Q3 2025 Portland Region condo data reveals only 5% of sales are realistically affordable for senior households on median fixed incomes, despite condos being an ideal downsizing option.

Entrance detail of the Empress Condominiums in Northwest Portland—a 1927 building exemplifying the historic character of many pre-1970 condominium conversions in the region. Photo: Abdur, Abdul-Malik, Portland Appraisal Blog (CC BY-SA 4.0)

Condominiums have long been viewed as an ideal downsizing option for seniors seeking lower-maintenance ownership, potential aging-in-place features, and proximity to urban amenities. National narratives—including recent discussions of a “silver tsunami” of baby boomer downsizers—often highlight condos as a key solution for older households looking to “rightsize.”

Yet Q3 2025 condominium closed-sales data from the Portland Region reveals a starkly different reality for seniors reliant on typical fixed incomes.

Using the Portland Appraisal Blog Affordability Index (PABAI)—a distribution-averaged metric calculated individually for each transaction based on actual sale price, reported HOA dues, and property taxes, combined with current mortgage rates, insurance estimates, and a conservative 20% down payment with 28% qualifying ratio—only 5.4% of the 651 condominium sales (35 units) generated a monthly carrying cost affordable on a median senior household income of approximately $68,284.

This analysis focuses exclusively on single-family residential class condominiums across the Portland Region—the six-county area that is the focus of this blog.

The Equity Divide in the Condo Market

Financing terms, as reported by listing agents in RMLS, tell much of the story (see table below). Cash purchasers accounted for 33.8% of transactions (220 sales) and paid the highest average price ($407,000) while accepting the highest average monthly HOA dues ($669). Conventional financing dominated another 54.1%, reflecting buyers with strong credit and often substantial down payments.

Financing Type

% of Sales

# Sales

Avg Close Price

Avg Monthly HOA

Cash

33.8%

220

$407,000

$669

Conv.

54.1%

352

$365,000

$460

FHA

8.0%

52

$283,000

$403

VA

2.6%

17

$340,000

$356

Q3 2025 Portland Region condominium financing terms as reported by listing agents in RMLS, showing average close price and monthly HOA dues by type. (Top 4 financing types only.) Data: RMLS | Portland Appraisal Blog

In contrast, FHA financing—typically associated with lower down payments and more income-sensitive qualification—represented only 8.0% of sales, with an average close price of $283,000 and more moderate HOA dues ($403 monthly).

This segmentation underscores a clear divide: equity-rich seniors downsizing from detached homes can readily access the market, often paying cash or leveraging large down payments to absorb elevated carrying costs. Seniors without significant prior home equity, reliant primarily on Social Security, pensions, or modest retirement savings, face severe barriers.

Price Distribution and the Narrow Affordable Tier

Q3 2025 condominium sales clustered heavily in the $200,000–$400,000 range, but the truly affordable segment for median senior incomes proved far smaller.

Price Band

# Sales

% of Total

Avg Close Price

Avg Year Built

Avg Monthly HOA

Under $200k

53

8%

$164,000

1968

$461

$200–299k

216

33%

$255,000

1984

$500

$300–399k

203

31%

$346,000

1997

$431

$400–499k

89

14%

$443,000

1999

$492

$500k+

90

14%

$779,000

1997

$889

Q3 2025 Portland Region condominium sales distribution by price band, with average year built and monthly HOA dues. Data: RMLS | Portland Appraisal Blog

The 35 units affordable under conservative PABAI assumptions were overwhelmingly concentrated in the under-$200,000 and lower $200,000–$299,000 bands—older, smaller properties that appear accessible on purchase price alone.

Age, Obsolescence, and Elevated Carrying Costs

Older condominiums—many conversions of pre-1970 apartment buildings — present particular valuation challenges. The table below excludes new construction deliveries, as agent-reported HOA dues for newly completed projects are often provisional or incomplete.

Year Built Bracket

# Sales

Avg Close Price

Avg Sq Ft

Avg Monthly HOA

Avg HOA per Sq Ft

Pre-1970

95

$304,000

977

$572

$0.67

1970–1989

194

$309,000

1,146

$575

$0.52

1990–1999

43

$388,000

1,117

$555

$0.52

2000–2009

199

$443,000

1,265

$661

$0.54

2010+

51

$474,000

1,394

$284

$0.26

Average Q3 2025 condominium characteristics by year-built bracket (new construction excluded due to provisional HOA reporting). Pre-2010 stock shows markedly higher HOA burden per square foot. Data: RMLS | Portland Appraisal Blog

Pre-1970 stock carries the highest average HOA dues per square foot ($0.67), reflecting ongoing capital needs for aging systems, reserves, and occasional special assessments. This elevated recurring cost creates meaningful external obsolescence for income-constrained buyers, even when entry prices appear lower.

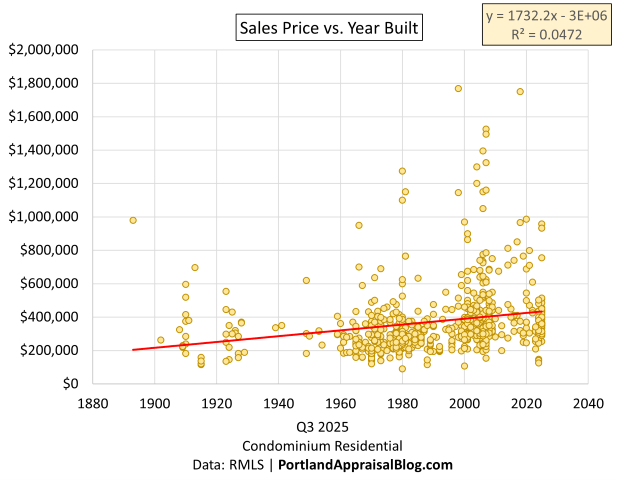

A scatterplot of sales price against year built further illustrates this dynamic. While newer construction generally commands higher prices, the weak correlation (R² = 0.047) confirms that factors beyond age—location, views, amenities, and building quality—dominate value. Older units cluster at lower prices, yet as shown above, they often carry disproportionately high recurring costs.

Sales Price vs. Year Built — Q3 2025 Portland Region condominiums (651 sales). The weak correlation (R² = 0.047) illustrates that location, amenities, and building quality drive value far more than age alone.

County-Level Consistency

The challenge persists across the Portland Region:

County

# Sales

% Affordable for Seniors

Multnomah

426

6.3%

Washington

144

3.5%

Clackamas

69

4.4%

Portland Region Total

651

5.4%

Share of Q3 2025 condominium sales affordable under conservative PABAI assumptions, by county. Data: RMLS | Portland Appraisal Blog

No county offers a meaningful suburban relief valve for fixed-income seniors. (Over 98% of Q3 2025 condominium sales occurred in the three counties in the table above.)

Even FHA Terms Do Not Meaningfully Expand Access

Conventional wisdom might suggest FHA financing—with 3.5% down payments and more lenient debt-to-income ratios—would open the market wider for seniors with limited savings. Yet when mortgage insurance premium (0.55% annual) and the resulting larger loan are included, the share of affordable units actually declines to 3.8%.

Higher principal and interest, combined with permanent MIP, outweigh the benefits of lower upfront equity for households with constrained monthly cash flow.

