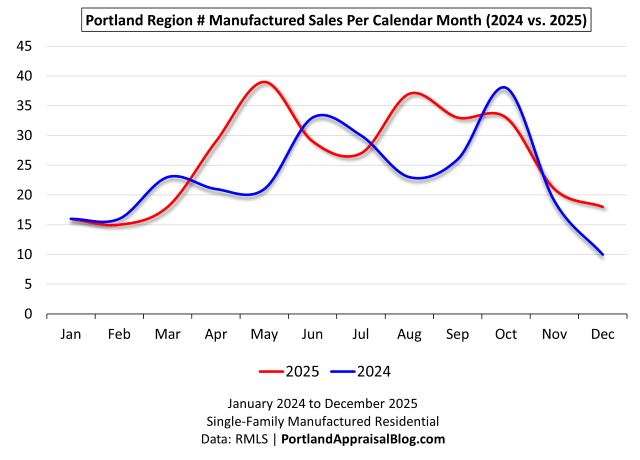

The line graph below compares monthly sales volume across the twelve months for 2024 and 2025.

The month‑by‑month comparison shows that 2025 was not just a stronger year in total volume—it was a more consistent and better‑balanced year across the calendar. Both years start in the mid‑teens, but the paths diverge quickly. In 2024, activity rose unevenly, with a strong March and June, a soft late summer, and a pronounced spike in October. By contrast, 2025 followed a smoother seasonal arc: a slow winter, a clear spring buildup, and a broad summer plateau that carried through early fall.

Several months illustrate this shift clearly. April and May 2025 were substantially stronger than the prior year, with May reaching 39 sales—nearly double the 2024 figure. August and September also outperformed their 2024 counterparts, reinforcing the sense of steady mid‑year demand. Even the late‑year slowdown behaved differently. While both years tapered in November and December, 2025 maintained higher activity, avoiding the sharp drop seen in December 2024.

Sales Price

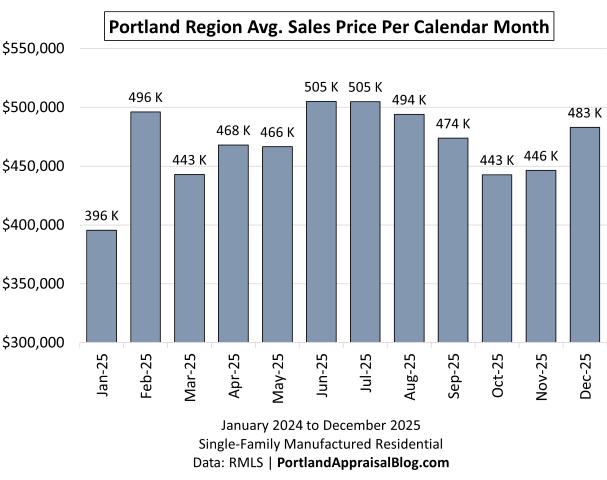

The following bar chart shows average monthly sales price for 2025:

Note: The y-axis starts at $300,000 to allow better examination of monthly differences.

Average prices in 2025 followed a smooth, well‑behaved seasonal arc that reflects a stable, demand‑supported manufactured‑home market. The year opened softly at $396K in January, which is typical for this segment given winter weather, rural access constraints, and limited buyer activity. Prices rose sharply in February to $496K and settled into the mid‑$400Ks through March, establishing the early‑spring lift that carried into the main selling season.

From April through August, the market held a steady mid‑year plateau. Monthly averages ranged from the high‑$460Ks to just over $500K, with June and July tied for the year’s peak at $505K. This consistency mirrors the strong mid‑year sales volume and is one of the reasons the price‑versus‑date scatter appears so orderly. The market had enough activity—and enough diversity of properties—to produce a stable pricing band without the volatility that can appear in smaller or more rural datasets.

Prices eased gently in September and October, returning to the mid‑$400Ks, but the decline was modest and short‑lived. November held firm at $446K, and December closed the year strongly at $483K, reversing the fall softness and signaling that buyer willingness remained intact even as the seasonal slowdown set in.

