Mandatory valuation bias & fair housing training is now required for all appraisers as of January 1, 2026. Quick breakdown of the AQB’s 7-hour CE requirement (4-hour refreshers after), plus the recent scrutiny and mixed outcomes driving it. Most appraisers deliver fair, data-driven valuations daily—this reinforces transparency and trust.

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Portland’s Ritz-Carlton Residences: Luxury tower with stunning views and hotel perks…but only 11 of 132 units sold through 2025, with buyers demanding massive discounts averaging $274,000 off original prices. Cuts starting at 50% are anticipated as major repositioning rolls out in 2026.

This is a classic case of location, location, location—the developers priced it like the Pearl District, but Portland Downtown’s condo market had other ideas.

Full in-depth analysis, charts, sales data, and what it means for buyers/lenders/developers in my latest blog post:

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Portland’s Title 11 Tree Code protects urban canopy but imposes mitigation fees ($472/inch), penalties ($1,000/day), and Heritage deed restrictions. This brief explores resale amenity value vs. redevelopment burdens for property owners.

Mature tree canopy arching over a residential street in Portland’s Arbor Lodge neighborhood (September 2025). This type of shaded, park-like setting is frequently marketed as an amenity in resale listings. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Trees define Portland’s character—from tree-lined residential streets to the vast canopies of Forest Park and Mt. Tabor. The City of Portland’s Title 11 Tree Code establishes comprehensive regulations for tree preservation on private property within city limits.

Portland City Code Chapter 11.00.010 outlines the code’s purpose:

Trees are a fundamental component of the City’s green infrastructure. The chapters within this Title address trees in both development and nondevelopment situations and seek to enhance the quality of the urban forest and optimize the benefits that trees provide. Desired tree benefits include:

1. Providing oxygen and capturing air pollutants and carbon dioxide; 2. Maintaining slope stability and preventing erosion; 3. Filtering stormwater and reducing stormwater runoff; 4. Reducing energy demand and urban heat island through shading of buildings and impervious areas; 5. Providing visual screening and buffering from wind, storms and noise; 6. Sustaining habitat for birds and other wildlife; 7. Providing a source of food for wildlife and people; 8. Maintaining property values and the beauty, character and natural heritage of the City; and 9. Meeting the multi-purposed objectives of the Urban Forest Plan, including reaching and sustaining canopy targets for various urban land environments.

These goals are laudable and align with Portland’s identity as a tree-rich city. Yet real-world implementation has generated significant friction for property owners—permit requirements, mitigation costs, enforcement actions, and occasional liability when protected trees fail.

In Q3 2025 closed detached single-family sales within the City of Portland, “tree” or “trees” appeared in listing remarks for 660 of 1,519 transactions (43%). Properties marketed with tree mentions averaged $678,689—$51,371 higher than those without. After regression-based adjustments for differences in living area ($267.72 per Total SF) and lot acreage ($347,496 per acre), an approximate $23,500 difference remained in favor of the tree-mention cohort. This observational finding—not a controlled paired-sales analysis—suggests the market may reward mature canopy as a contributory amenity in established resale properties. Because listing photographs frequently communicate tree presence more effectively than remarks, and because other influential variables (such as neighborhood, condition, and level of updating) are not controlled for here, the remaining price difference should be viewed as a general market indicator rather than a precise contributory estimate.

Ironically, the same trees that appear to support resale premiums can impose substantial constraints during redevelopment, additions, or even routine ownership.

Trees as Amenity: The Resale Perspective

Mature trees provide shade, privacy, and aesthetic appeal that buyers prize in Portland’s established neighborhoods. The high frequency of tree mentions in marketing remarks (43% in Q3 2025) reflects agent confidence in canopy as a selling point.

Since July 1, 2025, most non-development tree permit applications (routine pruning, removal, or replanting on existing homes) carry no charge—thanks to Portland Climate Emergency Fund support. This relief reduces ongoing maintenance costs for homeowners and reinforces the perceived contributory value of large trees in resale transactions.

Professional care is often required for large specimens to avoid safety issues or violations.