Appraiser Perspective: Comparable Selection and Reconciliation Challenges

When appraising condominiums, comparable selection must account for competitive market segments defined by building age, location, complex-specific amenities, and HOA structure. Units in markedly different projects—for example, a 1960s conversion versus a 2000s high-amenity tower—are rarely direct substitutes.

Differences in functional utility, functional obsolescence, and market-perceived recurring costs often require careful adjustments or exclusion from the primary grid.

Conclusion

While condominiums remain a logical theoretical choice for seniors seeking reduced maintenance and urban access, Q3 2025 condo data demonstrates that ownership is realistically attainable only for those with substantial prior home equity. For senior households reliant primarily on fixed incomes near the median, monthly carrying costs—particularly in older stock with higher HOA burdens—render the vast majority of the market out of reach without additional equity or savings.

Many will continue to rely on rental options or supportive housing models, such as the recently opened Julia West House in Portland, which provides dedicated affordable senior housing.

For many seniors, condominiums represent an appealing downsizing opportunity—yet Q3 2025 data shows monthly carrying costs limit access for those without substantial equity. Via Canva Pro

Sources & Further Reading

The Portland Appraisal Blog Affordability Index: PABAI

National Association of REALTORS discussion of senior downsizing trends: Original Article

Recent coverage of Julia West House supportive senior housing opening: Portland Appraisal Blog

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

The final full week of 2025 sharpened focus on the deep affordability barriers defining the Portland Region’s housing market, while also spotlighting regulatory and tax issues with real consequences for homeowners—especially veterans. A closer look at the 2024 MAV Reset Clarification revealed how the loss of a disabled veteran exemption can trigger a permanent upward reset in maximum assessed value, locking in higher property taxes even if the exemption is later restored. Meanwhile, groundbreaking on a major apartment project pushed forward despite tight financing, and fresh Q3 data underscored why most first-time buyers must now wait until age 40 to enter the detached single-family market.

That Q3 analysis, powered by the new Portland Appraisal Blog Affordability Index(PABAI), showed that fewer than 10% of recent detached sales were realistically within reach for households aged 25–44 once full PITI costs are considered. A separate deep dive into today’s typical $600,000 home purchase laid out the household income actually required—far above median levels for younger buyers. Together, these pieces highlight a region where entry-level detached ownership remains elusive without substantial down-payment help, outlier earnings, or delayed timelines.

At the same time, multifamily development continues as one of the brighter spots, with projects like the Barbur Apartments aiming to deliver more rental options amid high construction costs and steep financing hurdles. These efforts reflect broader attempts to ease the overall supply crunch, even as single-family affordability stays structurally constrained.

Sunday, December 21: Barbur Apartments Groundbreaking Highlights Plottage Value

The Barbur Apartments site sits at the prominent intersection of SW Barbur Blvd and SW Capitol Hill Rd. Photo: Portland Appraisal Blog

Groundbreaking commenced in mid-December 2025 on the Barbur Apartments, a 150-unit affordable family housing project located at the corner of SW Barbur Blvd and SW Capitol Hill Rd in Portland’s Hillsdale/Multnomah Village area. Developed by Innovative Housing, Inc., the complex will feature one three-story building and two four-story buildings, delivering 149 income-restricted units (one reserved for an onsite manager) with many larger two- to four-bedroom layouts targeted at immigrant and refugee families. Amenities include a courtyard and community spaces, with completion expected in Fall 2027.

The project carries an estimated total development cost of approximately $79.4 million, supported by about $27.3 million from the Portland Housing Bureau alongside regional Metro Housing Bond funds, federal sources, and Portland Clean Energy Community Benefits Fund contributions for energy efficiency. It emphasizes transit access along the Barbur corridor, with approved plans providing roughly 45 on-site parking spaces—a ratio of about 0.3 spaces per unit reflecting the transit-oriented design.

From an appraisal perspective, the redevelopment exemplifies plottage, the incremental value gained by assembling contiguous parcels into a larger, more developable site. Four tax lots totaling around 2.19 acres were purchased together in February 2025 for just under $6 million. Individually constrained by size, zoning, and existing improvements, the parcels supported only lower-intensity uses.

One parcel formerly held a 1927-built single-family home of approximately 2,336 square feet that was never listed on the open market and quickly demolished, demonstrating clear functional obsolescence as the corridor evolves. An adjacent former commercial strip—Barbur Blvd Rentals—remains standing but fenced within the construction zone. Together, these lots enable a density and scale unattainable separately, illustrating classic plottage and a shift to higher-density residential as the highest and best use.

Directly across Barbur Blvd sits a large Safeway complex with extensive covered and surface parking, a significant amenity for future residents. However, with the project’s limited on-site parking space and family-oriented unit mix, residents and guests may increasingly rely on this private lot for overflow. A mid-morning site visit revealed a nearly full garage, suggesting potential increased daytime use once occupied—a dynamic worth monitoring.

Local market data from 2024–2025 closed sales in Hillsdale and Multnomah Village underscores limited affordability. Detached homes led with 351 sales averaging $750,000 and 50 days on market. Condominiums, the most accessible ownership segment by volume, averaged $445,000 across 78 sales with longer 68-day absorption. Attached homes, a small segment of just 13 transactions, averaged $581,000—likely due to more recent construction (average year built 2010) and associated premiums. Overall averages reached $691,000, highlighting ownership barriers and the critical role of regulated rentals like Barbur Apartments for lower-income and larger households.

This assemblage aligns with broader city efforts to expand housing through density and public investment, including recent regulatory reforms aimed at reviving Portland development.

Tuesday, December 23: The Measure 50 Compression Trap and the 2024 MAV Reset Clarification

A classic pre-1940 home in the Portland Region – the type of property often benefiting from deep Measure 50 tax compression. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

In Oregon’s property tax system, established by Measure 50 in 1997, a common pitfall has emerged for buyers of older homes: unexpectedly high tax bills following the loss of certain partial exemptions. This occurs when a veteran or active-duty partial exemption ends—often upon sale or the owner’s passing without a qualifying successor—triggering a reset of the property’s Maximum Assessed Value (MAV) closer to current market reality. Previously, counties preserved the low MAV after removing the exemption, but updated 2024 guidance from the Oregon Department of Revenue now enforces a constitutional recalculation, potentially adding $2,000–$6,000 annually to taxes for pre-1997 properties with deep compression.

Measure 50 created two key values: Real Market Value (RMV), reflecting current market conditions, and MAV, initially set below 1995–1997 RMV and capped at 3% annual growth thereafter (with exceptions). The Assessed Value (AV) is the lesser of the two, leading to substantial compression in high-appreciation areas like Portland, where older homes often have MAV far below RMV. When a partial exemption disqualifies, the new guidance applies the Changed Property Ratio (CPR)—around 0.54 for residential properties in Portland Region counties for 2025–2026—to reset MAV to current RMV multiplied by CPR, aligning taxes more closely with newer homes.

Q3 2025 sales data for detached single-family residences in the Portland Region highlights this compression. Pre-1940 homes averaged $671,295 in sale price but only $6,396 in annual taxes, while 1940–1959 properties averaged $607,466 with $5,766 in taxes. In contrast, 2000–2019 homes averaged $761,061 with $7,685 in taxes. Effective tax burdens remained consistent at ~$9–$10 per $1,000 of sale price across eras, showing the market prices properties assuming similar overall loads. However, absolute taxes rise with newer construction due to less historical compression, and pre-1940 homes often command premiums despite lower taxes—creating vulnerability when resets occur.

