At today’s 6.49% mortgage rate, the monthly principal‑and‑interest payment on a Q1 2026 Portland Region median-priced detached home ($580,000) with 20% down is $2,930, up from $2,776 at February’s low. Lifetime interest rises to $590,708, and repricing all Q1 loans at today’s rate adds $156M in regional interest.

What Happened This Week

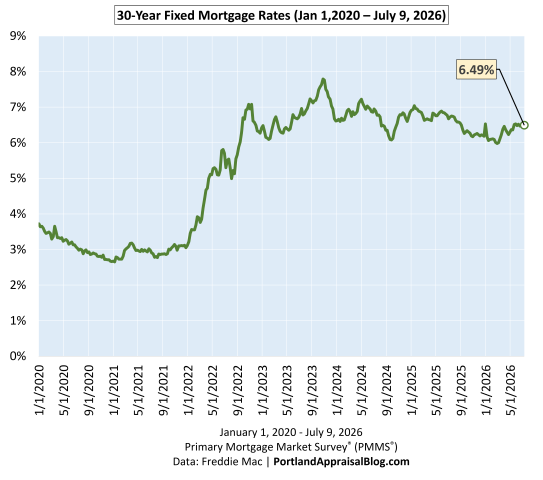

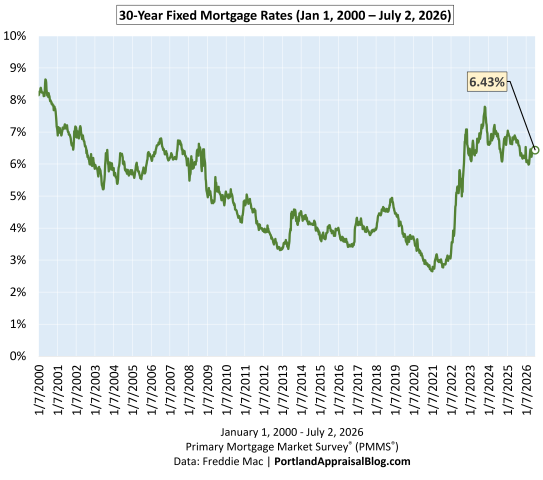

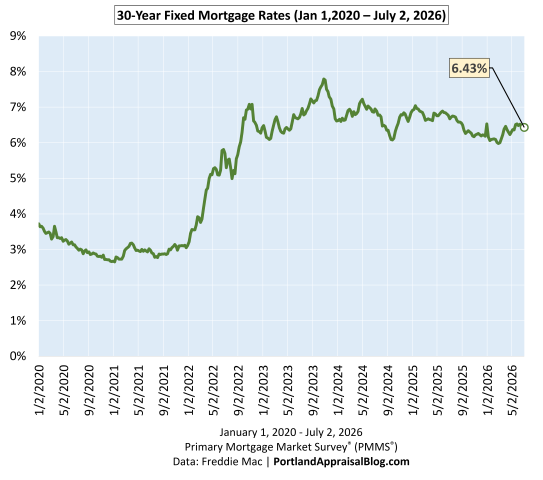

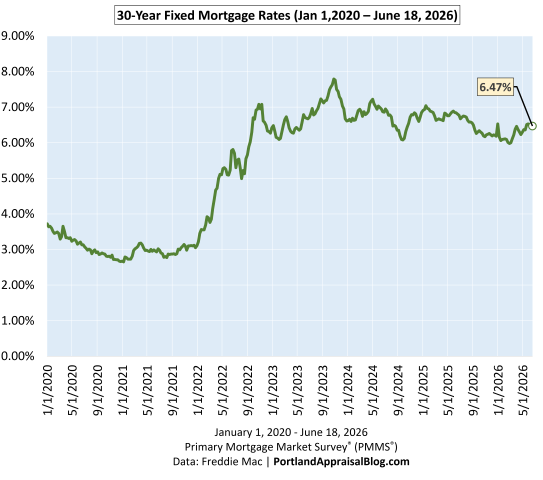

Mortgage rates moved higher this week, with the 30‑year fixed returning to 6.49%—a 6 bps increase from last week and sitting very close to the year‑to‑date highs. The broader 2026 pattern remains intact: rates bottomed on February 26th, climbed sharply through early April, cooled briefly, and then resumed their upward drift beginning April 23. With this week’s move, we remain near the top of the 2026 range, and the past seven weeks have been defined by a narrow, high‑pressure band of rate movement that had been drifting downward but snapped upward this week, breaking the short‑term pattern.

Affordability remains strained at these elevated levels. A 6 bps increase carries weight when rates are this high, and monthly payments continue to hover near their most challenging point of the year. As the charts below show, today’s rate sits just under the ceiling of the year‑to‑date range, and the PABAI continues to reflect the compounding affordability pressure facing buyers across the Portland Region.

Mortgage Rate Context

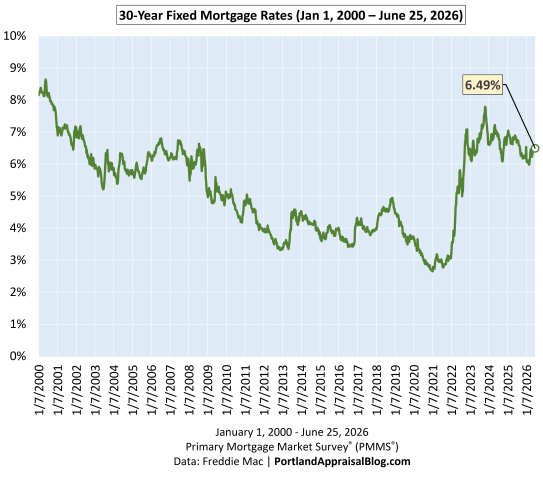

Long‑Run View (Since 2000)

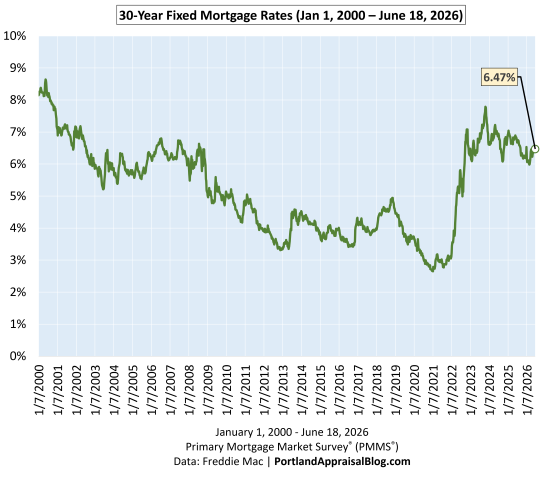

The long‑run chart shows how today’s rate fits into a 25‑year history of mortgage cycles. The early 2000s sat in the 6–8% range, the post‑Great Recession era brought a decade of unusually low rates, and the pandemic period pushed borrowing costs to historic lows. Years after leaving that ultra‑low‑rate environment, the market continues to adjust to more difficult financing constraints, and today’s 6.49% reflects that ongoing shift. With this week’s jump, rates remain elevated in a long‑term context, and affordability continues to be shaped by the same structural pressures highlighted in the medium‑run and short‑run views.

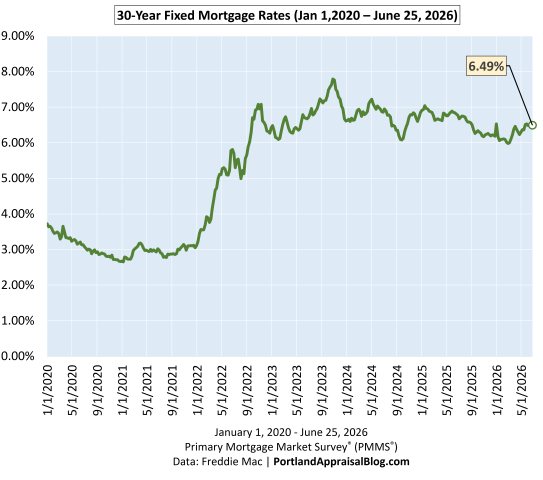

Medium‑Run View (Since COVID)

The COVID‑era chart highlights the dramatic rate compression of 2020–2021, the rapid surge of 2022, and the choppy plateau that has defined the past two years. Rates have been oscillating between roughly 6% and 7% since mid‑2023, and today’s 6.49% sits near the middle of that band. Volatility has cooled compared to 2022, but the medium‑run trend remains one of elevated and persistent borrowing costs, with the market continuing to adjust to structurally higher financing conditions across the Portland Region.

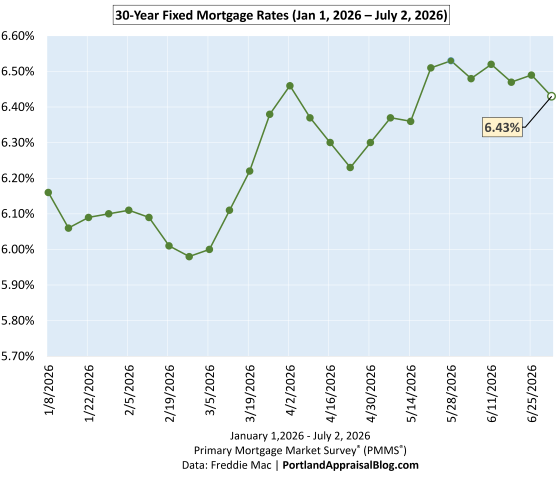

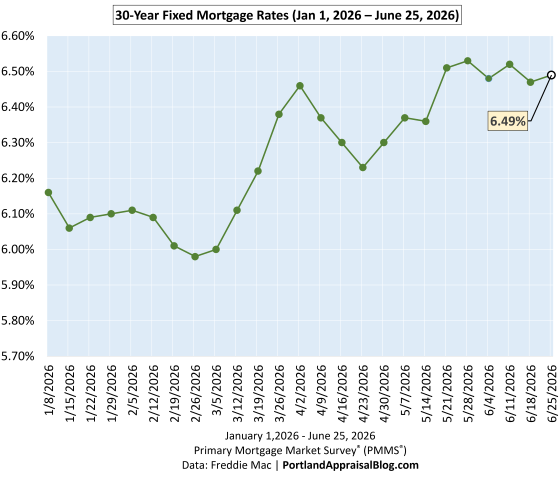

Short‑Run View (2026 YTD)

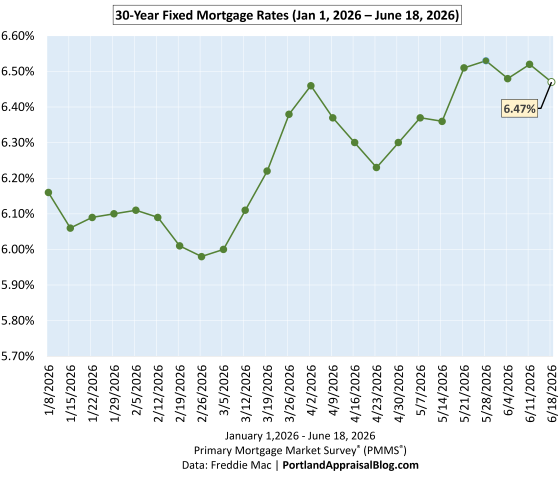

The year‑to‑date chart shows the full shape of the 2026 cycle: a clear bottom at 5.98% on February 26th, a sharp rise into early April, a brief cooldown, and a renewed climb that pushed rates to 6.53% in late May—the highest level of the year. This week’s reading of 6.49% brings us just below that peak, and affordability remains near its weakest point of 2026. This short‑run pattern is the most relevant for buyers today, as it directly shapes monthly payments and qualifying power across the Portland Region.

Portland Appraisal Blog Affordability Index (PABAI)

What PABAI Measures

The Portland Appraisal Blog Affordability Index (PABAI) measures how home close prices compare to what a median‑income household can qualify for under standard lending assumptions (HUD Portland‑Vancouver‑Hillsboro MSA median income, 20% down, and a 28% DTI for principal, interest, taxes, insurance, and HOA dues).

Unlike national affordability indices, PABAI is built from actual RMLS transactions rather than a single hypothetical price point. It computes an affordability ratio for every closed sale in the Portland Region during Q1 2026 and then averages those results—that average is the reported PABAI. Each housing segment—detached, attached, condos, and manufactured—is calculated separately, ensuring that segment‑specific dynamics are preserved rather than blended together. This approach produces far more precise, locally grounded insights into Portland‑area affordability and avoids the distortions that occur when fundamentally different housing types are combined into a single regional metric.