Professional arborist pruning a large tree using a bucket truck in the Portland metro area—illustrating the specialized care often needed for mature canopy under Title 11 regulations. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Trees as Burden: Real-World Homeowner Experiences

While the code’s environmental intent is clear, enforcement and preservation mandates have created documented challenges for property owners.

In one prominent case, a Southwest Portland family sought removal of a leaning Douglas-fir they considered hazardous. Urban Forestry denied the permit. During the January 2024 ice storm, the tree collapsed onto their home—narrowly missing their young daughter. The family filed suit in April 2025, seeking $4.7 million in damages; the lawsuit remains ongoing as of January 2026.

These incidents illustrate the liability risk when protected trees become dangerous—yet removal options remain restricted. Reports nationwide echo warnings: unauthorized tree cutting has led some property owners to severe financial consequences, including liens or loss of equity.

Illustrative example of tree-failure damage to a single-family home during the January 2024 ice storm in the Portland metro area (Bethany neighborhood, Washington County)—unrelated to the Bond family lawsuit but demonstrating the severity of ice storm impacts and risks posed by large, vulnerable trees. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Title 11 Fundamentals: Tree Removal Permits and Notice Requirements

Title 11 protects private trees 12 inches or larger in diameter at breast height (DBH—measured 4.5 feet above ground). Lower thresholds (6 inches DBH) apply in environmental overlay zones.

Tree removal permits fall into two categories: Type A (simpler, no public notice) and Type B (public notice and appeal opportunity). Type A covers smaller trees, limited numbers of healthy trees, dead/dying/hazardous trees, and one large healthy non-nuisance tree per residential lot per year.

Permit Type

Proposal

City/Street or Private

Public Notice/Appeal

A

Any Type A request1

City/street/ Private

No

A

Up to four healthy <20″ diameter nuisance and non-nuisance species trees

City/street

No

A

≥20″ diameter, healthy nuisance or non-nuisance species tree

City/street

No

B

More than four healthy >12″ diameter nuisance and non-nuisance species trees

City/street

Yes

B

≥20″ diameter, healthy non-nuisance species tree

Private

Yes2

B

More than four healthy ≥12″ diameter non-nuisance species trees

Private

Yes

Table 30-1 from Portland City Code Title 11, summarizing public notice and appeal requirements for tree removal permits. Type B permits—required for most removals of large healthy private trees—trigger neighbor notification and potential appeals.

Note 1: The applicant may appeal any Type A or B permit decision.

Note 2: No public notice or opportunity for public appeal is required for removal of one healthy non-nuisance species tree ≥20″ diameter per lot per calendar year in any residential zone.

Root Protection Zones and Buildable Area Constraints

During construction, root protection zones (RPZ) extend roughly one foot of radius per inch of trunk diameter. Encroachment is limited, and fencing plus arborist oversight are mandatory.

On typical R-5 or R-2.5 lots, multiple large trees can shrink buildable area by 20–40%, forcing smaller footprints or eliminating partition potential—directly affecting highest and best use for infill or teardown sites.

Summer foliage on a tree in a Portland neighborhood. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Mitigation and In-Lieu Fees: The Primary Development Cost

When preservation standards are not met (generally one-third of regulated trees), options include on-site replanting or payment into the Tree Planting and Preservation Fund.

The primary development mitigation is the per-inch fee paid to the fund for off-site planting and 5-year establishment. An alternative flat fee per on-site tree applies when partial retention or replanting occurs but full density is not achieved—often used when site constraints limit complete preservation.

Per City Code 11.10.070:

Where allowed by other provisions of this Title, a fee may be paid into the Tree Planting and Preservation Fund in lieu of planting or preserving trees. The fee per tree is the entire cost of establishing a new tree in accordance with standards described by the City Administrator. The cost includes materials and labor necessary to plant the tree, and to maintain it for five years. The fee will be reviewed annually and, if necessary, adjusted to reflect current costs.