The veteran (ORS 307.250) and active-duty (ORS 307.286) exemptions provide modest reductions—up to $31,565 or $108,366 for 2025–2026, worth $400–$700 annually in savings—but their disqualification now triggers the full MAV reset. With over 114,000 veterans in the metro area, affected transactions can see increases of $1,500–$4,000 yearly in typical cases, or $4,000+ in deeper-compression scenarios. This translates to $125–$333 monthly, comparable to a car payment, potentially straining affordability and prompting renegotiations.

For market participants, the reset introduces friction: buyers may demand concessions, sellers (including veterans or surviving spouses) face lower net proceeds, and properties can linger on the market if low current taxes mask future costs. Outliers with unusually low taxes may reflect active exemptions or compression soon to erode.

Appraisers should verify exemption status via county records, estimate post-reset taxes, and comment on marketability when material. Low-tax comparables warrant scrutiny—effective rates of 0.6–0.8% may signal compression, better aligned post-reset at 1.1–1.3%. Providing dual tax scenarios aids informed valuation. As resets appear in more closed sales from 2026 onward, this factor will increasingly explain pricing anomalies in Oregon’s older housing stock.

Thursday, December 25: Portland’s Starter Home Market (Q3 2025) — What $469k Really Buys

A classic early-20th-century bungalow in the Portland area—the type of modest, well-loved home that dominates today’s starter-tier inventory. Via Canva Pro

In another Appraisal Deep Dive, we examine Portland’s starter-home market using Q3 2025 RMLS data for detached single-family residences in the 5th–35th percentile by price—the same convention Redfin used in its October report highlighting Portland’s strong starter activity.

Redfin’s reported median of approximately $420,000 includes all property types, but focusing solely on detached homes—a popular choice across the metro, including for urban buyers seeking yard space and privacy—yields an average close price of $469,000. Local buyers want to know how much home this budget actually buys, and the data reveals a market overwhelmingly dominated by mid-century inventory, with stark county differences and only a modest presence of brand-new construction.

Across the core counties, Multnomah drives nearly half the volume with the oldest average build year (1951), while Washington posts the highest prices and hosts the most new homes. Outer counties like Columbia and Yamhill offer newer builds on larger parcels but far fewer sales. Square footage emerges as one of the stronger (though still modest) drivers of price, with most sales clustering between 1,200 and 2,000 square feet. Lot size patterns show a clear historical shift: post-war boom homes (1940s–1950s) typically enjoy generous parcels, while newer construction relies on much smaller lots—often the result of infill and divisions.

New homes account for just 4.2% of starter-tier sales (versus 9.1% market-wide), yet their presence remains noteworthy in a high-cost building environment. They sell for only about 3% more than existing homes despite brand-new condition but deliver less interior space and roughly half the land. For buyers, this creates a clear trade-off: modern efficiency and low maintenance on a very small lot (often minimal usable yard, especially in Multnomah and Washington) versus an older mid-century home with significantly more outdoor space, albeit with potential challenges in systems and layout—a choice particularly relevant for growing families prioritizing play areas or privacy.

Appraisal insights reveal that chronological age correlates weakly with both sales price and price per square foot. Effective age, condition, and site utility drive value far more, with lot size advantages in older homes often offsetting credits for new condition. When appraising the limited new-construction sales (down ~25% YoY overall, 48% in Multnomah), appraisers typically rely on other recent builds and adjust heavily for quality of upgrades and site characteristics.

Overall, Portland’s starter segment continues heavy reliance on mid-century stock on larger lots—a pattern unlikely to change dramatically in 2026 without major supply shifts, though the City of Portland is attempting to incentivize new projects via SDC waivers. The modest new-construction foothold demonstrates builder adaptation, but at the clear cost of site size and outdoor space.

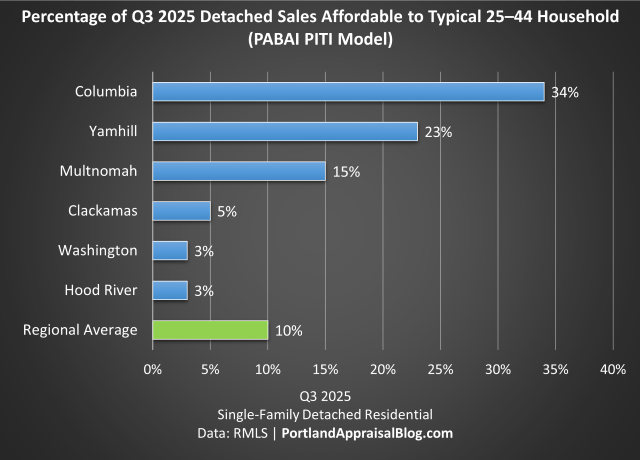

Saturday, December 27: Portland’s First-Time Buyers Have No Choice But to Wait Until 40 — Q3 2025 Data Explains Why

Classic Craftsman bungalows homes in a Portland neighborhood. While older detached stock like this offered relatively better access for younger buyers in Q3 2025 (15% affordable in Multnomah County under realistic PITI assumptions), many close-in properties commanded premium prices—this example on the right sold for $1.1 million. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Recent Q3 2025 data reveals that only about 10% of detached single-family homes in the Portland Region were affordable to typical households aged 25–44 under realistic payment assumptions, highlighting why first-time buyers are increasingly delayed until reaching age 40. Nationally, the median age of first-time buyers has hit a record 40, with their share of purchases at a historic low, driven by persistent affordability barriers.

Traditional measures, such as the National Association of Realtors’ Housing Affordability Index—which considers only principal and interest with a 25% qualifying ratio—suggest that roughly 28% of Q3 2025 detached sales in the six-county Portland Region were affordable to a household at the area median income of $124,100. However, incorporating actual property taxes and a conservative homeowners insurance estimate into the full PITI payment drops this to 20% for the same benchmark.

This analysis introduces the new Portland Appraisal Blog Affordability Index (PABAI)—a more accurate, PITI-based metric tailored to the Portland Region’s market. The PABAI expresses affordability as an index value (100 indicating exact qualification for the typical home) and derives the percentage of sales affordable to reference households. For the regional benchmark using HUD’s $124,100 area median income, the PABAI stood at approximately 78. For younger 25–44 households with a median income of about $110,000, it fell to 69—meaning only 9.8% of Q3 detached sales (460 out of 4,682) were within reach. The typical $600,000 detached home required roughly $159,000 in household income—45% above this cohort’s median.

County-level variation underscores geographic disparities for 25–44 buyers. Outer areas like Columbia County (34% affordable) and Yamhill County (23%) provided the most options, though often at the cost of longer commutes to urban centers. Multnomah County outperformed at 15%, benefiting from denser, older stock, while suburban Washington (3%) and Clackamas (5%) counties lagged due to larger lots and higher-priced inventory. Hood River registered just 3%.

In Q3 2025, younger buyers seeking detached homes typically needed substantial family assistance, extreme lifestyle sacrifices for larger down payments, or outlier incomes well above cohort medians to gain entry. Without these, most were effectively priced out until accumulating higher earnings in their late 30s or early 40s—or forced into alternatives like condominiums.