A PABAI of 100 means the market is exactly affordable at that income level (the Q1 2026 HUD median MSA income was $124,100 for a family of four). Values above 100 indicate excess qualifying capacity (more affordable), while values below 100 indicate a shortfall (strained affordability). Full methodology and the interpretation scale are available on the PABAI explainer page.

PABAI Range

Interpretation

120+

Strongly Affordable

100–119

Moderately Affordable

80–99

Strained

Below 80

Severely Constrained

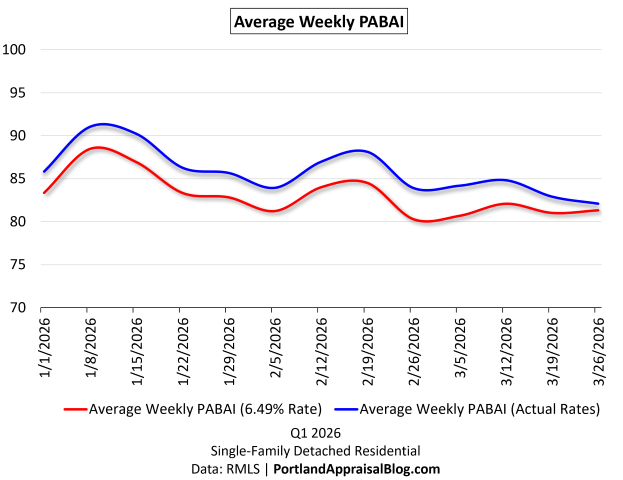

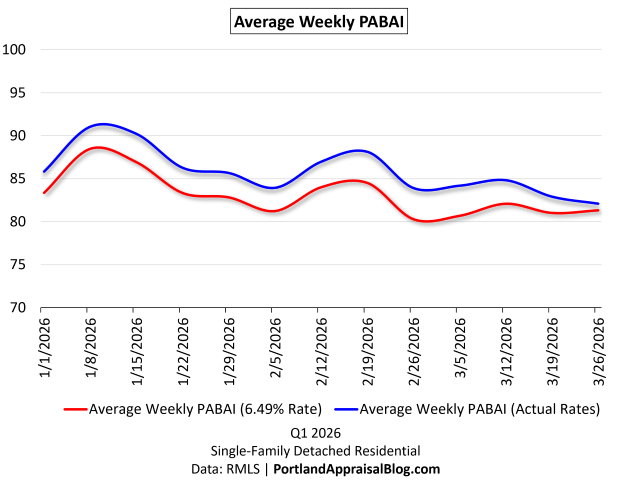

Q1 2026: Actual vs. Constant‑Rate Affordability

The Q1 chart compares two versions of PABAI: one using actual weekly mortgage rates, and one using today’s rate (6.49%) as a constant. Because the constant‑rate line uses a rate near the top of the 2026 range, it naturally sits below the actual‑rate line for most of the quarter. That part isn’t the story.

The key insight is the size and behavior of the gap between the two lines. Early in the quarter, actual rates were meaningfully lower than today’s 6.49% level, giving buyers more qualifying power than a flat‑rate environment would suggest. But as rates climbed through March and into April, the two lines began to converge—a visual confirmation of how persistent rate increases eroded affordability heading into spring. Today’s 6.49% rate keeps the constant‑rate line very close to the actual‑rate line at the end of Q1, reflecting the tightening affordability conditions that carried into mid‑ and late‑spring across the Portland Region.

Structural Unaffordability and the Seasonal Pattern

Detached homes in the Portland Region remain structurally unaffordable to a household earning the HUD median MSA income. PABAI has been below 100 for years, and Q1 2026 continues that pattern. What the chart makes clear is that winter remains the best window for buyers on tight qualifying budgets: affordability improves when rates soften and seasonal pricing cools. As spring approaches, both rates and prices firm up, and affordability reliably compresses.

With the 30‑year fixed now sitting near the highest levels of 2026, the convergence of the two PABAI lines at the end of the quarter reflects the same reality: rising rates have pushed qualifying costs to their weakest point of the year, and the early‑year affordability advantage has largely evaporated. Today’s 6.49% reading keeps affordability firmly in the strained range, underscoring how sensitive the market remains to even small rate movements.

Affordability Snapshot (This Week)

Q1 2026 Affordability Recomputed at Today’s Rate

The table below shows how Q1 2026 affordability metrics change when all 3,349 detached sales are recalculated at this week’s 6.49% rate. This is the clearest way to see how rising rates reshape qualifying power, housing burden, and the share of homes accessible to a median‑income household.

Because today’s rate sits near the top of the 2026 range, the recomputed metrics show a meaningful deterioration in affordability relative to the actual Q1 environment. Required income rises, housing burden increases, and the number of homes affordable to a median‑income household falls sharply—a direct reflection of how even small rate increases compound at elevated levels.

Taken together, these metrics show how quickly affordability erodes when rates rise into the mid‑6% range. The drop in Average PABAI from 85.45 to 82.69 may look modest at first glance, but it represents a meaningful tightening of qualifying power across the entire detached market. Required income rises to roughly $150,100, widening the gap between what a median‑income household earns and what the market demands. That shortfall now approaches 21%, a reminder that the typical Portland household remains well outside traditional affordability thresholds defined in the PABAI framework.

The payment side tells the same story. Recomputing Q1 sales at today’s rate pushes the average monthly mortgage obligation up by about $130, which may seem incremental on a monthly basis but compounds sharply over a 30‑year horizon. More importantly, the higher rate pushes the average front‑end DTI from 38.03% to 39.28%, a level that would be considered stretched even in more forgiving underwriting environments. These shifts are not abstract; they directly shape who can buy, what they can buy, and how competitive they can be in the Portland Region.

The Buyer‑Side Impact

The most visible consequence of these changes is the shrinking pool of homes accessible to a median‑income household. Under actual Q1 2026 rates, 967 detached homes were affordable; at today’s 6.49% rate, that number falls to 844. In percentage terms, the share of the market within reach drops from 28.9% to 25.2%—a loss of over three and a half percentage points in a single recalculation. This is the practical expression of rising rates: fewer viable options, tighter qualifying margins, and a market that becomes increasingly selective about who can participate.

For buyers, the experience varies by circumstance but the direction is the same. Households with limited flexibility feel the tightening most acutely, as even small rate movements can eliminate entire segments of the market. Move‑up buyers face a widening payment gap between their current home and the next one, making the trade‑up calculus more difficult unless equity is substantial. Cash buyers, by contrast, gain relative leverage as financed demand thins—though that advantage is uneven across price tiers.

Across all buyer types, the message is consistent: rising rates are reshaping the market in real time, and the affordability landscape at a 6.49% mortgage rate is meaningfully different from the one buyers faced just a few months ago. The shift is incremental week to week, but cumulative in effect—a defining feature of today’s strained affordability environment.

The Seller‑Side Impact

Rising rates don’t just reshape the buyer experience—they influence seller outcomes as well. In the Q1 2026 detached market, cumulative days on market (CDOM) increased 11.27%, and the current rate environment suggests that upward pressure on market times may persist. As affordability tightens and the pool of qualified buyers shrinks, homes that would have moved quickly in a lower‑rate environment may begin to sit longer, particularly in segments where pricing is already stretched.

Today’s 6.49% rate keeps financing conditions near the most challenging levels of 2026, reinforcing the same dynamic: fewer qualified buyers, more selective demand, and a market where pricing precision matters. This doesn’t imply an abrupt market slowdown, but it does mean sellers should expect a more deliberate buyer pool and prepare for longer market times—especially in higher‑priced tiers where rate sensitivity is most acute.

TIP: Total Interest Paid — Why Small Rate Moves Matter

Total Interest Paid (TIP) is one of the clearest ways to understand how mortgage rates shape long‑run affordability. While buyers shop based on monthly payment, the lifetime cost of borrowing moves far more dramatically than the payment itself. Even small rate changes can add—or remove—tens of thousands of dollars in interest over the life of a loan.

At today’s 6.49% rate, the lifetime interest on a standard Portland‑area purchase sits far above the levels buyers saw during the pandemic and meaningfully higher than the early‑March lows of this year. The difference between a 5.98% environment and a 6.49% environment may feel subtle on a monthly basis, but over 30 years it compounds into a substantial increase in total repayment—the kind of shift that materially affects long‑run household finances in the Portland Region.

This is why TIP matters: it captures the hidden cost of rising rates. Buyers feel the payment, but the long‑run financial burden is embedded in the interest curve. As the charts below show, the 2026 rate path has pushed TIP to some of the highest levels of the year, even as the monthly payment has moved more gradually. The cumulative effect is what reshapes affordability—a dynamic that becomes especially clear when comparing TIP across different rate scenarios.

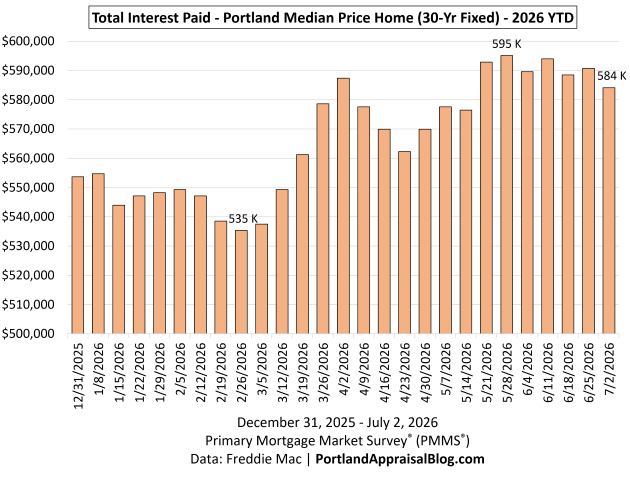

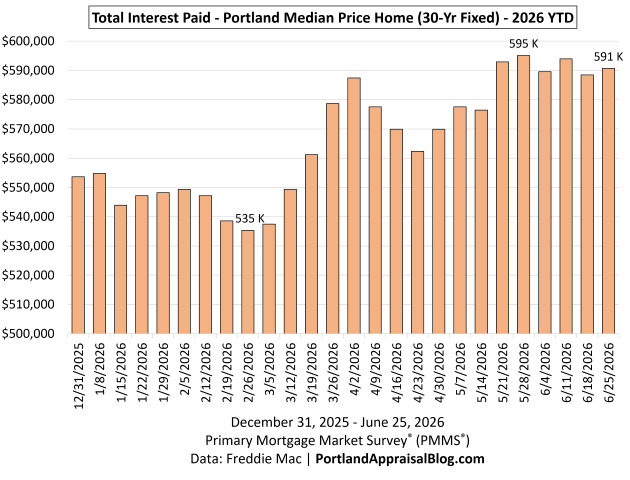

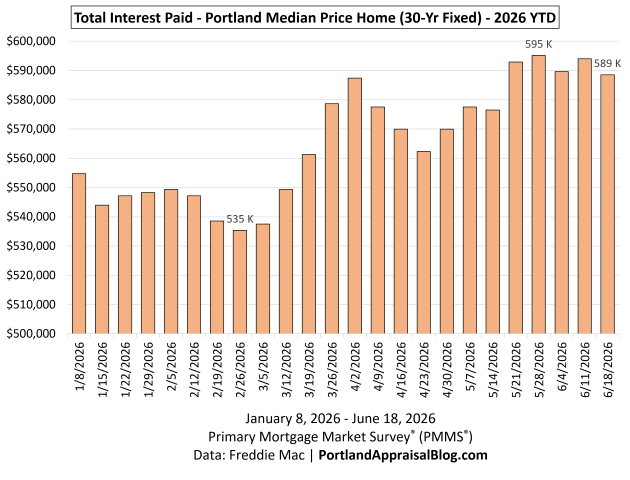

2026 YTD Total Interest Paid

Note: The y-axis starts at $500,000 to allow better examination of monthly differences.

The 2026 YTD TIP chart shows how sharply lifetime borrowing costs have moved as rates climbed through the first half of the year. These calculations are based on the total interest a buyer would pay on the Q1 2026 Portland median‑priced home of $580,000, assuming a 20% down payment and applying the rate effective in each week. This isolates the impact of rate movements alone, holding price and loan structure constant.

