What Happened This Week

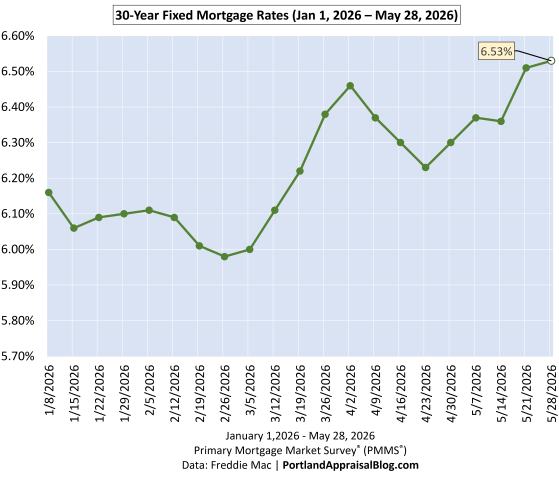

Mortgage rates climbed again this week to 6.53%, marking the third straight weekly increase. The broader 2026 pattern is now clear: rates bottomed on March 5th, surged sharply through early April, cooled briefly, and then reversed course on April 23rd. With this week’s move, we are now sitting at the highest 30‑year fixed rate of the year, and the spring cooldown is definitively over.

Affordability has deteriorated in step with these increases. Monthly payments are now higher than at any point in 2026, and the upward pressure on rates has pushed qualifying costs well above their early‑March lows. As the charts below show, today’s rate sits at the top of the year‑to‑date range, and the PABAI reflects a worsening affordability trend for the Portland Region as we move deeper into the spring market.

Mortgage Rate Context

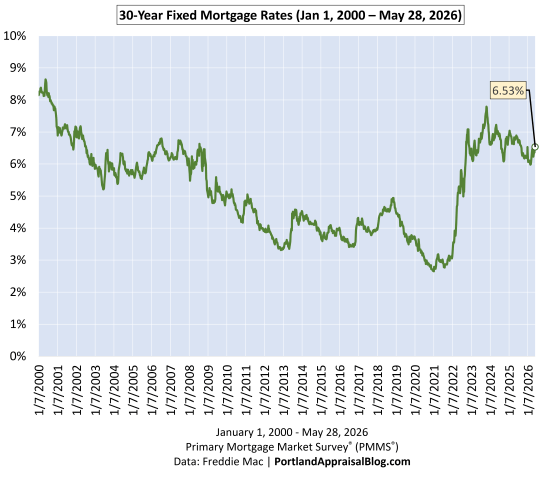

Long‑Run View (Since 2000)

The long‑run chart shows how today’s rate fits into a 25‑year history of mortgage cycles. The early 2000s sat in the 6–8% range, the post‑Great Recession era brought a decade of unusually low rates, and the pandemic period pushed borrowing costs to historic lows. Years after leaving that ultra‑low‑rate environment, the market continues to adjust to more difficult financing constraints, and today’s 6.53% reflects that ongoing shift.

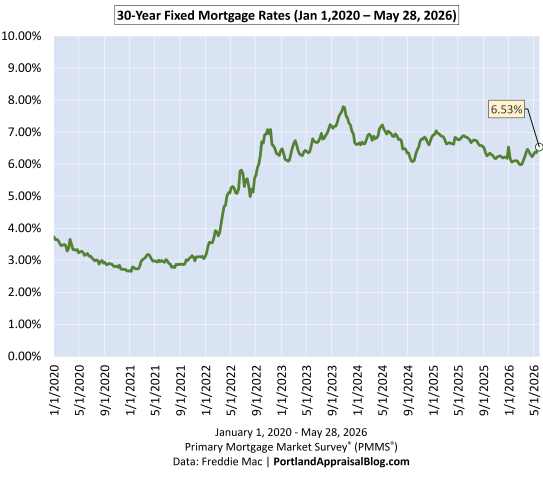

Medium‑Run View (Since COVID)

The COVID‑era chart highlights the dramatic rate compression of 2020–2021, the rapid surge of 2022, and the choppy plateau that has defined the past two years. Rates have been oscillating between roughly 6% and 7% since mid‑2023, and the recent climb places today’s rate near the upper end of that band. Volatility has cooled compared to 2022, but the medium‑run trend remains one of elevated and persistent borrowing costs.

Short‑Run View (2026 YTD)

The year‑to‑date chart shows the full shape of the 2026 cycle: a clear bottom on March 5th, a sharp rise into early April, a brief cooldown, and a reversal beginning April 23rd. With this week’s increase, the 30‑year fixed now sits at its highest level of the year, and the upward pressure has pushed affordability to its weakest point of 2026. This short‑run pattern is the most relevant for buyers today, as it directly shapes monthly payments and qualifying power.