The PABAI models affordability with a 20% down payment, 28% front-end ratio, actual rates, listing taxes, and a 0.40% insurance rate, offering granular insights beyond national indices that overlook taxes and insurance. This realistic approach confirms the structural challenges pushing first-time buyer ages upward in the Portland Region.

Taken together, this week’s coverage paints a picture of a Portland metro market where structural barriers—high prices, elevated property taxes, and insurance costs—continue to sideline younger households from detached homeownership. The introduction of the Portland Appraisal Blog Affordability Index offers a clearer, more localized tool for understanding these gaps, showing that realistic PITI-based qualifying leaves fewer than 10% of recent sales within reach for 25–44-year-olds.

Regulatory and measurement topics add another layer of complexity for industry professionals. Clarifications around the 2024 MAV Reset and the accompanying tax implications serve as reminders that appraisal assignments increasingly demand careful awareness of tax policy and its effects on value and marketability.

The common thread remains one of constrained supply at affordable price points, driving both multifamily investment and prolonged timelines for single-family entry. These dynamics suggest the region will continue favoring those with established equity or higher earnings, while first-time buyers face extended waits or alternative paths like condominiums.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Question: With first-time buyers now commonly having to wait until 40 to purchase a detached home in the Portland Region, what trade-offs are younger households making today to eventually break into ownership?

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Q3 2025 data shows only 10% of detached homes in the Portland Region were affordable to typical 25–44 households under realistic PITI assumptions using the Portland Appraisal Blog Affordability Index—explaining why first-time buyers have little choice but to wait until age 40.

Classic Craftsman bungalows homes in a Portland neighborhood. While older detached stock like this offered relatively better access for younger buyers in Q3 2025 (15% affordable in Multnomah County under realistic PITI assumptions), many close-in properties commanded premium prices—this example on the right sold for $1.1 million. Photo: Abdur Abdul-Malik, Portland Appraisal Blog

The National Association of Realtors recently reported that the median age of first-time home buyers has reached 40—the highest on record—with their share of purchases falling to a historic low of 21%. These trends are driven by affordability challenges that national indices like NAR’s Housing Affordability Index attempt to measure.

Using NAR’s standard methodology (principal and interest only, 25% qualifying ratio), approximately 28% of Q3 2025 detached single-family sales in the six-county Portland region were affordable to a household earning the area’s median income of $124,100.

In reality, no buyer escapes property taxes or homeowners insurance. When we incorporate actual taxes from listings and a conservative insurance estimate into the full monthly payment (PITI, 28% ratio), affordability drops to 20% for that same benchmark household.

To provide a more accurate local measure, this analysis introduces the Portland Appraisal Blog Affordability Index (PABAI)—a PITI-based index designed for the Portland Region’s residential market. Like traditional housing affordability indices, the PABAI expresses affordability as an index value where 100 means a household at the reference median income can exactly qualify for the typical home under realistic lending conditions. Values below 100 indicate unaffordability. A secondary calculation—the percentage of sales affordable to that reference household—derives directly from the index and serves as the primary insight in this post. For the overall Portland Region benchmark (using HUD’s Area Median Income of $124,100), the PABAI stood at approximately 78—confirming an unaffordable market even before drilling into younger households.

The challenge is even more severe for the cohort most people associate with first-time buyers: households headed by someone aged 25–44. With a median income of approximately $110,000 (2024 American Community Survey estimate), the PABAI drops to 69—meaning the typical younger household fell 31% short, with only 9.8% of Q3 detached sales (460 homes out of 4,682) within reach. The typical $600,000 detached home required roughly $159,000 in household income—45% above the cohort median.

Q3 2025 Affordability for Younger Buyers — County by County

Q3 2025 PABAI modeling reveals stark geographic variation for households aged 25–44.

County

Median Q3 Price

Required Income for Median Home

% of Sales Affordable: 25–44 Age Group

Columbia

$471,000

$122,000

34%

Yamhill

$510,000

$132,000

23%

Multnomah

$555,000

$150,000

15%

Clackamas

$675,000

$178,000

5%

Washington

$625,000

$165,000

3%

Hood River

$773,000

$195,000

3%

Regional

$600,000

$159,000

10%

Percentage of Q3 2025 detached sales affordable to typical 25–44 household under the PABAI (PITI model). Affordability modeled using 20% down payment, 28% front-end ratio, actual weekly rates, listing taxes, and 0.40% annual insurance estimate. Data: RMLS | Portland Appraisal Blog

Under the PABAI, outer counties like Columbia (34%) and Yamhill (23%) offered the highest shares of reachable detached homes, but this comes with trade-offs. Homes in these more rural areas typically involve longer commute times to Portland’s core amenities, job markets, and urban services—a key consideration for households prioritizing proximity over initial affordability. More urban Multnomah (15%) outperformed the pricier suburban counties of Washington (3%) and Clackamas (5%). Hood River’s premium inventory made it effectively inaccessible at just 3%.

The suburban counties’ low accessibility reflects their inventory mix. Clackamas County’s average lot size in Q3 sales was 1.07 acres—significantly larger than Washington County’s 0.36 acres or Multnomah’s 0.27 acres—contributing to higher median prices and required incomes well above the 25–44 cohort median. Larger lots and newer improvements demand stronger buyer qualifications, while Multnomah’s denser, older stock provided relatively more options for younger households.

The Realistic Paths to Ownership for Younger Buyers

For most households in their 20s and 30s, entry into the detached-home market in Q3 2025 required one of three things:

Substantial family assistance (gift for down payment, co-signer, or direct equity help).

Extreme lifestyle sacrifice (aggressive saving for larger down payment, renting with multiple roommates far longer, minimal discretionary spending).

Outlier household income (well above the cohort median—e.g., $150,000+ dual incomes early in careers).

Without one of these, even well-qualified younger buyers were effectively priced out until they aged into higher earnings—typically the late 30s or early 40s. Or they had to consider alternative housing options, like condominiums or townhouses.

This dynamic directly explains the national shift toward older first-time buyers and underscores the limited market participation of younger cohorts in the current environment.

Methodology Note

This analysis introduces the Portland Appraisal Blog Affordability Index (PABAI)—a PITI-based metric designed for the Portland region’s residential market (detached single-family, attached homes, condominiums, and manufactured homes on owned land). The PABAI measures the percentage of sales affordable to a reference household under realistic lending conditions. The PABAI can be calculated for distinct property types or the residential market as a whole. For this post, the PABAI is calculated for detached single-family homes only.

Affordability is modeled using a 20% down payment, 28% front-end housing expense ratio (per Freddie Mac guidelines), actual weekly 30-year fixed rates at closing, property taxes from listings, and a conservative 0.40% annual homeowners insurance rate (aligned with 2025 Oregon averages per Bankrate). Unlike national indices that rely on principal and interest only, the PABAI incorporates full PITI for a more accurate reflection of buyer qualification in the Portland region.

For an overall regional benchmark, the PABAI uses HUD’s Area Median Income for a 4-person household in the Portland–Vancouver–Hillsboro MSA ($124,100 as of 2025). In Q3 2025, the PABAI for this benchmark stood at approximately 78—meaning the typical household at the area median income could afford about 20% of detached sales under realistic PITI assumptions.