The low point came on February 26th, when a 5.98% mortgage rate produced a total interest burden of $535,342. As rates rose through March and into late May, TIP increased steadily, reaching a year‑to‑date high of $595,104 at the 6.53% rate on May 28th—a swing of nearly $60,000 in lifetime interest in just three months, driven entirely by rate movement.

This week’s 6.49% rate pulls TIP down slightly from the YTD high: the total interest burden at today’s rate is $590,708, a modest improvement but still among the highest readings of the year. The shape of the chart makes the pattern unmistakable—at today’s price levels, even small rate changes translate into large long‑run cost differences. Buyers feel the monthly payment, but the lifetime interest curve is where the true financial impact of rising rates becomes visible, especially when comparing TIP across different rate environments.

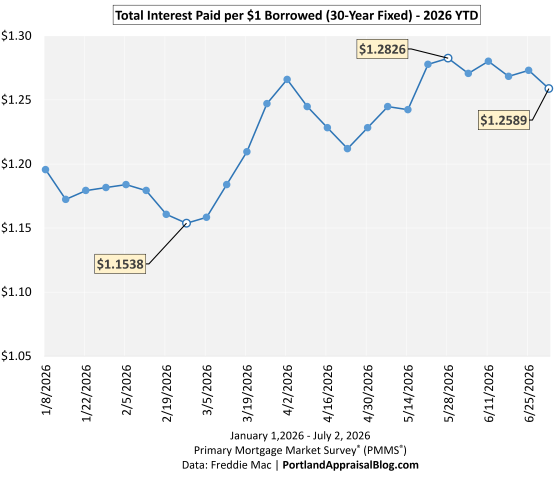

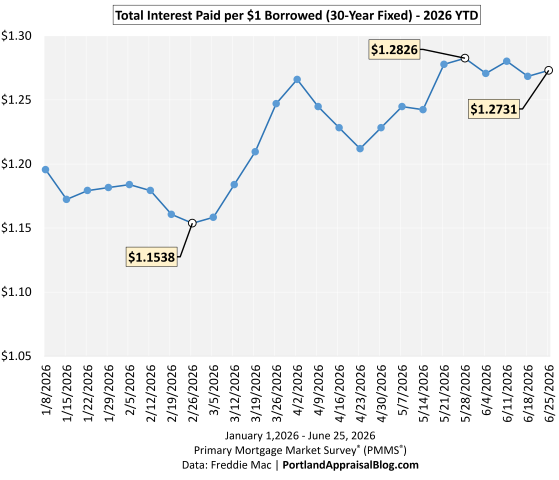

TIP per $1 Borrowed

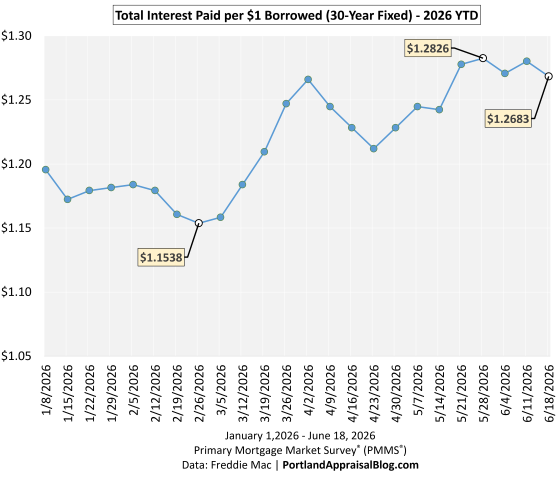

The TIP‑per‑$1 chart shows how much interest a buyer pays for every dollar borrowed at different mortgage rates. This is the clearest way to visualize the rate sensitivity of long‑run borrowing costs. At the year‑to‑date low of 5.98%, each dollar borrowed generated about $1.1538 in interest over the life of the loan. As rates climbed through the spring, that figure rose steadily, reaching $1.2826 at the late‑May peak of 6.53%.

Today’s 6.49% rate places the cost at $1.2731 per $1 borrowed, a slight improvement from the peak but still near the highest levels of the year. The line makes the pattern clear: once rates move into the mid‑6% range, each additional uptick adds meaningfully more lifetime interest—a dynamic that becomes especially clear when comparing rate environments side by side.

Regional Interest Delta (RID)

The Regional Interest Delta (RID) models how much total lifetime interest the Portland Region’s Q1 detached‑home buyers would collectively pay when mortgage rates shift. To keep the metric consistent, RID assumes that all 3,349 Q1 detached sales were financed under standard 20%‑down, 30‑year conventional underwriting, even though the actual dataset includes cash purchases and loans under FHA, VA, jumbo, and other programs. Rates are matched to each home’s close date to reflect the real timing of rate movements, but individual buyers may have locked slightly different rates depending on their specific loan terms. This approach provides a clean, apples‑to‑apples way to measure how rate changes affect the region’s total interest burden.

Using those actual matched rates, the region’s Q1 2026 pipeline will generate $2,091,901,976 in lifetime interest. Recomputing the same loans at today’s 6.49% rate increases the total to $2,248,407,532. The difference—the RID—is $156,505,556 in additional lifetime interest.

To put that number in perspective: the hollywoodHUB affordable‑housing development cost roughly $152 million to build. A single rate shift—applied across one quarter’s mortgage activity—now produces a lifetime interest delta exceeding the scale of a major regional housing project. This week’s RID represents a nine‑figure increase in long‑run borrowing costs driven solely by rate movement.

RID makes the scale of rate changes unmistakable. What looks like a modest shift at the household level becomes a region‑wide financial impact when applied across thousands of loans—a reminder of how sensitive the Portland market remains to even small movements in the 30‑year fixed.

Payment Delta

The Payment Delta shows how monthly affordability shifts as mortgage rates move. Using the Q1 2026 Portland median‑priced home of $580,000 with a 20% down payment, the monthly principal‑and‑interest payment changes meaningfully even with small rate movements.

Date

Rate

Monthly P&I

Pmt Delta

Feb 26, 2026

5.98%

$2,775.95

—

May 28, 2026

6.53%

$2,941.96

$166.01

July 9, 2026

6.49%

$2,929.74

$153.79

Payment Delta reflects the change from the year‑to‑date low on February 26. Monthly payment for home using median Q1 2026 price ($580,000) and 20% down. Primary Mortgage Market Survey® (PMMS®) Data: Freddie Mac | PortlandAppraisalBlog.com

From the YTD low to the late‑May peak, the monthly payment increased by about $166, and today’s payment remains nearly $154 higher than the February low.

While the Payment Delta is smaller in scale than the lifetime interest changes shown in TIP and RID, it is the number buyers feel most immediately. For households shopping at the lower end of the market, even a $150–$175 shift can meaningfully affect qualifying ratios, required down payment, or even which housing types remain viable—such as moving from detached homes to attached or condos. These adjustments often matter more for affordability‑sensitive buyers than for the broader market.

Closing Thoughts

The story of this week is straightforward: mortgage rates remain elevated, and the effects are visible across every major affordability metric. The PABAI continues to signal structural strain for median‑income households, and the recalculated Q1 data shows how even modest rate movements reshape qualifying power, monthly payments, and the share of homes within reach. The TIP and RID visuals make the pattern clear: higher rates don’t just affect individual buyers—they reshape the long‑run financial burden carried across the entire region.

For buyers, the takeaway is that financing conditions remain tight as we move into early summer. Winter continues to offer the best affordability window, but today’s rate environment means households on the margin feel pressure sooner and more sharply than in prior years. Even a $150‑range shift in the Payment Delta can influence qualifying ratios, required down payment, or which housing types remain viable—including whether buyers need to consider attached homes or condos instead of detached options.

For sellers, the implications are more subtle but no less real. The Q1 2026 detached market saw CDOM rise more than 11%, and the current rate backdrop suggests that upward pressure on market times may persist. A smaller pool of qualified buyers and higher monthly payments can translate into longer exposure, especially for homes priced aggressively or positioned in segments where affordability is already stretched. Pricing discipline and realistic expectations matter more in this environment than they did during the ultra‑low‑rate era.

As always, the Portland market adapts—sometimes quickly, sometimes reluctantly—but the direction of travel is clear. Higher rates are reshaping both sides of the transaction, and the early summer of 2026 is operating under some of the most constrained financing conditions we’ve seen this year.

Sources & Further Reading

All data presented in this weekly mortgage rate update is based on the Q1 2026 detached homes segment. The data is sourced directly from RMLS and has been subjected to rigorous cleaning and validation processes to ensure reliability for detached single-family residential analysis in the six-county Portland Region. The trends, comparisons, and commentary are the result of original appraisal expertise and independent analysis—not aggregated from secondary sources or news summaries.

Freddie Mac Primary Mortgage Market Survey® (PMMS®): Dataset

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Q1 2026 Portland Region condo update: average price $389k (+6.5%), median $325k (‑1.5%), sales 511 (‑8.6%), CDOM 119 days (+8%). Dollar volume dipped 2.6% as new construction fell sharply, yet still reached $199M. County trends diverged, and Ritz‑Carlton closings—after a year of no activity—kept the market from sliding further.

The City of Portland skyline with Mt. Hood in the distance. Via Canva Pro

The condo market entered 2026 on softer footing, with sales and dollar volume both slipping from last year’s pace. Activity was steady enough to keep the segment functional, but not strong enough to overcome the broader contraction. What complicated the picture was the renewed momentum at the Ritz‑Carlton Residences, which re‑emerged this quarter as a major force in the luxury segment. That revival reshaped the composition of what sold and kept the quarter from appearing weaker on the surface than the fundamentals alone would suggest.

The Ritz accounted for 60% of all $1M‑and‑up closings, and that concentration was enough to push average prices higher even as the rest of the market softened. Median prices, price‑per‑square‑foot, and total dollar volume all declined, reflecting a quieter underlying market. But the surge in luxury‑tower activity created a split narrative: the averages moved one way, the fundamentals another. It was a quarter defined less by broad price movement and more by what sold and where those sales occurred.

Affordability technically improved this quarter, and condos remain the most accessible segment for a median‑income household. But that improvement came from lower mortgage rates, not from dramatic changes within the condo market itself. Rising HOA dues continue to be a structural drag, and the segment’s geographic concentration limits its appeal. Many buyers still prefer detached homes with yards, and many prefer suburban or rural settings where condos are scarce or nonexistent. In that sense, condos remain affordable but not a panacea—an option that works well for some buyers, but not a broad solution to the region’s housing pressures.

The Portland Region in this update comprises the six Oregon counties of Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill. These counties form a contiguous housing ecosystem centered on Portland—Multnomah as the core home county, with the others tightly integrated through commuting patterns, economic ties, and shared market dynamics (e.g., Yamhill’s strong connection via Highway 99W and wine-country adjacency). Beyond Yamhill, the MLS system changes, further distinguishing this six-county area from broader geographic aggregations. For a detailed overview—including county profiles, population data, key value influencers, and why this definition differs from the official seven-county Portland–Vancouver–Hillsboro MSA—see the dedicated page: The Portland Region – Six-County Market Area Overview.

All data is sourced from RMLS and reflects open-market condominium residential sales. SNL (“Sold Not Listed”) entries—off-market transactions entered retroactively—have been excluded to preserve consistency with true market activity.

Since condominium is an ownership type and not necessarily a description of style, a strict examination was made of all other major single-family housing types in RMLS (detached homes, attached homes, and manufactured homes on owned land) and any condominium sales found in those segments were aggregated into this review. All figures underwent standard cleaning to address common RMLS accuracy challenges, including square footage/price typos, incomplete fields, status/date mismatches, and non-representative entries. For a detailed overview of these issues, their impact on market analysis, and mitigation through automated flagging, cross-verification, and manual review, see the dedicated page: RMLS Data Accuracy Challenges.

Portland Appraisal Blog Affordability Index (PABAI)

What PABAI Measures

The Portland Appraisal Blog Affordability Index (PABAI) is a model that estimates how home sale prices compare to what a median‑income household can qualify for under standard lending assumptions (HUD Portland‑Vancouver‑Hillsboro MSA median income, 20% down, and a 28% DTI for principal, interest, taxes, insurance, and HOA dues).