Portland Appraisal Blog Affordability Index (PABAI)

What PABAI Measures

The Portland Appraisal Blog Affordability Index (PABAI) measures how the average home close price compares to what a median‑income household can qualify for under standard lending assumptions (HUD Portland‑Vancouver‑Hillsboro MSA median income, 20% down, and a 28% DTI for principal, interest, taxes, insurance, and HOA dues).

Unlike national affordability indices, PABAI is built from actual RMLS transactions—all 3,349 detached sales for the Portland Region in Q1 2026—which allows for far more precise, locally grounded insights into Portland‑area affordability than any national model can provide.

A PABAI of 100 means the market is exactly affordable at that income level (the Q1 2026 HUD median MSA income was $124,100 for a family of four). Values above 100 indicate excess qualifying capacity (more affordable), while values below 100 indicate a shortfall (strained affordability). Full methodology and the interpretation scale are available on the PABAI explainer page.

| PABAI Range | Interpretation |

|---|---|

| 120+ | Strongly Affordable |

| 100–119 | Moderately Affordable |

| 80–99 | Strained |

| Below 80 | Severely Constrained |

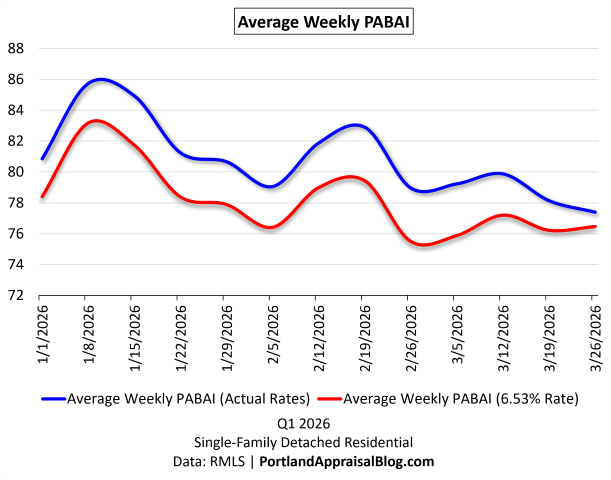

Q1 2026: Actual vs. Fixed‑Rate Affordability

The Q1 chart compares two versions of PABAI: one using actual weekly mortgage rates, and one using the current rate (6.53%) as a constant. Because the constant‑rate line uses the highest rate of the year, it naturally sits below the actual‑rate line for most of the quarter. That part isn’t the story.

The key insight is the size of the gap between the two lines. Early in the quarter, actual rates were meaningfully lower than the current rate (YTD high), giving buyers more qualifying power than a flat‑rate environment would suggest. But as rates climbed through March and into April, the two lines began to converge—a visual confirmation of how persistent rate increases have eroded affordability heading into spring.

Structural Unaffordability and the Seasonal Pattern

Detached homes in the Portland region remain structurally unaffordable to a household earning the HUD median MSA income. PABAI has been below 100 for years, and Q1 2026 continues that pattern. What the chart makes clear is that winter remains the best window for buyers on tight qualifying budgets: affordability improves when rates soften and seasonal pricing cools. As spring approaches, both rates and prices firm up, and affordability reliably compresses.

With the 30‑year fixed now at its highest level of 2026, the convergence of the two PABAI lines at the end of the quarter reflects the same reality: rising rates have pushed qualifying costs to their weakest point of the year.

Affordability Snapshot (This Week)

Q1 2026 Affordability Recomputed at Today’s Rate

The table below shows how Q1 2026 affordability metrics change when all 3,349 detached sales are recalculated at this week’s 6.53% rate. This is the clearest way to see how rising rates reshape qualifying power, housing burden, and the share of homes accessible to a median‑income household.

| Metric | Actual Q1 2026 | Recomputed at Today’s Rate | Change |

|---|---|---|---|

| Average PABAI | 80.47 | 77.77 | −2.70 |

| Required income (28% ratio) | ~$154,219 | ~$159,579 | +3.48% |

| Median‑income shortfall | 24.3% | 28.59% | +4.29 pts |

| Average monthly mortgage payment | $4,174.06 | $4,317.75 | +$143.69 |

| Housing burden (DTI) | 40.36% | 41.75% | +1.39 pts |

| Affordable homes | 738 | 597 | −141 homes |

| Share of homes affordable | 22.0% | 17.8% | −4.2 pts |

HUD Portland‑Vancouver‑Hillsboro MSA median income: $124,100

Data: RMLS (3,349 observations) | PortlandAppraisalBlog.com

How Rising Rates Reshape Affordability

Taken together, these metrics show how quickly affordability erodes when rates rise into the mid‑6% range. The drop in PABAI from 80.47 to 77.77 may look modest at first glance, but it represents a meaningful tightening of qualifying power across the entire detached market. Required income rises to nearly $160,000, widening the gap between what a median‑income household earns and what the market demands. That shortfall now approaches 29%, a reminder that the typical Portland household is operating well outside traditional affordability thresholds.