Reference incomes for specific age cohorts are estimated from the U.S. Census Bureau’s 2024 American Community Survey (Table B19037) using standard linear interpolation on grouped income data. For households aged 25–44, this yields an estimated median of approximately $110,000. This lowers the PABAI to approximately 69 for this age band, placing only 9.8% of Q3 2025 detached sales within reach.

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

Q3 2025 RMLS data shows the Portland Region’s detached starter homes (5th–35th percentile) average $469k and are dominated by mid-century builds on larger lots—with new construction offering modern features but far less space. Appraisal and buyer insights below.

A classic early-20th-century bungalow in the Portland area—the type of modest, well-loved home that dominates today’s starter-tier inventory. Via Canva Pro

Earlier this month, Redfin highlighted Portland as one of the stronger markets nationally for starter-home activity, defining starter homes as sales in the 5th–35th percentile by price. We adopt the same percentile convention here for consistency.

Redfin’s reported median of approximately $420,000 for Portland starter homes includes all property types (condos, townhomes, and single-family). Focusing solely on detached single-family residences—a popular choice across the region, including for many urban buyers seeking yard space and privacy over attached ownership—Q3 2025 RMLS data for the 5th–35th percentile tier shows an average close price of $469,000.

Few would be surprised that new construction plays a limited role in true entry-level pricing—after all, building costs remain elevated. Yet the data shows builders are still delivering a modest but meaningful number of brand-new homes into this tier (about 4.2% of starter sales, compared to 9.1% across the full market). This demonstrates that, through efficient design, infill strategies, and lot divisions, new product can compete in the lower price bands.

Local buyers want to know: how much home does a starter budget actually buy? This analysis examines square footage, lot size, build era, and location differences across counties—revealing a market dominated by mid-century homes with a modest but noteworthy presence of brand-new construction.

How Much Home a Starter Budget Buys by County

The table below summarizes Q3 2025 closed sales for detached single-family homes in the 5th–35th percentile across the core Portland Region counties (Hood River row excluded due to only two qualifying sales).

County

Avg Close Price

Avg Yr Built

Avg Total SF

Avg Acres

# of Sales

Clackamas

$474,738

1965

1,553

0.279

256

Columbia

$457,108

1983

1,774

0.617

58

Mult.

$459,909

1951

1,591

0.163

666

Wash.

$488,954

1976

1,495

0.154

323

Yamhill

$453,522

1981

1,532

0.197

113

Grand Total

$468,595

1963

1,565

0.203

1,418

Data: RMLS | Portland Appraisal Blog

Multnomah County drives nearly half the volume, delivering the oldest average build year (1951). Washington County posts the highest average prices and hosts the most new construction. Outer counties like Columbia and Yamhill provide newer homes on larger parcels, though with far fewer transactions.

Surprisingly, across the region, starter homes are very similar in average price. The standard numerical metrics which are easy to see in RMLS, (e.g. total square footage, lot size, year built, etc.), are not the primary determinant of value. As we shall see, what matters more is quality, condition, and overall site & functional utility. Buyers in the starter home tier make conscious trade-offs between older homes with larger lots and newer homes with little to no functional backyard.

Of all the standard numeric metrics, total square footage shows one of the stronger relationships with price in the starter tier—though the influence is still modest.

Close Price vs. Total Square Feet for Starter-Tier Detached Homes ≤ 0.5 Acres (Q3 2025 RMLS data – 1,380 observations). Note: The Y-axis begins at $350,000 to allow for better viewing of the dataset.

Larger homes tend to sell for higher prices, though with considerable variation—most sales fall between 1,200 and 2,000 square feet. The very slight tilt to the right indicates a weak but present relationship between starter home size and close price. The coefficient of determination (R2) for this graph is 0.1253, meaning total square footage explains only about 12.5% of the variation in price. Since total square footage is often one of the primary determinants of value in the broader housing market, this is a big clue that the size of the home isn’t the primary factor for buyers looking to enter the starter home market.

The Historical Supply Pattern: Lot Size and Build Era

Portland’s entry-level inventory bears the clear imprint of the post-war building boom.

Lot Size vs. Year Built for Starter-Tier Detached Homes ≤ 0.5 Acres (Q3 2025 RMLS data – 1,380 observations).

A polynomial trendline highlights the peak lot sizes during the 1940s–1950s post-war era, followed by a steady decline that began in the early 1960s and accelerated in recent decades. The pattern reflects an era when generous lots were standard, followed by shrinking parcels as land values rose, urban growth boundaries took effect, and lot divisions became common. Buyers choosing older starter homes today typically gain significantly more outdoor space than those selecting new construction.

New Construction: A Modest but Noteworthy Presence

While new homes account for only 4.2% of starter-tier sales, their ability to reach this price range in a high-cost building environment remains impressive.

Segment

Avg Close Price

Avg Total SF

Avg Acres

# of Sales

Existing

$467,996

1,569

0.207

1,359

New

$482,387

1,479

0.107

59

Grand Total

$468,595

1,565

0.203

1,418

Data: RMLS | Portland Appraisal Blog

New homes sell for only about 3% more than existing ones despite brand-new condition, but deliver less interior space and roughly half the land.

Buying a new home in the starter tier is akin to buying a new car on a tight budget: you gain the benefits of fresh systems, modern design, and warranty peace of mind, but often in a smaller package with fewer amenities compared to a well-maintained used model from a higher trim line.

County

Avg Close Price

Avg Yr Built

Avg Total SF

Avg Acres

# of Sales

Clackamas

$489,803

2025

1,606

0.154

8

Columbia

$420,000

2025

1,458

0.130

2

Mult.

$450,820

2025

1,098

0.088

18

Wash.

$509,366

2025

1,699

0.079

25

Yamhill

$475,578

2025

1,540

0.216

6

Grand Total

$482,387

2025

1,479

0.107

59

Data: RMLS | Portland Appraisal Blog

For buyers, this creates a clear choice: a brand-new home with modern efficiency but typically on a very small lot—often with minimal or no usable yard space, especially in Multnomah and Washington counties where most new construction occurs—or an existing mid-century home that generally offers significantly more land and outdoor space, albeit with the potential challenges of older systems and layouts. This trade-off is particularly relevant for growing families or those prioritizing play areas, gardens, or privacy.

Appraisal Insights and Challenges

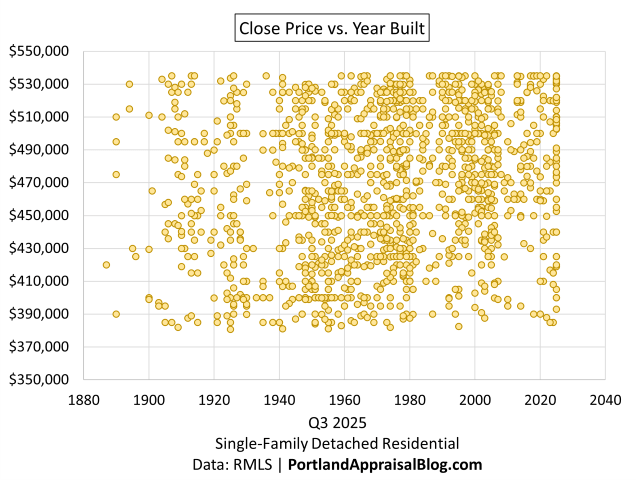

One of the most revealing patterns appears when plotting close price against build year.