Unlike national affordability indices, PABAI is built from actual RMLS transactions rather than a single hypothetical price point. It computes an affordability ratio for every closed sale in the Portland Region during the analysis period using rates matched to the date of close, reported taxes, reported HOA dues, and an insurance estimate based on a percentage of the home’s value. The individual affordability ratios are then averaged to produce the reported PABAI value for that period. For Q1 2026, this approach captures the actual mix of homes sold and the financing conditions present at the time those transactions occurred. Each housing segment—detached, attached, condos, and manufactured—is calculated separately, ensuring that segment‑specific dynamics are preserved rather than blended together. This approach provides a more detailed, locally grounded view of Portland‑area affordability and avoids the distortions that occur when fundamentally different housing types are combined into a single regional metric.

A PABAI of 100 means the market is exactly affordable at that income level (the Q1 2026 HUD median MSA income was $124,100 for a family of four). Values above 100 indicate excess qualifying capacity (more affordable), while values below 100 indicate a shortfall (strained affordability). Full methodology and the interpretation scale are available on the PABAI explainer page.

PABAI Range

Interpretation

120+

Strongly Affordable

100–119

Moderately Affordable

80–99

Strained

Below 80

Severely Constrained

Residential Housing Snapshot

Category

Detached

Attached

Condo

Manuf.

Total $ Volume

$2.2B

$161.0M

$199.0M

$32.4M

Avg Price

$659,197

$444,672

$389,438

$540,352

Avg PPSF (Total SF)

$316.21

$286.91

$325.55

$356.75

Avg Total SF

2,164

1,576

1,180

1,571

Avg Lot Size (ac)

0.655

0.066

N/A

7.959

Avg Age (Yrs)

46.03

15.09

32.03

29.10

Avg CDOM

80.22

80.59

119.62

118.25

# of Sales

3,349

362

511

60

% of Market

78.21%

8.45%

11.93%

1.40%

Highest Sale

$5,725,950

$1,175,000

$2,450,000

$2,400,000

Lowest Sale

$135,000

$249,000

$100,000

$199,700

Price Spread Ratio

42.41

4.72

24.50

12.02

PPSF Spread Ratio

30.93

4.08

11.91

13.29

Total SF Spread Ratio

23.46

4.14

12.24

3.52

Avg PABAI

85.45

110.38

122.83

118.04

Q1 2026 (4,282 total residential sales). Data: RMLS | PortlandAppraisalBlog.com

The Portland Region’s residential market remains anchored by detached homes, which continue to define the overall structure of housing activity in Q1 2026. Detached properties account for the vast majority of open‑market sales and dollar volume, and they remain the least affordable segment with a PABAI well below 100. They also sit on the most land, offer the largest average dwelling size, and span the widest range of product types—from sub‑$150,000 fixers to multi‑million‑dollar estates. Their internal diversity and land intensity shape much of the region’s pricing landscape, and they remain the segment most buyers prefer even when affordability pushes them elsewhere.

Attached homes serve as the clearest alternative when detached becomes harder to access. They are the youngest and most uniform segment, with tight spread ratios and predictable pricing that make them the region’s most “commodity‑like” housing type. Their moderate affordability and consistent product profile position them as the safety‑net entry point for buyers priced out of detached homes. Manufactured homes and condos share several surface‑level similarities—age, CDOM, affordability, and even price ceilings—but diverge sharply in how they trade. Manufactured homes trade on land, while condos trade on HOA dues, the hidden variable that shapes their affordability profile and increasingly picks winners and losers within the segment.

Condos remain the most affordable segment in the region, with a PABAI nearly at 123 this quarter, but affordability alone does not translate into broad appeal. Many buyers prefer detached homes with yards, and many prefer suburban or rural settings where condos are scarce or nonexistent. Others deliberately avoid homeowners associations and their attendant dues and rules, regardless of price point. Condos also represent a relatively small share of the region’s housing activity: they make up roughly 12% of all Q1 sales but contribute less than 8% of total dollar volume. Given their lower prices compared to detached homes, this gap is expected and reflects the structural role condos play in the ecosystem—an accessible option for some buyers, but not a proportional driver of regional dollar volume.

Three of the four residential segments cluster in the low–mid $300s PPSF, underscoring that structure cost is relatively consistent across the metro; it is land, size, dues, and buyer preferences that create the separation between segments. Spread ratios help illustrate this internal variation by comparing the highest and lowest values within each segment—higher ratios indicate a wider spectrum of product types and price points, while lower ratios signal a more uniform, commodity‑like segment. Detached homes show the widest internal variation, attached homes the tightest, and condos a bimodal profile shaped by older stock on one end and boutique new construction and luxury towers on the other. This ecosystem context sets the stage for the condo‑specific analysis that follows.

Portland Region Q1 2026 Overview

Overall Regional Trends

The table below summarizes key metrics for condominium residential sales in the Portland Region (Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill counties) for Q1 2026 compared with Q1 2025.

Category

Q1 2025

Q1 2026

Change

Total $ Volume

$204.3 Million

$199.0 Million

-2.61%

Average Price

$365,524

$389,438

+6.54%

Median Price

$329,900

$325,000

-1.49%

Avg SP/OLP

94.66%

92.88%

-1.88%

Avg PPSF (TSF)

$335.68

$325.55

-3.02%

Avg HOA Dues

$458.84

$586.72

+27.87%

Median HOA Dues

$422.00

$482.00

+14.22%

Avg Age (Yrs)

27.58

32.03

+16.10%

Avg CDOM

110.76

119.62

+7.99%

Avg Total SF

1,111

1,180

+6.21%

Total # of Sales

559

511

-8.59%

# of New Constr.

144

97

-32.64%

# of REOs

8

13

+62.50%

# of Short Sales

1

3

+200.00%

Average PABAI

113.92

122.83

+8.91 pts

# Affordable

351

355

+4 units

% Affordable

62.79%

69.47%

+6.68 pts

Note: The calculated average HOA dues is for sales reporting nonzero HOA dues (547 sales for Q1 2025 & 491 sales for Q1 2026). All other metrics use the full dataset for each quarter. Condominium Residential | Q1 2025 & Q1 2026 Data: RMLS | PortlandAppraisalBlog.com

Key Observations From the Aggregate Data

The overall condo market contracted in Q1 2026, with total sales down 8.6% and total dollar volume slipping 2.6% from last year. Median price and PPSF both declined, reflecting softer underlying conditions, and marketing times lengthened as buyers remained deliberate. Yet average price rose 6.5%—a paradox explained not by broad appreciation, but by what sold. The revival of the Ritz‑Carlton Residences reshaped the quarter’s composition, lifting the averages even as the fundamentals moved in the opposite direction.

The Ritz accounted for 60% of all $1M‑and‑up closings, and that concentration alone was enough to shift the quarter’s pricing profile. But the luxury segment was stronger even beyond the Ritz: the region recorded more $1M+ condo sales this year than last, contributing to the rise in average price and the increase in average unit size. Without this luxury‑tier activity, the quarter would have shown a more pronounced decline in averages. Instead, the data reveal a split narrative—averages up, fundamentals down—driven almost entirely by composition.

HOA dues surged this quarter, with average dues rising nearly 28% and median dues up 14%. Part of this increase reflects the luxury‑tower mix: Ritz units carry some of the highest dues in the region, and their reappearance in the dataset pulled the average upward. But the rise in median dues shows that the trend extends beyond any single building. Insurance costs, reserve requirements, and aging infrastructure continue to push dues higher across the region, reinforcing the role of HOA dues as a structural drag on the segment and a key factor in picking winners and losers among condo complexes.

Affordability improved meaningfully, with PABAI rising from 113.92 to 122.83, making condos the most accessible segment for a median‑income household. This improvement wasn’t just theoretical: the number of condos affordable to a median‑income household rose from 351 to 355, even as total sales declined. Over two‑thirds of all condos sold in Q1 2026 were affordable under standard underwriting assumptions. But this improvement was rate‑driven, not price‑driven. Lower mortgage rates expanded buying power, while rising dues offset part of that gain. Condos remain objectively affordable, but affordability alone does not broaden demand—many buyers prefer detached homes, suburban settings, or simply wish to avoid homeowners associations and their attendant dues and rules, regardless of price point.

The market also slowed further, with CDOM rising nearly 8% and the average age of sold units increasing from 27.6 to 32.0 years. New‑construction closings fell by one‑third, consistent with the region’s long‑term decline in condo development outside Portland’s urban core. Distressed sales ticked up slightly but remain extremely low in absolute terms, signaling normalization rather than systemic stress. Taken together, the aggregate data describe a quieter quarter shaped by composition, structural costs, and the ongoing aging of the condo stock, accented by a sharp showing in the ≥ $1M segment.

Portland Region Scatter Plots

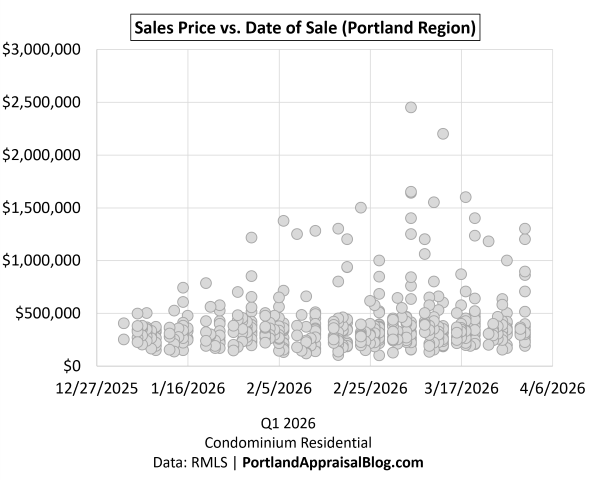

To visualize the sales price distribution of individual condominium units across Q1 2026, the following scatter plots show sales price by date of sale:

The distribution is steady and tightly clustered through most of the quarter, with the bulk of condo sales occurring below the $600,000 mark. Day‑to‑day variation is modest, and the scatter maintains a consistent horizontal band that reflects the core price range of the segment. The only notable deviation appears in mid‑to‑late March, where a handful of high‑priced sales rise sharply above the main cluster—these are the Ritz‑Carlton Portland Residences returning to market activity. Their re‑entry creates a visible vertical lift in the plot, but it does not alter the underlying structure of the broader condo market, which remains stable and price‑dense.

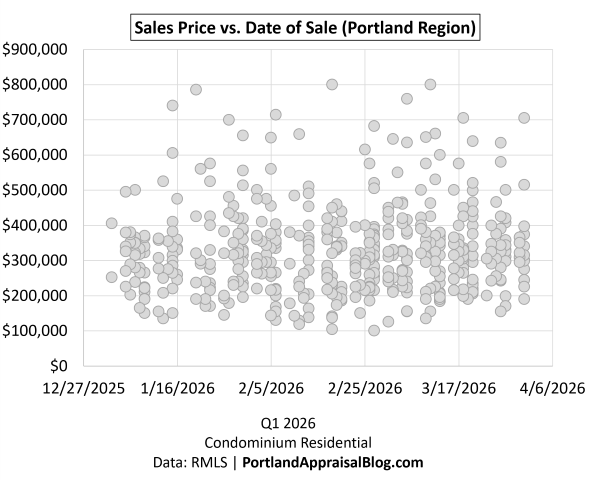

Zooming in on sales priced at $800,000 or less we have:

This zoomed‑in view isolates the portion of the condo market where the vast majority of Q1 2026 activity occurred. Once the upper‑end sales, such as those from the Ritz‑Carlton, are removed, the distribution becomes much easier to read: prices are tightly clustered between roughly $250,000 and $600,000, with only a modest tapering above that range. The day‑to‑day variation is small, and the scatter shows a steady, continuous flow of sales rather than any abrupt shifts or gaps.

What stands out most is how uniform the segment behaves. Even as rates fell and dues rose, the underlying price distribution remained stable, with no visible compression or expansion in the mid‑market band.