Current FY 2025–26 rates (effective July 1, 2025):

Category

Fee

Planting and Establishment Fee in Lieu (primary development mitigation)

$472.00 per DBH inch

Planting and Establishment Fee in Lieu (per on-site tree alternative)

$712.00 flat

Preservation Fee in Lieu (Private Trees ≥12″ and <20″ DBH)

$1,888.00 per tree

Preservation Fee in Lieu (Private Trees ≥20″ DBH)

$472.00 per DBH inch

Most non-development applications (removal, replanting, pruning, etc.)

No charge

Selected fees from the FY 2025–26 Title 11 Trees Fee Schedule, highlighting the primary development mitigation rate ($472 per DBH inch) and non-development relief (most applications no charge).

A single 24-inch tree removed during development triggers approximately $11,328 in-lieu ($472 × 24). Multiple trees on infill lots commonly total $20,000–$50,000 or more.

These funds support equity-focused plantings—thousands of free yard and street trees in priority neighborhoods, as detailed in the FY 2023 Fund Report.

Cover of the Portland Urban Forest Plan Executive Summary (October 2025)—a vibrant collage highlighting community planting events, equity-focused tree giveaways, and the joyful stewardship that in-lieu mitigation fees help fund across Portland.

Enforcement and Penalties

Civil penalties reach $1,000 per tree per day, with restoration fees up to $944 per DBH inch for Heritage Trees (doubled for removal). Liens may be placed on the property.

For example, unauthorized removal of a typical 24-inch Heritage Tree could trigger restoration fees of approximately $22,656 ($944 × 24) plus daily penalties up to $30,000 over 30 days—potentially $50,000 or more in total liability.

Undisclosed prior violations—discoverable via Bureau of Development Services history—can impair marketability and would likely require an adjustment in appraised value.

Heritage Trees: Permanent Deed Encumbrance

Heritage Trees receive elevated protection due to age, size, historical association, or horticultural value. Common designations include Oregon white oaks, European beeches, London planes, and legacy Douglas-firs.

Private trees require owner consent for designation, but once recorded on the deed, the restriction binds all future owners. Removal or significant pruning typically requires City Council approval—a major encumbrance on development feasibility.

Nuisance Trees and Exemptions

Dead, dying, or officially listed nuisance species receive streamlined removal pathways. Certain small lots (<5,000 sq ft) and high-site-coverage scenarios carry lighter standards.

The 2025 Urban Forest Plan: Looking Ahead

Adopted October 22, 2025, the Plan sets ambitious canopy targets (citywide 45% in 40 years; every neighborhood ≥25%) and prioritizes equity in low-canopy areas. Community input emphasized preserving large trees while acknowledging burdens and calling for greater owner rights.

Recommendation #7 explicitly calls for improving City codes to support resilience and urban forest health—signaling Phase 3 Title 11 amendments may adjust preservation standards, mitigation, or incentives in coming years.

Takeaway: Navigating Portland’s Tree Code in Property Valuation

Portland’s urban forest remains one of its greatest assets—delivering shade, beauty, wildlife habitat, and environmental benefits across tree-lined neighborhoods and iconic parks like Forest Park and Mt. Tabor. Title 11’s preservation framework helps sustain this legacy, while mitigation fees fund equity-focused plantings that expand canopy in historically underserved areas.

Yet the code creates meaningful trade-offs for property owners. In resale transactions, mature trees often enhance market appeal and may support modest contributory value—evident in marketing frequency and observational signals from recent sales data. In redevelopment or major improvement scenarios, however, the same trees trigger mitigation costs, root protection constraints, and potential permanent encumbrances—shifting highest and best use and reducing land residual value.

Appraisers reconcile these dual realities through targeted due diligence. Portland Maps provides the tree inventory and Heritage layer for initial screening. Title reports (when available from lenders on purchase transactions) flag recorded Heritage designations. Bureau of Development Services permit history may require direct inquiry if redevelopment potential raises red flags—particularly on infill or teardown lots where prior violations or approved removals can materially affect feasibility. The free PDX Tree Map offers a quick view of city-managed street and park trees for neighborhood context, though private trees (the main Title 11 focus) are not included.