Close Price vs. Year Built for Starter-Tier Detached Homes ≤ 0.5 Acres (Q3 2025 RMLS data – 1,380 observations). Note: The Y-axis begins at $350,000 to allow for better viewing of the dataset.

The remarkably consistent price band across decades illustrates that chronological age has little direct influence on value in the Portland Region’s entry-level segment.

In this tier, actual age correlates weakly with sales price because buyers weigh multiple factors:

Functional obsolescence in mid-century stock (outdated floor plans, smaller kitchens/bathrooms, less efficient systems) is often mitigated by updates and strong location appeal.

Effective age and condition drive far more of the value than the original build date.

Lot size and site utility frequently favor older homes; the smaller parcels common in new construction require substantial negative adjustments that offset much of the credit for new condition.

Comparable selection remains within county, where abundant mid-century comps in Multnomah, Clackamas, and Washington provide solid support — but thinner volume in outer counties demands careful bracketing.

When appraising a new-construction home in this tier—where truly similar recent sales are still limited and down approximately 25% year-over-year in Q3 2025 (with Multnomah County off 48%)—appraisers typically rely on other relatively recent builds (often within 10 years) and apply appropriate adjustments for differences in site characteristics, size, and location.

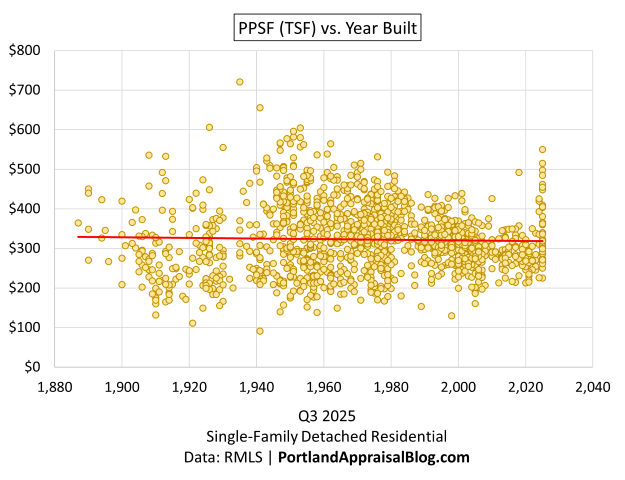

The same pattern holds when looking at the data from a price-per-square-foot lens, but with a slight twist:

PPSF (TSF) vs. Year Built for Starter-Tier Detached Homes ≤ 0.5 Acres (Q3 2025 RMLS data – 1,380 observations).

From the 1950s onward, PPSF becomes progressively more compressed—older homes exhibit wide spreads driven by dramatic differences in condition, updates, historic appeal, and location premiums, while mid-era and late-20th-century stock tightens as market expectations and remodeling homogenize perceived value.

Brand-new 2025 homes, however, break this decades-long compression pattern. Their PPSF spreads out again, reflecting greater influence from location-driven land costs and builder-specific choices (e.g., finishes, lot configuration) rather than the uniformity imposed by age and updates on existing stock. In effect, today’s entry-level new construction reintroduces variation that mirrors pre-1950 homes—but for different reasons: land value dominance and strategic specs to hit price points, rather than condition swings. This underscores why new-construction starter homes often form their own submarket. Appraisers valuing them face a narrower but distinct comp pool.

These dynamics show that the starter home market is not uniform and the appraiser needs to carefully delineate the competitive market segment to avoid having to make large adjustments between disparate properties. One technique appraisers often employ is to use similar, but older sales when recent data is thin and make an appropriate market conditions adjustment.

Conclusion

The Portland Region’s Q3 2025 starter-home segment continues to rely predominantly on mid-century inventory on lots larger than anything new we’re building today—a pattern unlikely to shift dramatically in 2026 absent major changes in new supply. (Although the City of Portland is certainly trying to incentivize new projects with SDC waivers.) The modest foothold of new construction shows builders adapting through infill and efficient design, but at the clear cost of site size and outdoor space.

For buyers, the choice boils down to priorities: modern and low-maintenance on a small lot, or more space and yard with the realities of an older home. For appraisers, lenders, and agents, recognizing how effective age, site utility, location, and condition outweigh chronological age remains key to accurate valuation in this segment.

Portland’s Temporary SDC Exemption for New Housing Units (2025–2028): Portland Appraisal Blog

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

How pre-1997 Portland metro homes—especially those with veteran or active-duty exemptions—are facing sudden property tax jumps on sale or disqualification.

A classic pre-1940 home in the Portland Region – the type of property often benefiting from deep Measure 50 tax compression. Photo: Portland Appraisal Blog

Imagine closing on a well-maintained pre-1940 Craftsman in an established close-in Portland neighborhood. The sale price felt fair, the taxes shown on the listing and county statement appeared reasonable, and the transaction cleared due diligence without issue. Then the next year’s tax bill arrives—$2,000 to $6,000 higher than anticipated. The increase isn’t due to a sudden spike in market value, but to a change in how Oregon counties now calculate Maximum Assessed Value (MAV) when certain partial property tax exemptions end.

This situation is no longer hypothetical. Oregon REALTORS first highlighted the risk in a December 12th, 2025 internal “Forms Tip of the Week” communication, alerting members that the loss of veteran or active-duty partial exemptions—commonly triggered when a qualifying veteran or surviving spouse sells the home or passes away without a qualifying successor—can lead to significant tax increases under updated guidance from the Oregon Department of Revenue.

While the veteran and active-duty exemptions (ORS 307.250 and 307.286) have drawn attention to the issue, the underlying driver is broader: the substantial tax compression created by Measure 50 for properties built or long-held before 1997.

Historically, when these modest partial exemptions ended, counties simply removed the discount and allowed the low underlying MAV to continue. The 2024 guidance change now enforces a constitutional requirement to reset MAV closer to current market reality upon disqualification.

The outcome: buyers may face permanently higher carrying costs they did not expect, sellers (including veterans and surviving spouses) can find their properties harder to market at full value, and appraisers encounter a marketability factor worthy of note when present.

This Deep Dive reviews the mechanics, illustrates the pattern with Portland Region sales data, and provides practical steps for identifying and addressing the issue in appraisal assignments.

Understanding Measure 50: The Foundation of Tax Compression

To grasp why the loss of a veteran or active-duty exemption can now lead to significant tax increases, we must first understand Oregon’s Measure 50 property tax system, approved by voters in 1997.

Measure 50 replaced the previous tax structure with two key values for each property:

Real Market Value (RMV): The county assessor’s estimate of what the property would sell for on the open market. This value can rise or fall annually with market conditions.

Maximum Assessed Value (MAV): A separate taxable value created by Measure 50. For existing properties in 1997, MAV was initially set at approximately 90% of the 1995–1997 RMV. Thereafter, MAV is generally limited to a 3% annual increase, with exceptions for major additions, improvements, or certain other events.

The Assessed Value (AV) is the lesser of RMV or MAV. Taxes are calculated by multiplying the AV by the local tax rate.