Core Market (< $1M)

The table below shows core-market metrics for Q1 2026 compared with Q1 2025:

Category

Core (< $1M) Q1 2025

Core (< $1M) Q1 2026

% Change

Total $ Volume

196.16 Million

$164.37 Million

-16.21%

Average Price

$354,087

$338,206

-4.48%

Median Price

$329,900

$318,500

-3.46%

Avg SP/OLP

94.66%

92.75%

-2.02%

Avg PPSF (TSF)

$332.42

$305.36

-8.14%

Avg HOA Dues

$446.96

$501.79

+12.27%

Median HOA Dues

$419.50

$473.50

+12.87%

Avg Age (Yrs)

27.73

33.21

+19.75%

Avg CDOM

111.03

122.67

+10.49%

Avg Total SF

1,100

1,136

+3.28%

Total # of Sales

554

486

-12.27%

# of New Constr.

142

80

-43.66%

% of $ Volume

96.00%

82.60%

-13.97%

% of Market

99.11%

95.11%

-4.03%

Note: The calculated average HOA dues for the core market is for sales reporting nonzero HOA dues (542 sales for Q1 2025 & 466 sales for Q1 2026). All other metrics use the full dataset for each quarter. Condominium Residential | Q1 2025 & Q1 2026 Data: RMLS | PortlandAppraisalBlog.com

The core condo market—nearly the entire dataset in Q1 2025 and still over 95% of sales in Q1 2026—retreated across almost every major indicator this quarter. Prices softened, with the average down 4.48% and the median down 3.46%. Total dollar volume fell sharply (‑16.21%), driven by both lower prices and fewer sales. New construction dropped by nearly half, reducing the supply of newer, more efficient units and contributing to a noticeable increase in average age, which rose from 27.7 to 33.2 years.

Market tempo also slowed. Average cumulative days on market increased from 111 to 123 days, consistent with a segment where buyers remain selective and inventory is aging. PPSF declined more than headline prices (‑8.14%), reflecting a mix shift toward older, larger, and more moderately priced units.

The dues environment continues to exert pressure. Average HOA dues climbed to just over $500 per month, with median dues rising similarly. These carrying‑cost increases offset part of the buying‑power gains from lower mortgage rates and remain a structural headwind for demand.

Luxury Market (≥ $1M)

The table below shows luxury-market metrics for Q1 2026 compared with Q1 2025:

The luxury condo segment was meaningfully present again in Q1 2026, with 25 sales at or above $1 million. Even excluding the Ritz‑Carlton Portland Residences, the luxury tier still produced twice as many sales as last year, confirming that high‑end condo activity broadened beyond a single building. Total dollar volume reached $34.64 million, and this surge in luxury transactions helped stabilize the quarter overall—core market volume contracted sharply, but the revival of luxury prevented a deeper slide in regional totals.

Luxury pricing this quarter was consistent, with most units trading between roughly $1.2 million and $1.4 million. HOA dues remain a defining feature of the segment: median dues exceeded $2,200 per month, a level that rivals a mortgage payment and underscores the carrying‑cost profile of high‑end condominium ownership. New construction dominated the luxury pool, pulling the average age of units down and contributing to faster absorption, with average cumulative days on market falling to 60 days.

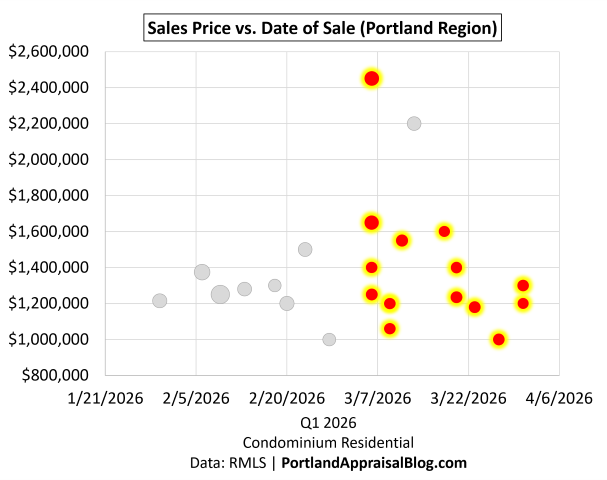

The following scatter plot shows individual sales of $1 million or more across Q1 2026:

Note: The y-axis starts at $800,000 to allow better examination of the dataset. Dots are sized by total square footage.

The scatter plot highlights how sharply the luxury segment shifted once the Ritz‑Carlton Portland Residences resumed closings in March 2026. The red-orange dots with yellow highlight mark those Ritz units, and once they appear, the rest of the luxury market essentially goes quiet—only one non‑Ritz luxury sale closed after the Ritz came online. This pattern reinforces how thin and episodic the ≥ $1M tier is: a single building can dominate the entire segment for weeks at a time.

The remaining non‑Ritz sales form a small band between roughly $1M and $1.4M earlier in the quarter, showing that luxury was active but modest before the Ritz re‑entry. Once the Ritz closings began, the scatter becomes almost entirely Ritz‑driven, visually confirming what the table already suggests—the luxury segment’s revival in Q1 2026 was concentrated, building‑specific, and heavily influenced by the timing of one development.

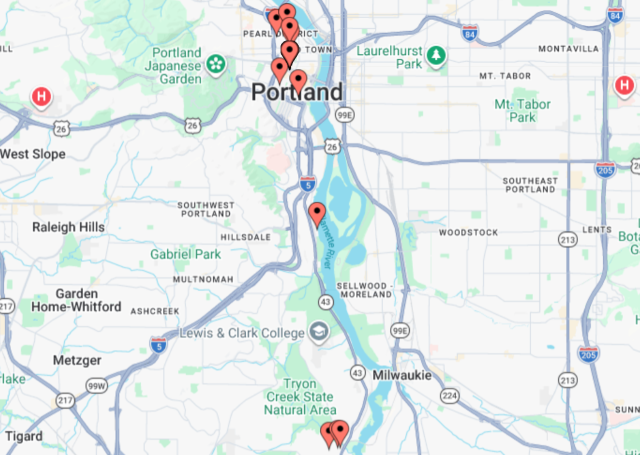

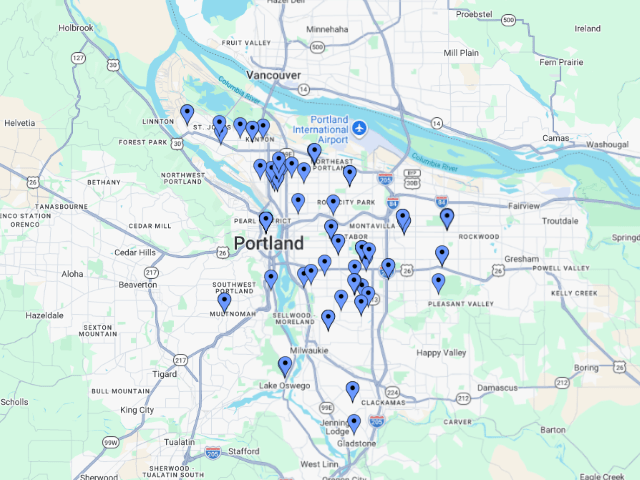

The following map shows where the luxury sales occurred:

And the following table lists the complexes where the sales occurred:

The building‑level breakdown makes clear how concentrated the luxury segment was in Q1 2026. The Ritz‑Carlton Portland Residences accounted for the majority of ≥ $1M sales, with 15 of the 25 transactions this quarter. Outside of the Ritz, luxury activity was modest but meaningfully present across a handful of established buildings in Lake Oswego, the Pearl District, and Portland Downtown. Each of those developments contributed one luxury sale, underscoring how thin and selective the high‑end condo market remains.

This distribution also highlights the geographic reality of luxury condominium living in the Portland Region: it is almost entirely confined to Lake Oswego, the Pearl District, and PortlandDowntown. No other neighborhoods or suburban markets produced a ≥ $1M condo sale this quarter. The table reinforces the same pattern seen in the scatter plot—once the Ritz resumed closings, it dominated the segment.

Bottom-line Summary

Condo activity in the Portland Region softened overall in Q1 2026, with the core market contracting across prices, volume, and sales counts. Core units took longer to sell, PPSF declined, and HOA dues continued their steady climb toward the $500/month mark. These shifts reflect a segment that remains affordable but is moving more slowly, with buyers staying selective and inventory aging.

The luxury tier revived sharply, driven by the return of closings at the Ritz‑Carlton Portland Residences. Even excluding the Ritz, luxury produced twice as many ≥ $1M sales as last year, and the segment’s contribution kept regional dollar volume from sliding further.

Overall, Q1 2026 was a mixed quarter: a cooling core market offset by a concentrated burst of luxury activity, producing a regional picture defined by slower absorption, rising dues, and a luxury segment that re‑entered the market with outsized influence.

Sales Volume

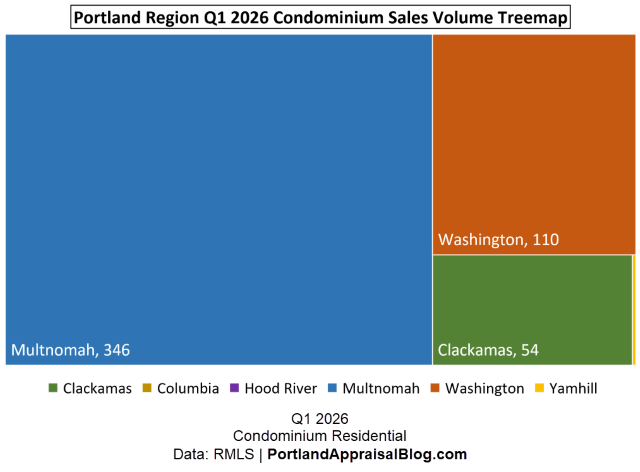

A treemap visualizing the distribution of condominium sales by county in Q1 2026 clearly illustrates the market’s geographic concentration.

The treemap makes the structure of Q1 2026 condo activity immediately clear: this is a Multnomah‑driven market. With 346 sales, Multnomah accounts for over two‑thirds of all regional condo transactions, and its block in the treemap visually dominates everything else. Washington County forms the second anchor at 110 sales (about 22% of the market), creating a clear two‑county core that carries nearly 90% of all condo activity.

Clackamas shows a modest presence at 54 sales, but the remaining counties barely register. Yamhill contributes one sale, and both Columbia and Hood River record zero condo transactions this quarter. The treemap’s proportions reinforce how geographically concentrated condo demand is: the market is effectively a three‑county story, with Multnomah at the center, Washington providing meaningful support, and Clackamas adding a smaller but steady share.

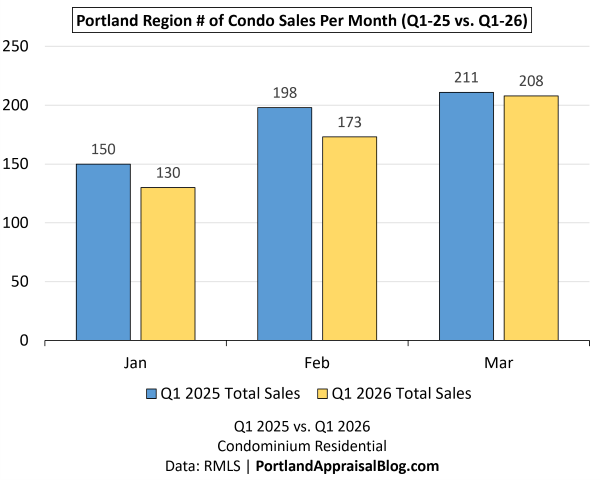

The bar chart below compares monthly sales volume across the three months of Q1 for 2025 and Q1 2026.

The bar chart comparing Q1 2025 and Q1 2026 shows a clear, steady pattern: each month in 2026 trailed its 2025 counterpart, and the gap was consistent enough to pull the quarter down by nearly 9%. January and February posted the largest shortfalls, with January down 20 sales and February down 25, reflecting a softer start to the year. March nearly matched last year—208 vs. 211—but not quite enough to offset the weaker first half of the quarter.

The visual reinforces what the treemap and core‑market tables already suggest: the slowdown wasn’t a single‑month anomaly, but a broad, quarter‑long easing of condo activity. Even with the luxury revival in March, overall sales volume remained lower, and the bar chart makes that month‑by‑month pattern easy to see at a glance.

Sales Price

The bar chart below compares monthly average sales prices across the three months of Q1 for 2025 and Q1 2026.

The bar chart shows a very clear pattern in Q1 2026: prices were soft early in the quarter and then surged in March. January and February tracked almost exactly with the broader slowdown in core activity—both months posted average prices slightly below their 2025 levels, with January down about 9% and February essentially flat.

March is where the visual breaks sharply from the first two months. Average price jumped to $441,378, a 22.8% increase over March 2025. That spike aligns directly with the return of closings at the Ritz‑Carlton Portland Residences, which had been absent from the market for over a year. Even a modest number of Ritz units materially lifts the monthly average, and the bar chart makes that influence unmistakable.