As the 2025 Urban Forest Plan unfolds—with its emphasis on preserving mature trees alongside calls for greater resident cost relief and owner rights—Phase 3 code amendments may refine these balances in coming years. Monitoring regulatory evolution will remain essential for accurate valuation in Portland’s tree-rich market.

Autumn foliage in a Portland park, exemplifying the seasonal beauty and character that mature trees contribute to the city’s residential and public spaces. Via Canva Pro.

PDX Tree Map (Portland public tree inventory viewer): Interactive Map

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

The Confederated Tribes of Grand Ronde’s $15.25 million 2019 acquisition of the contaminated former Blue Heron mill site at Willamette Falls exemplifies investment value and value-in-use, enabling a highest and best use shift stalled under prior ownership.

Willamette Falls in full cascade, with the former Blue Heron Paper Mill site in the midground. The dramatic natural setting contrasts sharply with decades of industrial obsolescence on the ~22-acre riverfront parcel. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)

The former Blue Heron Paper Mill site at Willamette Falls in Oregon City has long exemplified the valuation challenges posed by contaminated industrial brownfields. After the mill’s 2011 closure and subsequent bankruptcy, the ~22-acre riverfront parcel endured years of vacancy, burdened by functional obsolescence, deferred maintenance, and significant environmental liabilities that deterred conventional market participants.

In August 2019, the Confederated Tribes of Grand Ronde acquired the property for a recorded $15.25 million. This transaction stands out for appraisers as a clear illustration of investment value—the worth of a property to a particular purchaser based on individual motivations—and value-in-use, where non-economic factors such as cultural and ancestral significance justify a substantial premium over typical market indicators.

Panoramic view of the former Blue Heron mill complex along the Willamette River, with falls mist visible on the left. The sprawling structures illustrate extensive functional and external obsolescence following more than a decade of vacancy. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)

Site History and Market Perception

The property’s ownership and valuation history underscores the stagnation under conventional private ownership:

Year

Event

Recorded Price / RMV

2000

Acquired by Blue Heron Paper Company from Smurfit Newsprint Corp.

$2.5 million

2011

Mill closure and Chapter 11 bankruptcy filing

—

2014

Bankruptcy court sale to private developer (Falls Legacy LLC)

Clackamas County Real Market Value (post-acquisition)

~$3.6–$4.3 million (land-focused)

2021–2024

Phased demolition and remediation (approximately 40% of structures removed by 2024)

—

Recent

Oregon City master plan approval (GLUA240002)

—

Key ownership and valuation milestones for the ~22-acre former Blue Heron mill site, derived from Clackamas County public records and contemporaneous reporting. The lack of nominal appreciation from 2000 to 2014, followed by the substantial premium in 2019, highlights the impact of buyer-specific motivations.

Foreground view across derelict waterfront infrastructure at the former Blue Heron site, framed by graffiti-covered rail elements. The image captures visible signs of prolonged obsolescence and inaccessibility. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)Detailed view of cracked concrete pads and obsolete industrial remnants in the site’s foreground basin area. Such conditions exemplify brownfield liabilities common in post-industrial valuation. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)

Appraisal Implications—Investment Value and Value-in-Use

The $15.25 million purchase price—nearly seven times the 2014 bankruptcy sale and well above the assessor’s reported Real Market Value immediately preceding the transaction—reflects investment value driven by the Tribe’s profound cultural connection to Willamette Falls, a sacred ancestral homeland and traditional fishing ground. This non-economic value-in-use enabled the Tribe to overcome remediation and holding-cost barriers that had stalled private redevelopment efforts for years.

Appraisers reconciling such sales must distinguish investment value (or value-in-use) from market value derived from arms-length transactions among typical participants. Limited comparable sales for culturally significant or heavily contaminated riverfront parcels often require significant adjustments for buyer motivation, extraordinary assumptions regarding cleanup feasibility, and bracketing with more conventional industrial land comps.