In high-appreciation markets like the Portland metro area, this 3% cap creates substantial tax compression over time. A home purchased or built before 1997 can have an MAV far below its current RMV after decades of strong market growth.

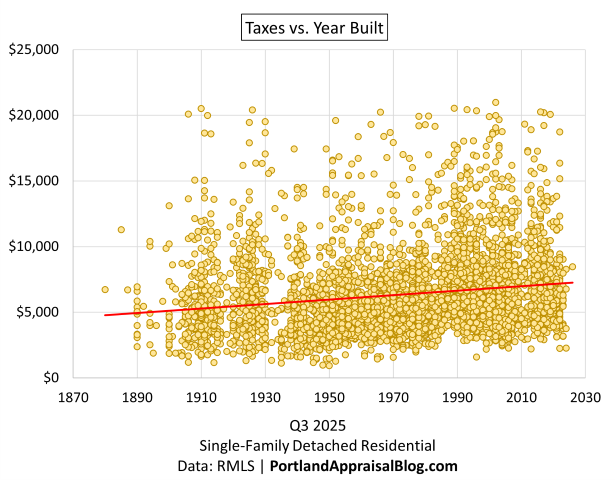

Annual property taxes vs. Year Built, excluding new construction and obvious data errors. Note: Scatter plots are limited to properties with annual taxes of $21,000 or less to highlight the primary distribution and improve readability.

The scatter illustrates the effect clearly: pre-1960 homes are overwhelmingly clustered below $10,000–$12,000 in annual taxes, with the densest grouping under $8,000–$9,000. Properties on the far left (pre-1920 builds) often show the deepest compression, having benefited from the longest period of capped MAV growth. Post-1990 homes, by contrast, display significantly higher tax burdens, reflecting less historical compression.

When a triggering event occurs—such as disqualification from a partial exemption—the MAV can be recalculated using the Changed Property Ratio (CPR), typically around 0.54 for residential properties in Portland Region counties for the 2025–2026 tax year, applied to current RMV.

In the next section, we examine local sales data that quantifies the scale of this compression and illustrates why the reset can matter in real transactions.

The Data: Tax Compression in the Portland Metro Market

Q3 2025 sales data from detached single-family residences (SFR) in the Portland Region (Clackamas, Columbia, Hood River, Multnomah, Washington, and Yamhill counties) illustrates the scale of Measure 50 compression and why a MAV reset can create material differences in carrying costs.

The table below summarizes average sale prices and annual property taxes by approximate decade built. Flagged new construction is excluded due to frequently incomplete or preliminary tax assessments at the time of sale, which can distort the pattern of long-term compression. This brings the Q3 2025 dataset to 4,256 sales total.

Decade Bucket

Avg Sale Price

Avg Annual Taxes

Avg Tax per $1k Sale Price

Pre-1940

$671,295

$6,396

$9.33

1940–1959

$607,466

$5,766

$9.53

1960–1979

$640,000

$5,783

$9.16

1980–1999

$714,535

$7,367

$10.31

2000–2019

$761,061

$7,685

$10.10

2020+ (non-new construction)

$924,420

$8,016

$9.12

Grand Total (excluding new construction)

$688,838

$6,665

$9.68

Data: RMLS | Portland Appraisal Blog

Several patterns stand out:

Absolute tax burden increases with newer construction: pre-1980 homes average $5,766–$6,396 in annual taxes, while 2000–2019 properties average $7,685 and 2020+ non-new construction reaches $8,016.

Effective burden consistency: The Tax per $1k column remains remarkably stable at ~$9–$10 across all eras. This indicates the market prices properties assuming a similar overall tax load, regardless of age.

Pre-1940 premium: Outside recent construction, pre-1940 homes command the highest average sale prices ($671,295) despite paying among the lowest absolute taxes.

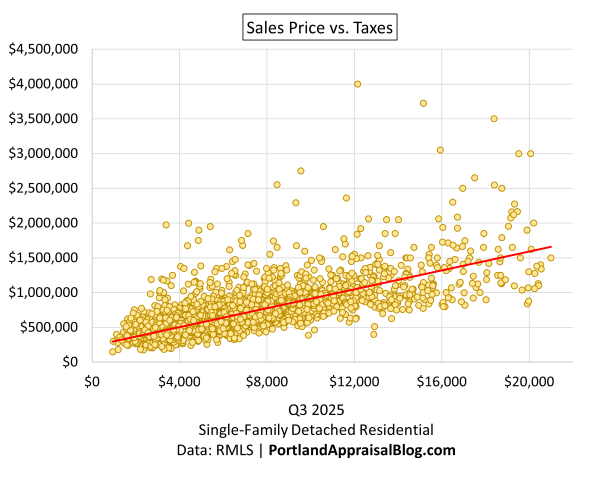

Street sign in Portland’s Historic Irvington neighborhood—one of the areas with many high-value pre-1940 homes exhibiting significant Measure 50 compression. Photo: Portland Appraisal Blog (CC BY-SA 4.0)Sale price vs. annual taxes, excluding new construction and obvious data errors. Note: Scatter plots are limited to properties with annual taxes of $21,000 or less to highlight the primary distribution and improve readability.

This scatter shows a strong positive correlation, confirming the market efficiently incorporates expected tax burden into pricing.

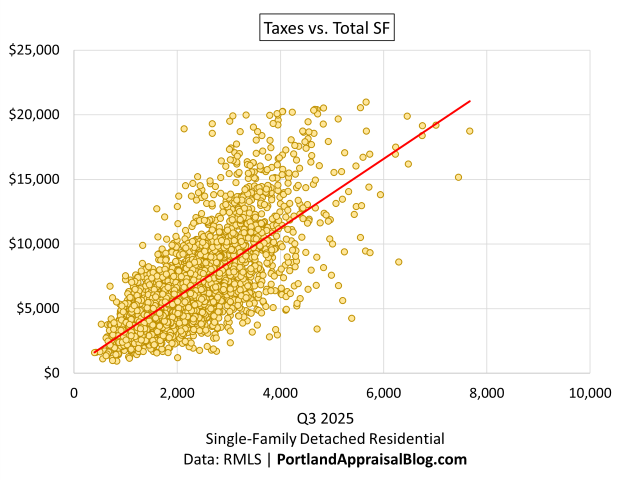

Annual taxes vs. total square footage, excluding new construction and obvious data errors. Note: Scatter plots are limited to properties with annual taxes of $21,000 or less to highlight the primary distribution and improve readability.

Here, numerous low-tax outliers are visible below the trend line—properties paying substantially less than size and location would otherwise suggest, consistent with Measure 50 compression.

Taken together, the data reveals a market that rewards older stock with lower absolute taxes without discounting sale prices accordingly. When a MAV reset occurs, absolute taxes move toward levels seen in newer comparable properties, creating the potential for noticeable increases in annual carrying costs.

In the following sections, we explore the specific veteran and active-duty exemptions and the 2024 guidance change that can trigger this alignment.

The Veteran and Active-Duty Exemptions

The exemptions at the center of the current concern are partial property tax reductions for certain military veterans, surviving spouses, and active-duty service members. With approximately 267,000 veterans living in Oregon (and over 114,000 in the Portland metro region), even a fraction of qualifying owners selling or changing status can affect a meaningful number of transactions.