The payment side tells the same story. Recomputing Q1 sales at today’s rate pushes the average monthly mortgage obligation up by roughly $144, which may seem incremental on a monthly basis but compounds sharply over a 30‑year horizon. More importantly, the higher rate pushes the average front‑end debt-to-income ratio from 40.36% to 41.75%, a level that would be considered stretched even in more forgiving underwriting environments. These shifts are not abstract; they directly shape who can buy, what they can buy, and how competitive they can be.

The Buyer‑Side Impact

The most visible consequence of these changes is the shrinking pool of homes accessible to a median‑income household. Under actual Q1 2026 rates, 738 detached homes were affordable; at today’s rate, that number falls to 597. In percentage terms, the share of the market within reach drops from 22.0% to 17.8%—a loss of more than four percentage points in a single recalculation. This is the practical expression of rising rates: fewer viable options, tighter qualifying margins, and a market that becomes increasingly selective about who can participate.

For buyers, the experience varies by circumstance but the direction is the same. Households with limited flexibility feel the tightening most acutely, as even small rate movements can eliminate entire segments of the market. Move‑up buyers face a widening payment gap between their current home and the next one, making the trade‑up calculus more difficult unless equity is substantial. Cash buyers, by contrast, gain relative leverage as financed demand thins, though that advantage is uneven across price tiers.

Across all buyer types, the message is consistent: rising rates are reshaping the market in real time, and the affordability landscape at a 6.53% mortgage rate is meaningfully different from the one buyers faced just a few months ago.

The Seller‑Side Impact

Rising rates don’t just reshape the buyer experience—they influence seller outcomes as well. In the 2025 detached market, cumulative days on market (CDOM) increased 11.09%, and the current rate environment suggests that upward pressure on market times may persist. As affordability tightens and the pool of qualified buyers shrinks, homes that would have moved quickly in a lower‑rate environment may begin to sit longer, particularly in segments where pricing is already stretched. This doesn’t imply an abrupt market shutdown, but it does mean sellers need to price with greater precision and expect a more selective buyer pool as 2026 progresses.

Closing Thoughts

The story of this week is straightforward: mortgage rates have climbed to their highest level of 2026, and the effects are visible across every affordability metric. The PABAI continues to signal structural strain for median‑income households, and the recalculated Q1 data shows how even modest rate movements reshape qualifying power, monthly payments, and the share of homes within reach.

For buyers, the takeaway is that financing conditions remain tight and are tightening further as we move deeper into the spring market. Winter continues to offer the best affordability window, but the current rate environment means households on the margin will feel pressure sooner and more sharply than in prior years.

For sellers, the implications are more subtle but no less real. Last year’s detached market saw CDOM rise more than 11%, and the present rate backdrop suggests that trend may persist. A smaller pool of qualified buyers and higher monthly payments can translate into longer market times, especially for homes priced aggressively or positioned in segments where affordability is already stretched. Pricing discipline and realistic expectations matter more in this environment than they did during the ultra‑low‑rate era.

As always, the Portland market adapts—sometimes quickly, sometimes reluctantly—but the direction of travel is clear. Higher rates are reshaping both sides of the transaction, and the spring of 2026 is operating under the most constrained financing conditions we’ve seen this year.

Sources & Further Reading

All data presented in this quarterly update is sourced directly from RMLS and has been subjected to my rigorous cleaning and validation process to ensure reliability for detached single-family residential analysis in the six-county Portland Region. The trends, comparisons, and commentary are the result of original appraisal expertise and independent analysis—not aggregated from secondary sources or news summaries.

- The Portland Region – Six-County Market Area Overview: Portland Appraisal Blog

- RMLS Data Challenges: Portland Appraisal Blog

- Portland Affordability Index – PABAI: A Realistic Housing Qualification Metric for the Portland Region: Portland Appraisal Blog

- HUD Portland-Vancouver-Hillsboro, OR-WA MSA: Median Household Income

- The 2025 Portland Region Detached Homes Market in Review: Portland Appraisal Blog

Coda

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

{kind=link}