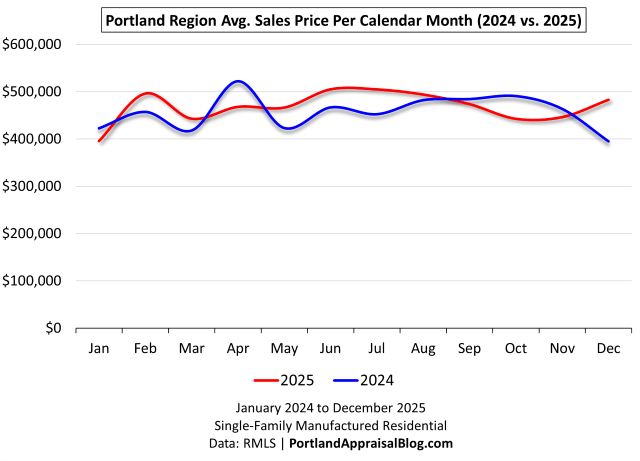

The line graph below compares average monthly sales prices across the twelve months for 2024 and 2025.

The year‑over‑year comparison shows two very different pricing rhythms. 2024 moved with sharper swings, including a pronounced April spike and a steep December drop, while 2025 followed a smoother, more stable seasonal arc with a firm close to the year. The contrast between the two lines reinforces the broader theme of 2025 as a steadier, more demand‑supported market.

Several months illustrate the divergence clearly. January and February opened with a reversal of roles: 2024 began higher in January, but 2025 surged ahead in February with a jump to $496K. Through spring, the two years traded places—2024 peaked at $522K in April, while 2025 held a more moderate but consistent mid‑$400K to mid‑$500K range. By early summer, 2025 had clearly taken the lead, with June and July both landing just above $500K, compared to mid‑$400Ks in 2024.

The late‑summer and early‑fall months show the same pattern. August and September were tighter between the two years, but 2025 maintained a slight edge. October and November flipped again, with 2024 briefly rising above 2025, but the difference was modest and short‑lived. The most striking contrast appears in December: 2025 closed at $482,952, while 2024 fell to $394,887, its lowest point of the year. That strong finish in 2025 reinforces the stability seen in the scatter plots and confirms that the market ended the year with pricing confidence rather than seasonal weakness.

Across the full calendar, 2025 shows a smoother, more coherent price structure, with fewer abrupt shifts and a stronger mid‑year plateau. The 2024 line, by comparison, reflects a more volatile pattern shaped by mix, timing, and thinner winter volume.

Cumulative Days on Market

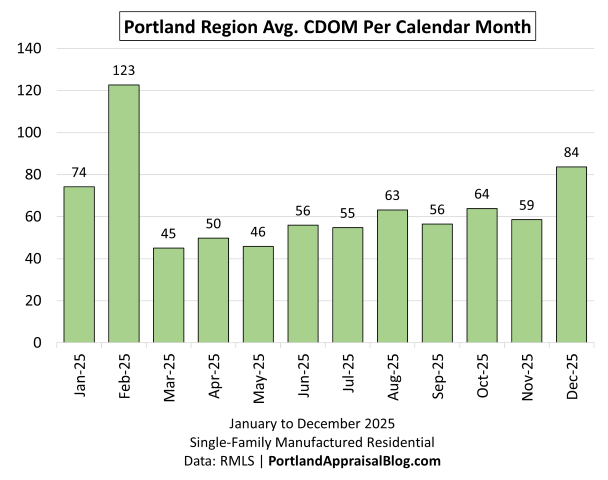

The bar chart below compares average cumulative days on market (CDOM) throughout 2025.

Cumulative Days on Market in 2025 followed a seasonal pattern that is typical for the manufactured‑home segment, but with enough mid‑year stability to reinforce the broader theme of a steady, demand‑supported market. January opened at 74 days—elevated but not unusual for winter, when rural access, weather, and buyer activity all slow. February spiked to 123 days, the highest point of the year, driven by a small number of older listings finally clearing. This kind of early‑year cleanup is common in this segment and does not indicate weakening demand.

From March through October, the market settled into a remarkably consistent mid‑year band. CDOM ranged from the mid‑40s to mid‑60s, with March at 45 days, April at 50, and May at 46. Even as volume increased in the spring and summer, marketing times remained stable, suggesting that buyers were active and well‑matched to available inventory. The summer months—June through August—held between 55 and 63 days, and September and October stayed in the mid‑50s to mid‑60s. This eight‑month stretch of steady CDOM is one of the clearest indicators that the 2025 market was functioning smoothly.