Despite softer pricing in January and February, the strength of March pulls the quarterly average up 6.5% year‑over‑year. The visual reinforces the same theme seen throughout the regional overview: core softened, but luxury prevented a deeper slide, and the timing of Ritz closings shaped the quarter’s pricing profile more than any other single factor.

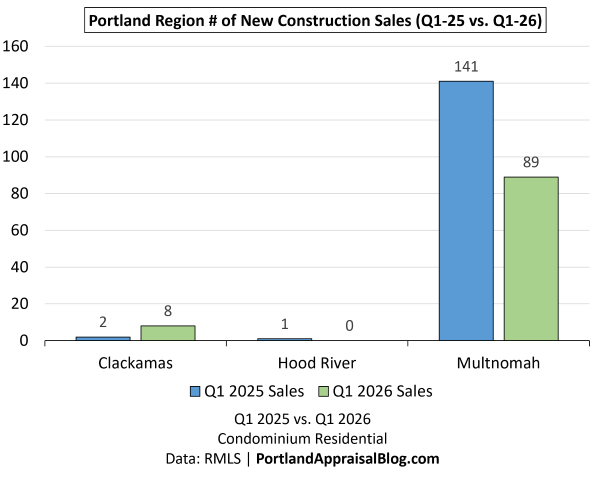

New Construction

The bar graph below shows monthly total condominium sales in Q1 2026, with new construction volume nested within each bar to illustrate the portion of sales that were newly built.

This visual tells a slightly different story once you place it alongside the regional overview tables. New construction was present and steady throughout Q1 2026, and its share of monthly sales rose each month—from 14% in January to 23% in March. Builders clearly remained active, and their contribution was meaningful.

But the bar chart also shows what the overview table already hinted at: new construction wasn’t enough to offset the broader slowdown. Total condo sales fell by 48 units year‑over‑year, and new construction fell by 47 units over the same period. The near‑perfect alignment between those two numbers means the decline in new construction explains almost the entire drop in regional sales volume. Builders helped stabilize the quarter, but their output still landed below last year’s levels.

The visual is best understood as a month‑to‑month strengthening within a year‑over‑year decline. New construction played a stabilizing role, but not a compensating one.

The bar graph below shows the number of new construction closings by county, with side-by-side bars for Q1 2025 and Q1 2026.

The county breakout makes one point unmistakable: condo new construction in the Portland Region is essentially a Multnomah County story. Multnomah delivered 89 new‑construction closings in Q1 2026—down from 141 last year—and because it produces over 90% of all new‑construction condo activity, any slowdown there immediately becomes a regional slowdown. The bar chart shows this visually: Multnomah’s bar contracts sharply, and every other county is so small that they function as rounding errors.

Clackamas is the only county that moved upward, rising from 2 to 8 closings, but even that increase represents just 8% of the regional total. Hood River, Washington, Yamhill, and Columbia collectively contributed one new‑construction sale last year and none this year, reinforcing how geographically concentrated builder activity is.

The takeaway is simple: when Multnomah slows, the region slows, because almost all condo new construction happens there.

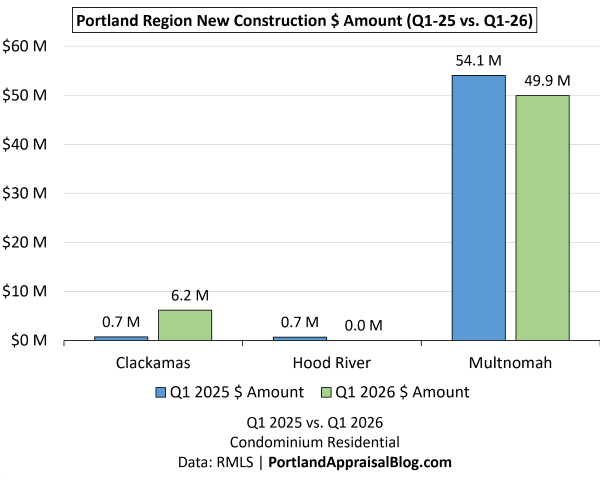

The table below shows new construction sales volume by dollar amount for Q1 2026 compared with Q1 2025.

The following double bar chart provides the above information at a glance.

This table and its companion bar graph sharpen the story we’ve been building: Multnomah still dominates condo new construction, but its slowdown defined the quarter—and the only reason regional dollar volume didn’t fall was a lift from Clackamas.

Multnomah’s new‑construction dollar volume slipped from $54.1M to $49.9M (‑7.66%). That decline aligns with the ‑32.64% drop in new‑construction unit counts shown in the regional overview. Even with the Ritz contributing high‑value closings in March, Multnomah still ended the quarter down year‑over‑year. The Ritz helped hold the line, preventing a steeper decline, but it didn’t fully erase the slowdown.

What actually nudged the regional total slightly upward (+1.06%) was Clackamas County. Its increase from $728K to $6.16M—driven by six additional new‑construction closings—was just enough to offset Multnomah’s decline. The scale is small, but the impact is real: without Clackamas’ bump, regional new‑construction dollar volume would have fallen.

The bar graph reinforces this visually. Multnomah’s bar towers over every other county, and its contraction shapes the regional trend. Clackamas appears as a modest but meaningful counterweight. The remaining counties—Columbia, Hood River, Washington, Yamhill—contribute effectively nothing and function as rounding errors.

The following map shows the distribution of new construction sales:

The vast majority of new construction condos are located east of the Willamette River.

Cumulative Days on Market

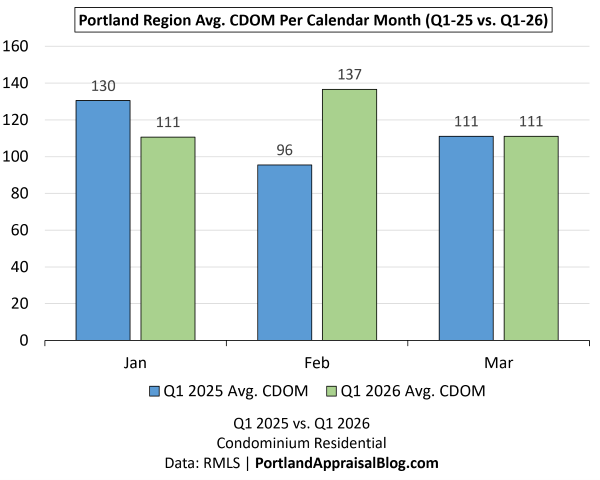

The bar chart below compares average cumulative days on market (CDOM) across the three months of Q1 2025 and Q1 2026.

The monthly CDOM comparison shows that Q1 2026 didn’t move uniformly—it wobbled month‑to‑month before settling into the higher quarterly average we see in the overview. January actually improved year‑over‑year, dropping from 130 to 111 days (‑15%). That early‑quarter efficiency didn’t last. February swung sharply in the opposite direction, rising from 96 to 137 days (+43%), which is the month that ultimately pulls the quarter upward. March then returned to equilibrium, matching last year almost exactly at 111 days.

The bar chart’s pattern—down, up, flat—visually reinforces the broader takeaway: the market wasn’t consistently slower every month, but it was slower overall. With February carrying so much weight, the quarter ends at an average 119.62 days, up 7.99% year‑over‑year. That increase aligns with what we’ve seen throughout the regional overview: buyers were more selective, listings aged longer, and the core market softened enough to push CDOM upward even as luxury activity revived late in the quarter.

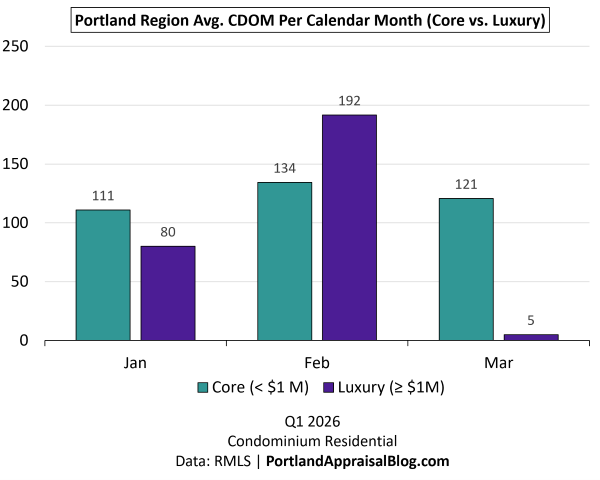

The bar chart below breaks out average CDOM by market segment for the three months of Q1 2026, comparing core (< $1M) and luxury (≥ $1M) properties.

The core‑versus‑luxury comparison shows how differently the two segments behaved in Q1 2026, and how sharply March diverged from the rest of the quarter. Core listings moved slowly throughout, averaging 122.67 days on market for the quarter. January and March were steady at 111 and 121 days, while February pushed higher to 134, which is the month that ultimately drives the core average upward.

Luxury moved in a much more uneven pattern. January’s 80‑day average reflects a normal pace for high‑end units in a softer market. February’s 192‑day average shows the opposite extreme—luxury listings that sat for months before finding buyers. Then March breaks the pattern entirely: the return of Ritz‑Carlton closings produced a cluster of sales with 0 or 1 days on market, pulling the luxury average down to 5 days for the month and dropping the quarterly luxury average to 60.16 days.

Those ultra‑low March readings aren’t random outliers—they’re a signal of pent‑up demand and pre‑positioned buyers waiting for the Ritz‑Carlton Portland Residences to resume closings. When the project finally released units again, the brokerage almost certainly had interested parties already lined up, so the earliest March sales closed immediately upon hitting the market. In other words, the March luxury CDOM isn’t fast because the market structurally changed—it reflects a pipeline of buyers who had been waiting months for the opportunity to transact.

HOA Dues

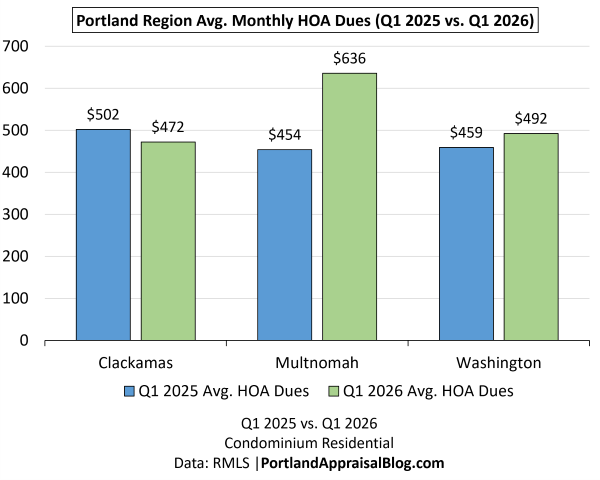

HOA dues are a defining feature of the condominium residential market. The bar chart below compares average monthly HOA dues (for reporting sales) for Q1 2025 and Q1 2026 broken out by county:

The county‑level breakout immediately highlights how uneven HOA dues are across the region—and how sharply Multnomah shifted year‑over‑year. Clackamas and Washington both show modest, stable figures, with Clackamas dipping slightly from $502 to $472 and Washington increasing from $459 to $492. Those changes are small enough that they don’t meaningfully alter the character of either county’s condo market.

Multnomah is the outlier. Average monthly dues jumped from $454 in Q1 2025 to $636 in Q1 2026, a substantial increase driven by the mix of units that sold this quarter. With the return of Ritz‑Carlton closings—and several other high‑amenity buildings contributing sales—Multnomah’s average reflects a heavier concentration of complexes with premium services and correspondingly higher dues. Because Multnomah accounts for the vast majority of regional condo activity, its shift dominates the overall trend.

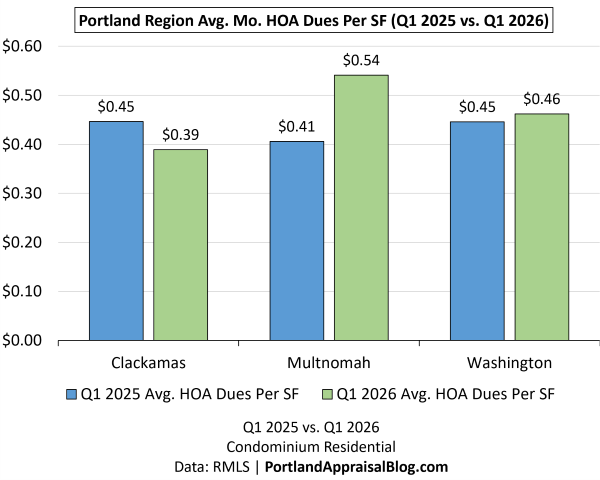

The bar chart below compares average monthly HOA dues per square foot (for reporting sales) for Q1 2025 and Q1 2026:

The dues‑per‑square‑foot view tracks closely with the average monthly dues, reinforcing that HOA costs in the Portland Region scale primarily with unit size rather than with county‑specific fee structures. Clackamas and Washington remain stable year‑over‑year, with Clackamas dipping from $0.45 to $0.39 per square foot and Washington holding essentially flat at $0.45 to $0.46. These small movements mirror the modest changes in their average monthly dues and reflect markets where HOA fees tend to be predictable and tied to straightforward maintenance obligations.