This situation parallels a more recent Portland case explored on this blog: the 1803 Fund’s adaptive reuse plans for historic grain silos along the Willamette River. In both instances, a buyer with specific motivation recognized potential in a functionally obsolete industrial asset that had deterred conventional market participants—ultimately enabling a highest and best use shift through targeted redevelopment.

Intimate perspective on remaining mill buildings, showing moss-covered roofs, rust, broken windows, and heavy graffiti—clear evidence of functional obsolescence after years of vacancy. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)

Current Progress and the Tumwata Village Vision

Recent site visits confirm active transformation: demolition equipment, including excavators, is visibly engaged in clearing remaining structures.

Phased demolition began in 2021, with multiple rounds completed by 2024 removing approximately 40% of the former mill buildings. Remediation continues in coordination with state and federal environmental agencies.

A major fire in January 2025 destroyed one of the larger remaining buildings on the site (the former mill’s three-story structure). The incident, ruled arson and unrelated to demolition activities, did not delay the overall redevelopment timeline. Progress has continued steadily, as evidenced by recent infrastructure planning and the current state of the property.

Renamed Tumwata Village, the redevelopment proposes a mixed‑use cultural district that weaves together public access trails, ecological restoration of the riverbank and lagoon, tribal gathering spaces, and a modest mix of commercial and hospitality uses—all grounded in the site’s ancestral significance. By prioritizing riverfront restoration and new trail connections, the plan could open up rare land‑based vantage points of Willamette Falls, a natural landmark that today is mostly viewed from commercial boat tours or distant overlooks. If fully realized, the transformation would support the Confederated Tribes of Grand Ronde in cultural reclamation and long‑term stewardship, while giving Oregon City and the broader public renewed access to a stretch of the falls long closed off by industrial operations.

Oregon City’s recent approval of the master plan (GLUA240002) formalizes this highest and best use shift from interim speculative hold to culturally driven redevelopment.

Readers interested in detailed conceptual plans and site renderings can review the Tribe’s 2022 design report.

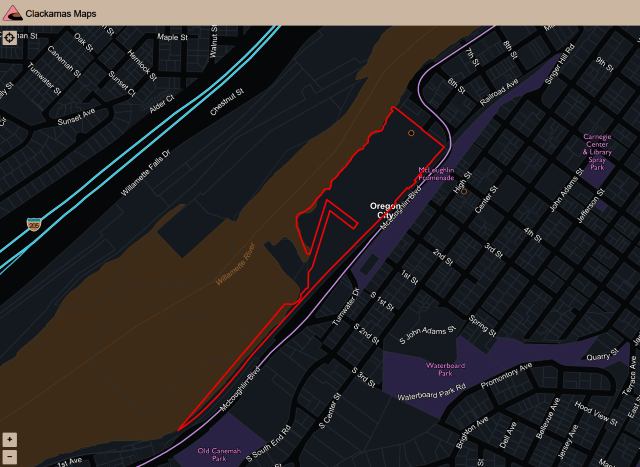

Mid-demolition scene at the site, with construction equipment including an excavator and partially cleared areas visible. Ongoing remediation phases demonstrate the reversal of obsolescence through active transformation. Photo: Abdur Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)Clackamas County GIS overview of the ~22-acre former Blue Heron mill site (red outline), illustrating its extensive Willamette River frontage and proximity to the falls. The contiguous parcel configuration supports comprehensive redevelopment potential. Source: Clackamas County Maps.

Takeaway

The Tumwata Village acquisition serves as a compelling case study in investment value and value-in-use. When a purchaser’s motivations—here rooted in cultural reclamation—align with a property’s unique attributes, transaction prices can far exceed indicators derived from conventional market behavior. Appraisers must remain alert to these distinctions, employing careful reconciliation techniques and appropriate adjustments when comparable data is limited.

Ultimately, the project illustrates how buyer-specific utility can reverse long-standing obsolescence, shifting a site’s highest and best use in ways the open market alone could not achieve. If realized, the vision promises not only tribal stewardship of ancestral lands but also broader public access to one of Oregon’s most iconic natural features—offering land-based and proximate views of Willamette Falls where few currently exist.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}