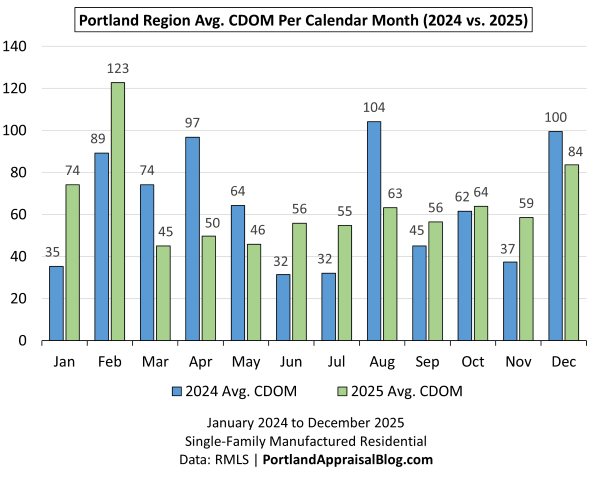

The bar chart below compares cumulative days on market for 2024 and 2025.

The year‑over‑year comparison shows that while the shape of CDOM changed noticeably between 2024 and 2025, the overall level barely moved. The annual averages were 60.55 days in 2024 and 61.03 days in 2025—a difference of less than half a day. In a small segment like manufactured homes, this is exactly what you expect: the monthly pattern can shift dramatically depending on which slow listings clear when, but the underlying market tempo remains stable.

The month‑to‑month behavior is where the two years diverge. Early 2025 opened with elevated winter CDOM—74 days in January and 123 in February—driven by a handful of older listings finally closing out. In contrast, 2024 began unusually low before rising into the 80–90‑day range. Spring flipped the pattern again: 2025 settled quickly into the mid‑40s to mid‑50s, while 2024 spiked to 97 days in April. Summer showed the same contrast, with 2025 holding steady in the mid‑50s to low‑60s and 2024 swinging from the low‑30s in June and July to 104 days in August.

Despite these very different seasonal shapes, both years ultimately lived in the same CDOM neighborhood. Neither year shows evidence of systemic softening, prolonged marketing times, or inventory backing up. Even the late‑year divergence—2024 ending at 100 days versus 84 in 2025—reflects timing and mix rather than a structural shift in demand. Manufactured‑home markets often show sharper winter variability due to rural access, weather, and financing logistics, and both years behaved within that normal envelope.

The key takeaway is that 2025 wasn’t meaningfully “faster” or “slower” than 2024. It was simply smoother. The mid‑year band in 2025 was more stable, the volatility was lower, and the seasonal rhythm was more predictable. The nearly identical annual averages underscore that the manufactured‑home market maintained a consistent, balanced tempo across both years.

Housing Supply

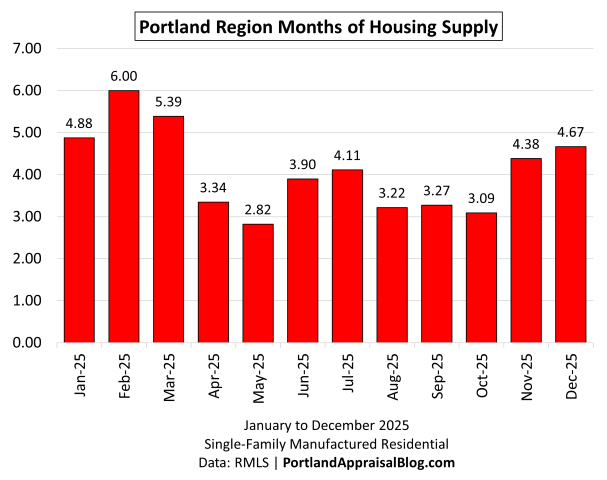

Months of supply (MOS) represents the number of months it would take to absorb current active inventory at the prevailing sales pace, assuming no new listings enter the market. The following bar chart shows MOS by calendar month for 2025:

Months of Housing Supply in 2025 moved through a clean, seasonal arc that mirrors the stability seen in pricing, volume, and CDOM. The year opened with elevated winter supply—4.88 months in January and 6.00 months in February—a normal pattern for manufactured homes, where rural access, weather, and slower buyer activity tend to stretch inventory relative to sales. From there, supply tightened quickly as spring demand arrived. March dropped to 5.39 months, and April fell sharply to 3.34 months, setting up the strongest stretch of the year.

The core of the market—May through October—held a remarkably stable band between roughly 2.8 and 4.1 months. May posted the year’s low at 2.82 months, reflecting strong absorption and a well‑matched buyer pool. June and July rose modestly into the 3.9–4.1 range, and August through October settled into a tight cluster between 3.09 and 3.27 months. This six‑month plateau is one of the clearest indicators that the 2025 manufactured‑home market was balanced and functioning smoothly. Supply was neither constrained nor excessive; it simply tracked demand in a predictable, orderly way.