Multnomah again stands out. Dues per square foot rose from $0.41 to $0.54, a jump that aligns with the county’s sharp increase in average monthly dues. The pattern confirms that the higher HOA costs in Q1 2026 weren’t driven by smaller units or unusual fee structures—they were driven by the mix of buildings that sold, particularly high‑amenity complexes like the Ritz‑Carlton Portland Residences and other full‑service properties. When those buildings transact, both total dues and dues per square foot rise in tandem.

The consistency between the two charts underscores a simple point: HOA dues in this region are largely a function of square footage, and when the sales mix shifts toward buildings with premium services, both the monthly dues and the per‑square‑foot metrics move together.

Miscellaneous Statistics & Standout Transactions

Here are some of the most notable outliers and extremes from the 2026 Portland Region condominium residential market—numbers that illustrate the full range of the data and the extremes buyers and appraisers encounter.

Lowest Sales Price: $100,000—This was a 1,104 sq. ft. bank owned condo unit in the golf course community Country Club Estates in Gresham. The unit needed a little work, but represented a low-price entry for bargain buyers. This property also has the lowest price per square foot for the quarter ($90.57). Photos of this property are currently available online.

Highest Sales Price: $2,450,000—Unsurprisingly, the highest sale of the quarter was a unit on the 32nd floor of The Ritz Carlton Residences. This luxury new construction unit also had the highest price per square foot for the quarter ($1,078.89) as well as the highest monthly HOA dues ($3,833). Photos of this property are currently available online.

Smallest Condo: 340 sq. ft.—This condo is located right by I-205 and sold for $118,500—close in price to the lowest sale. HOA dues are also modest, just $192 per month. The low dues may have contributed to the assessment the unit had paid off prior to close, which was nearly $20,000. This illustrates the risk of condo associations with unusually low dues. Photos of this property are currently available online.

Largest Condo: 4,163 sq. ft.—This riverfront condo unit located in the South Portland neighborhood took the crown for the largest condo in Q1 2026. The unit has three bedrooms and three bathrooms and sold for $1.25M. Photos of this property are currently available online.

Highest Monthly HOA Dues Per SF: $1.55/SF—Located in Beaverton, this two-bedroom, two-bath condo is 1,119 sq. ft. and has monthly HOA dues of $1,784. The condo is in an age-restricted community (55+) and includes 14 meals per month. Photos of this property are currently available online.

Longest CDOM: 1,433 days—This 886 sq. ft. condo is located in the Goose Hollow neighborhood and first went on the market in early 2022 and was listed for $335,000. After several listings it finally managed to close for $270,000 in March of 2026. Photos of this property are currently available online.

With the regional aggregate trends, graphs, monthly patterns, and notable outliers covered, the remainder of this update turns to a county-level breakdown. The following sections present year-over-year comparisons for each of the three counties in the Portland Region with appreciable volume—Multnomah, Washington, and Clackamas. Columbia and Hood River counties had no sales and Yamhill County only had one sale for the quarter. Each county snapshot includes key metrics, commentary on local drivers, and any segment-specific observations that help explain broader regional patterns.

Multnomah County Q1 2026 Stats

The table below summarizes key metrics for Multnomah County condominium residential sales in Q1 2026 compared with Q1 2025.

Category

Q1 2025

Q1 2026

Change

Total $ Volume

$145.0 Million

$143.8 Million

-0.86%

Average Price

$382,678

$415,580

+8.60%

Median Price

$337,500

$333,000

-1.33%

Avg SP/OLP

94.34%

92.75%

-1.69%

Avg PPSF (TSF)

$353.33

$347.11

-1.76%

Avg HOA Dues

$454.28

$636.25

+40.06%

Median HOA Dues

$399.08

$493.00

+23.53%

Avg Age (Yrs)

25.59

32.32

+26.32%

Avg CDOM

122.34

124.10

+1.44%

Avg Total SF

1,095

1,180

+7.69%

Total # of Sales

379

346

-8.71%

# of New Constr.

141

89

-36.88%

# of REOs

5

10

+100.00%

# of Short Sales

1

0

-100.00%

Average PABAI

114.14

120.26

+6.12 pts

# Affordable

232

217

-15 units

% Affordable

61.21%

62.72%

+3.39 pts

Note: The calculated average HOA dues is for sales reporting nonzero HOA dues (370 sales for Q1 2025 & 330 sales for Q1 2026). All other metrics use the full dataset for each quarter. Condominium Residential | Q1 2025 & Q1 2026 Data: RMLS | PortlandAppraisalBlog.com

Multnomah’s Q1 2026 condo market shows a mix of stability, compositional change, and luxury‑driven influence. Total dollar volume barely moved year‑over‑year (‑0.86%) despite an 8.7% decline in sales count, a sign that higher‑value transactions—particularly the Ritz‑Carlton closings—helped offset lower throughput. Average price rose 8.6%, even as median price dipped slightly, reflecting a shift toward larger and more expensive units rather than broad price appreciation.

HOA dues saw the most dramatic change. Average dues jumped 40%, and median dues rose 23.5%, confirming that the increase wasn’t limited to the luxury segment. A heavier concentration of older, full‑service, and higher‑amenity buildings contributed to the rise, and the mix shift is reinforced by the increase in average unit age (+26%) and average square footage (+7.7%).

Market tempo remained surprisingly steady. CDOM rose only 1.44%, indicating that Multnomah did not experience the same slowdown seen in the broader regional market. Listings continued to move at nearly the same pace as last year, even with fewer new‑construction units and a more varied mix of properties.

Affordability improved modestly. PABAI rose from 114.14 to 120.26, and the share of affordable units increased from 61.2% to 62.71%, driven primarily by better mortgage rates rather than price declines. The number of affordable units dipped slightly, but affordability as a percentage of sales increased. The reason for the decline in the raw affordable unit count is due to the mix of sales this quarter—especially the number of high-dollar sales from the Ritz Carlton.

Overall, Multnomah’s Q1 2026 performance reflects a market shaped by luxury activity, older and larger units, and higher HOA dues, yet one that maintained a steady tempo and remained broadly affordable under current financing conditions.

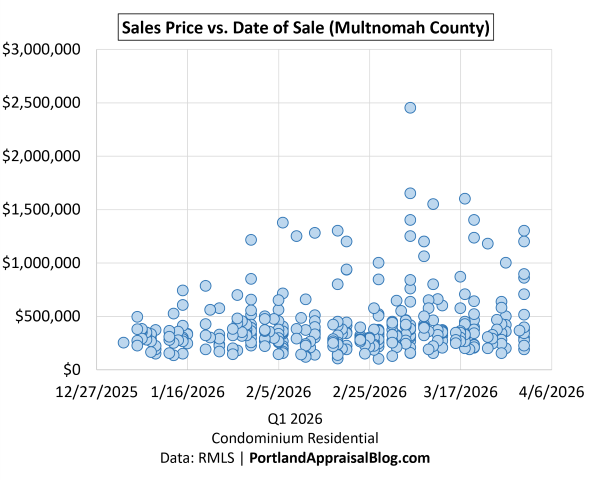

The following is a scatter plot of all Multnomah County sales in Q1 2026:

The full scatter plot presents a clear picture of how Q1 2026 unfolded in Multnomah County. Most sales cluster at $500,000 or below, forming a dense core that reflects the county’s typical condo activity. That concentration is consistent with the pricing distribution shown in the table: even with luxury influence, Multnomah remains a predominantly mid‑market environment.

The plot also shows the moment when Ritz‑Carlton closings came online in March. Those sales appear as the higher‑priced outliers rising above the main cloud. They don’t overwhelm the graph numerically, but they do stand out visually and help explain why dollar volume held steady despite fewer total sales.

No major tilt or directional shift is evident across the quarter. Sales are distributed evenly through time, with no clear slowdown or surge outside the Ritz activity. That stability aligns with Multnomah’s CDOM figures, which changed very little year‑over‑year.

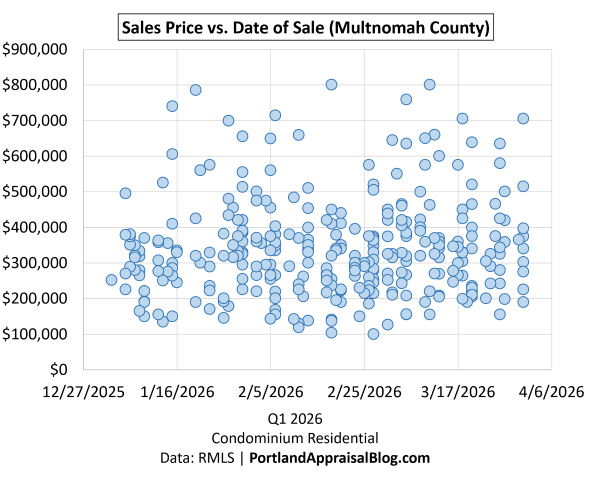

Zooming in on sales priced at $800,000 or less we have:

Clipping the data to sales at $800,000 or less produces a much clearer view of Multnomah’s core condo market, with 316 of the 346 Q1 2026 sales remaining. With the higher‑priced sales removed, the cloud becomes noticeably thinner above $500,000, which is exactly what we would expect given that the county’s average condo price in Q1 2026 was roughly $416,000. Most activity sits well below the $500,000 mark, forming a dense, stable cluster that reflects the dominant mid‑market segment.

The distribution across the quarter remains even. There’s no visible tilt toward early or late months, and no clustering that suggests a sudden shift in buyer behavior or market tempo. The scatter simply shows consistent transactional flow throughout Q1 2026, with the core segment operating at a steady rhythm.

This zoomed‑in view isolates the everyday market dynamics in Multnomah County, separate from the higher‑priced and luxury influence seen in the full‑range scatter. It highlights how the majority of condo sales occur in a relatively narrow price band and how stable that segment remained throughout the quarter.

Washington County Q1 2026 Stats

The table below summarizes key metrics for Washington County condominium residential sales in Q1 2026 compared with Q1 2025.

Category

Q1 2025

Q1 2026

Change

Total $ Volume

$40.14 Million

$31.84 Million

-20.67%

Average Price

$316,074

$289,498

-8.41%

Median Price

$305,000

$295,000

-3.28%

Avg SP/OLP

95.59%

92.96%

-2.75%

Avg PPSF (TSF)

$297.17

$260.77

-12.25%

Avg HOA Dues

$459.30

$492.49

+7.23%

Median HOA Dues

$425.00

$482.00

+13.41%

Avg Age (Yrs)

31.00

32.57

+5.07%

Avg CDOM

77.60

106.03

+36.64%

Avg Total SF

1,092

1,136

+4.02%

Total # of Sales

127

110

-13.39%

# of New Constr.

0

0

—

# of REOs

3

1

-66.67%

# of Short Sales

0

3

—

Average PABAI

116.72

133.74

+16.23 pts

# Affordable

87

98

+11 units

% Affordable

68.50%

89.09%

+20.59 pts

Note: The calculated average HOA dues is for sales reporting nonzero HOA dues (125 sales for Q1 2025 & 107 sales for Q1 2026). All other metrics use the full dataset for each quarter. Condominium Residential | Q1 2025 & Q1 2026 Data: RMLS | PortlandAppraisalBlog.com

Washington County’s condo market saw more pronounced shifts between Q1 2025 and Q1 2026, with several indicators pointing to softer demand conditions. Total dollar volume fell 20.7%, a larger decline than the 13.4% drop in the number of sales, suggesting that the units selling this year were generally lower‑priced. Average price, median price, and price per square foot all moved downward, reflecting a mix that leaned toward more modest units. The broader economic backdrop—particularly the Intel layoffs—likely contributed to this tilt, reducing upward pressure on pricing and dampening buyer activity across the westside.