The late‑year rise—4.38 months in November and 4.67 months in December—is exactly what you expect in this segment. Manufactured homes often see sharper winter slowdowns due to siting logistics, inspections, and financing timelines, and 2025 behaved squarely within that normal envelope. Importantly, even the year‑end levels remained moderate. There was no sign of inventory backing up or buyers stepping away.

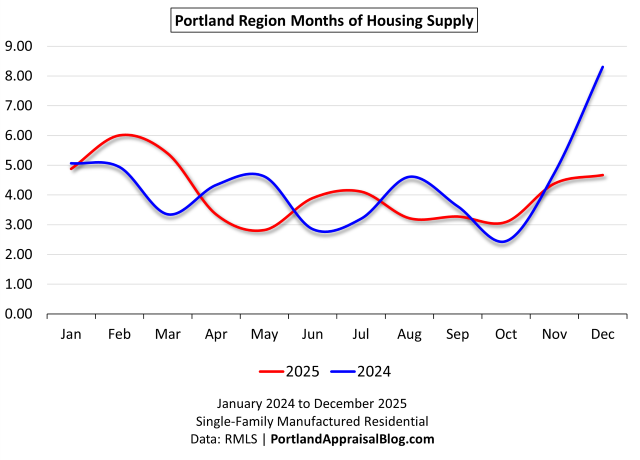

The line graph below compares months of supply for 2024 (blue line) and 2025 (red line), with a full y-axis scale to show true proportional differences:

The year‑over‑year comparison shows that while the month‑to‑month pattern of housing supply shifted noticeably between 2024 and 2025, the overall level of inventory remained almost identical. The annual averages were 4.34 months in 2024 and 4.09 months in 2025, a difference of just a quarter of a month. In a small segment like manufactured homes—where a handful of listings can swing a single month—this near‑match in annual supply is expected. What changed was the seasonal shape, not the underlying balance between listings and sales.

The two years diverged early. January and February 2025 opened with 4.88 and 6.00 months of supply, while 2024 began slightly lower at 5.06 and 4.94. By March, the pattern flipped: 2025 eased to 5.39 months, while 2024 tightened sharply to 3.35. Spring continued the alternating rhythm. April and May 2025 dropped to 3.34 and 2.82 months, reflecting strong absorption, while 2024 rose to 4.33 and 4.62. Summer followed the same back‑and‑forth dynamic. June and July 2025 held at 3.90 and 4.11 months, compared to 2.85 and 3.20 in 2024, before August reversed the relationship again with 3.22 months in 2025 versus 4.61 in 2024. Through early fall, 2025 held a tight, stable band between 3.09 and 3.27 months, while 2024 ranged from 3.62 down to 2.45.

The most dramatic difference appears in December. Supply spiked to 8.30 months in 2024, the highest point across both years, while December 2025 closed at 4.67 months, elevated but still within a normal seasonal range. This single month accounts for much of the visual gap between the two lines and reflects timing and mix rather than a structural imbalance.

Despite the month‑to‑month volatility, both years lived in the same overall supply environment. Neither shows evidence of inventory backing up or buyers stepping away. The mid‑year plateau in 2025—roughly three to four months of supply from May through October—reinforces the broader theme of a balanced, well‑functioning market. The 2024 line, by contrast, is more jagged, shaped by thinner volume and a few months where slower listings accumulated. The nearly identical annual averages—4.34 vs. 4.09 months—underscore that the manufactured‑home market maintained a consistent, stable supply profile across both years, even as the monthly curves took different paths.

Histograms

Histograms offer a unique and powerful perspective on the manufactured homes market that traditional summary statistics and bar charts cannot fully capture: they reveal the underlying shape, spread, and clustering of the data, exposing patterns, skewness, tails, and bifurcations that averages and medians alone obscure.

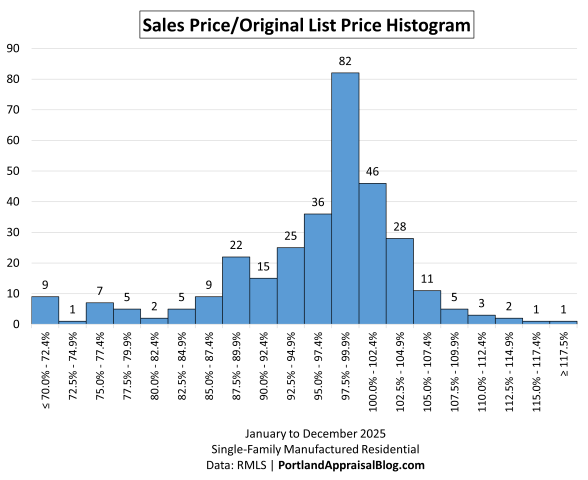

The following histogram shows the distribution of sales price as a percentage of original list price in 2025:

The distribution of sale‑to‑list ratios in 2025 shows a market that centered tightly around full price, with most transactions occurring in a narrow band and only light activity at the extremes. The single largest bin—97.5% to 99.9%—contains 82 sales (26.03%), and the surrounding bins at 95.0%–97.4%, 100.0%–102.4%, and 102.5%–104.9% add another substantial block of activity. Once aggregated, the full 95% to <105% band contains 192 sales, representing 60.95% of all transactions. This is the clearest signal in the dataset: the manufactured‑home market in 2025 rewarded accurate pricing with highly predictable outcomes, and most homes sold within just a few percentage points of their original list price.

Below‑list activity was present but modest. All bins under 90% of list total 60 sales (19.05%), spread thinly across many small ranges. No single low‑ratio bin dominates, and the counts taper quickly as ratios fall. These cases likely reflect idiosyncratic situations—condition issues, location constraints, or listings that began overpriced and required significant repositioning—rather than a structural pattern of deep discounting.

The upper tail behaves similarly. At 105% or above, the combined bins total 23 sales (7.3%), with each individual range containing only a handful of transactions. These are the occasional competitive situations where buyers stretched above list—clean acreage, desirable settings, or well‑prepared homes—but they remain the exception rather than the rule.

Taken together, the histogram shows a market with a very stable pricing center and only light activity at the extremes. The dominant pattern is straightforward: nearly two‑thirds of all manufactured‑home sales closed within 5% of the original list price, and the remaining third is split between modest under‑list adjustments and a small number of above‑list outcomes. The distribution reinforces the broader theme of the 2025 manufactured‑home market—steady demand, accurate pricing, and predictable negotiation dynamics.

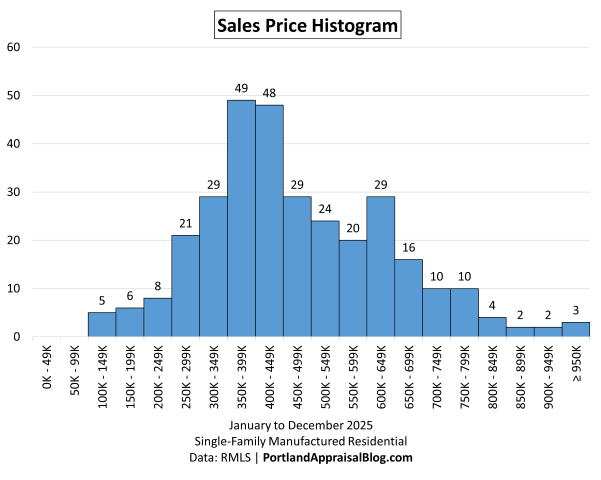

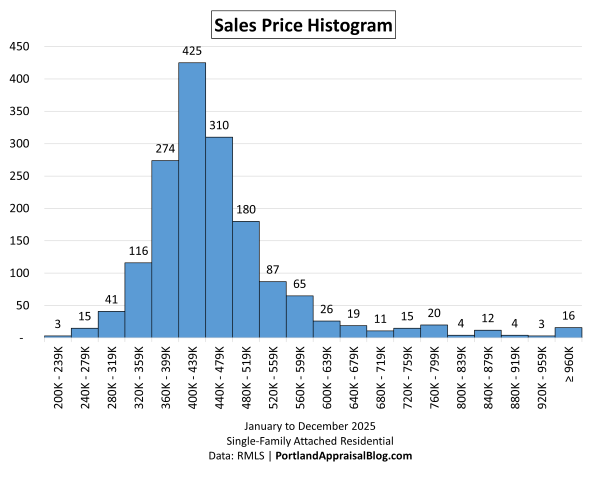

The following histogram shows the distribution of sales prices of manufactured homes in 2025:

The 2025 sales‑price histogram shows a market with a clear middle, a long but orderly tail, and no distortive spikes—exactly what you want to see in a manufactured‑home dataset of this size. The distribution builds gradually from the low end, peaks cleanly in the mid‑price ranges, and then tapers in a predictable pattern as prices rise.