Marketing times lengthened substantially. Average CDOM rose from 77.6 days to 106.0 days, adding nearly a full month to the typical listing period. This increase mirrors the regional slowdown but was likely amplified locally by employment uncertainty. Sellers also had to concede more from their original list prices, with SP/OLP falling from 95.6% to 93.0%, a shift consistent with a market where buyers exercised more caution and negotiation leverage.

Affordability, however, improved sharply. PABAI increased more than twenty points, and the share of affordable units rose from 68.5% to 89.1%. Even with fewer total sales, the number of affordable units increased from 87 to 98. This improvement is driven primarily by better mortgage rates, though the decline in pricing helped reinforce the trend. Washington County’s condo segment remains one of the most affordable in the region, and Q1 2026 underscored that position.

Washington County also had no new‑construction condo sales in either quarter, and this absence is part of a longer‑running trend. The entire year of 2024 produced just 12 new condo units and all of 2025 produced only 5, leaving the county with virtually no active condo development pipeline. This lack of new supply does not directly explain the jump in CDOM—that increase is clearly tied to regional softening and the Intel layoffs—but it does shape the composition of what sells. With no new units entering the mix, the segment leans heavily on older, modest buildings. Average age naturally drifts upward, PPSF becomes more sensitive to demand shifts, and buyers face a narrower range of choices than in counties with active condo development.

The contrast with Washington County’s attached‑home market is notable. While condo development has been nearly inactive, the attached segment has been exceptionally strong. In 2025, 53.65% of all attached‑home sales in the Portland Region occurred in Washington County, and builders delivered 393 new attached units, compared to 169 in Multnomah. Builders appear to be responding to buyer preferences, and those preferences currently favor attached homes over condos. This divergence helps explain why Washington’s condo segment feels constrained while its attached segment remains active and well‑supplied. For more detail on this trend, see the 2025 Attached Homes Annual Review.

Taken together, these patterns show a condo market adjusting to economic headwinds while also operating within a limited development environment. Softer demand, longer marketing times, and lower pricing define the quarter, but the structural absence of new condo supply adds an additional layer that shapes the segment’s age profile, affordability, and overall behavior.

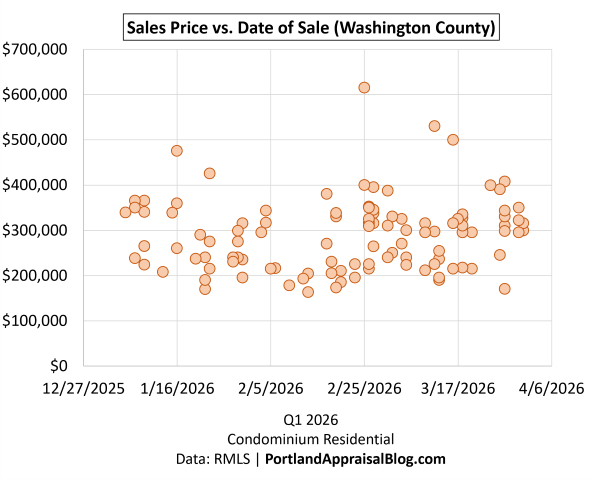

The following is a scatter plot of all Washington County sales in Q1 2026:

The full scatter plot for Washington County shows a market that is active but clearly softer than Multnomah, with most sales clustering below $400,000 and only a small number of transactions pushing toward the upper end of the county’s condo price spectrum. The cloud is dense in the mid‑market range, reflecting the county’s overall pricing profile and the declines seen in average price, median price, and PPSF in the quarterly table.

There is no strong tilt or directional shift across the quarter. Sales appear consistently from the beginning of January through the end of March, with no obvious surge or slowdown tied to specific weeks. This even distribution aligns with the broader regional pattern of slower but steady buyer activity. The scatter does not show abrupt gaps or clustering that would suggest a sudden change in demand; instead, it reflects a market that continued to move, albeit at a more measured pace.

The upper end of the scatter is relatively thin, which is expected given Washington County’s average condo price of $289,498 in Q1 2026 and the absence of new luxury or high‑amenity buildings. Without new‑construction condos entering the mix, the segment leans heavily on older, modest units—a structural condition that shapes the entire distribution of prices visible in the plot. The lack of new supply doesn’t create volatility; it simply limits the range of available product types, which is exactly what the scatter shows.

Overall, the full‑range scatter illustrates a condo market defined by mid‑market activity, steady transactional flow, and a narrower price band than counties with active condo development. It complements the table by visually reinforcing the softer pricing environment and the stable but slower rhythm of Q1 2026.

Clackamas County Q1 2026 Stats

The table below summarizes key metrics for Clackamas County condominium residential sales in Q1 2026 compared with Q1 2025.

Category

Q1 2025

Q1 2026

Change

Total $ Volume

$16.62 Million

$23.16 Million

+39.36%

Average Price

$353,546

$428,844

+21.30%

Median Price

$320,000

$352,500

+10.16%

Avg SP/OLP

94.94%

93.84%

-1.16%

Avg PPSF (TSF)

$300.25

$321.18

+6.97%

Avg HOA Dues

$502.03

$472.11

-5.96%

Median HOA Dues

$486.00

$504.00

+3.70%

Avg Age (Yrs)

35.19

29.09

-17.33%

Avg CDOM

95.30

116.35

+22.09%

Avg Total SF

1,247

1,272

+1.99%

Total # of Sales

47

54

+14.89%

# of New Constr.

2

8

+300.00%

# of REOs

0

2

—

# of Short Sales

0

0

0.00%

Average PABAI

106.19

115.90

+9.71 pts

# Affordable

28

39

+4 units

% Affordable

59.57%

72.22%

+12.65 pts

Note: The calculated average HOA dues is for sales reporting nonzero HOA dues (46 sales for Q1 2025 & 53 sales for Q1 2026). All other metrics use the full dataset for each quarter. Condominium Residential | Q1 2025 & Q1 2026 Data: RMLS | PortlandAppraisalBlog.com

Clackamas County’s condo market stands out immediately because it is the only county to post an increase in total dollar volume. The jump of 39.36% is driven almost entirely by higher throughput: sales rose from 47 to 54, a meaningful gain given how small this segment is. With such low volume, even modest increases in activity can move county‑level totals quite a bit.

Pricing moved upward across the board. Average price rose 21.3%, median price increased 10.2%, and PPSF climbed nearly 7%. These increases are partly compositional. Clackamas had 8 new‑construction condo sales in Q1 2026 compared to just 2 the year before. In a small market, even a handful of new units can lift averages, especially when the existing stock is older and more modest. The decline in average age from 35.2 years to 29.1 years reflects this shift directly. Clackamas also saw several sales at or above $1.5M; the highest sale in Q1 2025 was only $710,000.

The HOA pattern in Clackamas is different from the other counties. Median dues are higher than average dues, which indicates that a number of units have very low HOA dues that pull the average down. This is consistent with the county’s inventory: Clackamas has more small, older complexes with minimal amenities, and those buildings often carry lower dues. At the same time, the median rising from $486 to $504 shows that the typical building still saw modest upward pressure.

Marketing times lengthened, with CDOM rising from 95.3 to 116.4 days, a trend consistent with the regional slowdown. Sellers conceded slightly more from their original list prices, though the change in SP/OLP was modest. Affordability improved as well, with PABAI rising nearly ten points and the share of affordable units increasing from 59.6% to 72.2%.

Overall, Clackamas shows a mix of stronger throughput, higher pricing, and modest compositional shifts driven by a small but meaningful increase in new‑construction units. It remains a small condo market, but Q1 2026 was a comparatively active quarter.

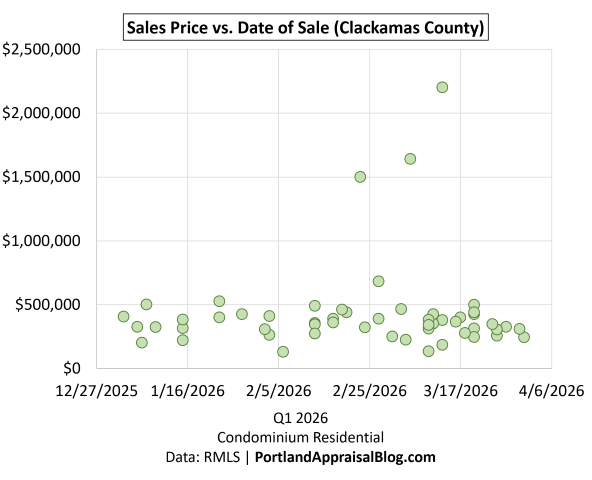

The following is a scatter plot of all Clackamas County sales in Q1 2026:

The full scatter plot for Clackamas County shows a market with a wide price spread, reflecting both the county’s modest core inventory and the presence of a few high‑end units that push well above the typical range. Most sales cluster between roughly $200,000 and $500,000, forming a dense mid‑market cloud that aligns with the county’s median price of $352,500. This is the heart of Clackamas’s condo activity, and the scatter makes clear that the majority of transactions occur in this relatively narrow band.

Above that core, the plot shows a handful of higher‑priced outliers—units selling above $1 million, and even one approaching $2.2 million. These sales, located in Lake Oswego, are not representative of the broader market, but they do help explain why average price rose 21.3% year‑over‑year. In a small county with only 54 sales, even a few high‑end closings can noticeably lift averages. This is also where the increase in new‑construction units matters: Clackamas recorded 8 new‑construction condo sales in Q1 2026, compared to just 2 the year before. New units tend to be larger, newer, and more expensive, and their presence contributes to the upward movement in both average price and PPSF.

The scatter shows steady activity across the quarter, with no strong tilt toward early or late months. Sales appear consistently, reflecting a market that moved at a measured but continuous pace. The increase in CDOM—rising from 95.3 to 116.4 days—is not visible in the scatter itself, but the even distribution of points suggests that listings continued to find buyers despite the slower regional tempo.

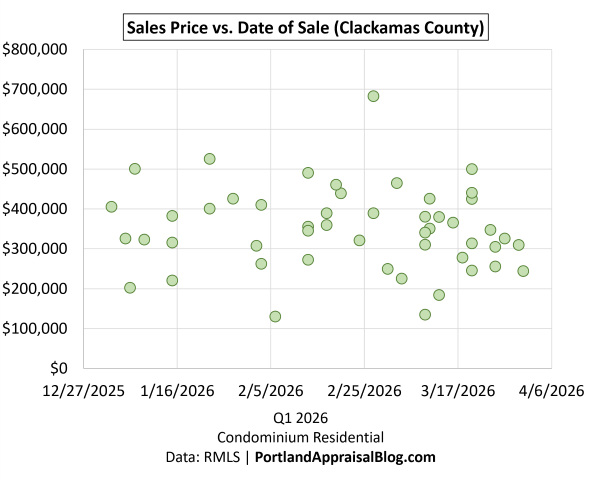

Zooming in on sales priced at $700,000 or less we have:

Zooming in on sales $700,000 and below helps isolate the core market by removing the high‑end outliers. Once clipped, the scatter becomes much more representative of typical Clackamas activity. The cloud is dense below $500,000, and the distribution above that level is almost nonexistent—exactly what we would expect given the county’s pricing profile and the modest nature of most of its condo inventory.

This zoomed‑in view reinforces the compositional story in the table. Clackamas remains a small condo market dominated by older, mid‑market units, but the addition of a few new‑construction sales in Q1 2026 nudged pricing upward and lowered the average age of the segment. The scatter shows that the core market remained active and stable, while the high‑end units—though few—added noticeable lift to the county’s averages.

Closing Thoughts

Across the Portland Region, Q1 2026 showed a condo market adjusting to softer demand, longer marketing times, and a more cautious buyer pool. Washington County reflected this most clearly, with lower pricing, slower tempo, and a sharp rise in affordability shaped by both economic conditions and a lack of new‑construction supply. Multnomah County remained the region’s anchor, with stable mid‑market activity and a handful of luxury closings that lifted dollar volume without altering the underlying rhythm of the quarter. Clackamas County stood apart, posting higher throughput and higher pricing, helped by a small but meaningful increase in new‑construction units and a few high‑end sales that expanded the county’s price range.

Even with these differences, the counties shared several common themes. Marketing times increased everywhere, sellers conceded more from their original list prices, and the mid‑market segments carried the bulk of transactional activity. Improved mortgage rates pushed affordability higher across the region, especially in counties with modest inventory profiles.