The disabled veteran or surviving spouse exemption (ORS 307.250) provides a reduction to assessed value for homeowners with a service-connected disability rating of 40% or higher (or unremarried surviving spouses). For the 2025–2026 tax year, the reduction is up to $31,565 (service-connected) or $26,303 (standard), worth roughly $400–$700 in annual tax savings in Portland metro areas depending on local rates.

A separate active-duty exemption (ORS 307.286) offers a larger reduction (up to $108,366 for 2025–2026) for Oregon-domiciled service members on qualifying active duty outside the state.

Both are partial exemptions applied to the assessed value of the owner’s primary residence and tied to personal status. Eligibility generally requires a one-time application and VA certification (re-filing needed only if moving to a new property or certified by a private physician rather than the VA).

While the direct savings from these exemptions is modest ($400–$700/year for most veteran claims), the 2024 DOR guidance change treats their disqualification as triggering a full MAV reset—potentially closing decades of Measure 50 compression and leading to significantly higher taxes.

Active-duty cases (e.g., exemption ending upon return home) are less common and typically involve properties with less historical compression.

In the next section, we detail the 2024 guidance change and how it activates the reset.

The 2024 Rule Change

For decades, when a veteran or active-duty partial exemption ended, county assessors typically removed the reduction but preserved the underlying compressed MAV, allowing it to continue growing at the standard 3% rate.

This practice changed with updated guidance from the Oregon Department of Revenue, effective for disqualifications on or after January 1, 2024.

The DOR clarified that disqualification from a partial exemption triggers the constitutional requirement to recalculate MAV using the Changed Property Ratio (CPR)—the county-wide ratio of average MAV to average RMV for the property class. The new MAV becomes current RMV multiplied by the CPR (typically around 0.54 for residential properties in Portland Region counties for the 2025–2026 tax year).

This administrative enforcement of the existing constitutional language means the modest exemption savings ($400–$700/year) is no longer the only consequence. The reset can close much of the Measure 50 compression gap.

In the Portland Region data, pre-1980 homes average $5,766–$6,396 in taxes. A reset aligns absolute taxes closer to 2000+ levels ($7,685–$8,016 average), producing increases commonly in the $1,500–$4,000 annual range on typical sales, with $4,000+ possible in deeper-compression or higher-rate scenarios.

The change is statewide, though impacts vary by local appreciation and rates. Some counties have noted the potential for “significant increase” on loss of exemption.

In the next section, we examine the real-world implications for transactions and what appraisers should watch for.

Real-World Implications

The 2024 guidance change does not turn every pre-1997 home sale into a crisis, but it introduces friction that can affect negotiations, marketability, and reconciliation of comparables.

Typical tax increases fall in the $1,500–$4,000 annual range for properties in the Portland Region dataset ($600,000–$800,000 sale prices with pre-1980 build years). This translates to $125–$333 extra per month.

The Silent Car Payment

In late 2025 terms:

Average used-car payment: ~$532/month

Average new-car lease: ~$596/month

Average new-car purchase payment: ~$748/month

A $2,000–$4,000 annual increase ($167–$333/month) is less than a typical car payment but still noticeable—equivalent to a permanent, non-negotiable “utility bundle” that never goes away. For buyers already stretched in a higher-interest-rate environment, it can shift affordability and prompt renegotiation.

Outlier cases with deeper compression (often “sweet” pre-1940 homes in high-appreciation locations) can see $4,000–$8,000+ increases ($333–$667/month)—territory overlapping average used-car or new-lease payments. These are the transactions Oregon REALTORS described as producing “increases in the thousands,” sometimes requiring substantial seller concessions or risking fallout during due diligence.

The primary impact is often on marketability rather than outright deal death:

Savvy buyers (or their agents/lenders) anticipate the higher future taxes and adjust offers downward.

Sellers—particularly veterans or surviving spouses downsizing—may receive lower net proceeds (capitalizing a $3,000 increase at 6% equates to ~$50,000 less effective value).

Listings can linger if the low current taxes mask the post-closing reality.

For appraisers, this creates a new lens for outliers:

A comparable with an unexplained lower price, large concession, or extended days on market may reflect buyer reaction to a pending MAV reset.

Low-tax outliers in the grid (visible in the Taxes vs. Total SF scatter) could indicate compressed MAV or an active exemption—worth verifying via county records when material.

The change is statewide, but effects are most pronounced in areas with strong historical appreciation, like the Portland Region.

In the next section, we outline practical steps appraisers can take to identify and address this factor in reports.

What Appraisers Should Do

The 2024 guidance change introduces a marketability factor that appraisers in Oregon should consider when the subject or comparables involve pre-1997 properties, particularly those with potential veteran or active-duty exemptions.

Practical Checklist

Verify Exemption Status Review county tax records and the preliminary title report (if available) for indications of an active veteran, surviving spouse, or active-duty partial exemption. Many counties list it on the property tax statement or online portal.

Estimate Post-Transfer Tax Liability If an exemption is present and likely to disqualify on transfer (e.g., sale to non-qualifying buyer), note the potential increase. Use county assessor tools or CPR data to project the reset MAV (current RMV × CPR) and resulting taxes. Typical jumps in the Portland Region fall in the $1,500–$4,000 annual range, with higher amounts possible in deep-compression cases. Note that tax rates vary by code area.

Comment on Marketability When Material Include commentary if the differential is significant: “The subject property currently benefits from a veteran partial exemption expected to end upon transfer, potentially increasing annual taxes by an estimated $X. This may affect buyer affordability and market reaction.”

Reconcile Outliers with This Lens Low-tax outliers in the sales grid (visible in Taxes vs. Total SF analysis) may reflect compressed MAV or an active exemption—a “decaying asset” under the new guidance. Check effective tax rate (annual taxes ÷ sale price): ~0.6–0.8% may indicate compression; consider post-reset alignment (~1.1–1.3%) in reconciliation. Using a compressed comparable without adjustment risks overvaluing the subject’s marketability, as savvy buyers increasingly factor in the reset.

Use Dual Scenarios if Appropriate For subjects with active exemptions, provide current and projected post-reset tax estimates in the addendum or comments to inform the intended user.

Resources:

County assessor websites (tax statements often flag exemptions)

DOR Veteran Exemptions page

MAV Manual for general mechanics

As resets propagate into closed sales (expected more visibly in 2026 onward), this factor may explain otherwise puzzling comparables. Early identification helps ensure accurate valuation and informed clients.

In the closing section, we look at the broader outlook.

Closing Thoughts

The 2024 DOR guidance change is an administrative enforcement of a long-standing constitutional provision, but its impact is only now becoming visible as disqualifications occur and 2025–2026 tax statements arrive. Larger effects are expected in the 2026–2027 cycle as more veteran-owned properties sell or change status.

The 2025 Oregon Legislative Session saw bills (e.g., HB 2361/SB 387 aiming to lower the disability threshold, HB 3287 to increase exemption amounts) intended to expand veteran benefits. While these efforts highlight recognition of the issue, none addressed the MAV reset trigger itself. The constitutional requirement remains unless amended or re-interpreted.

For appraisers working in the Portland Region and similar appreciation-driven markets, this issue adds one more layer to marketability analysis. Low-tax outliers in older properties represent a benefit that can evaporate on transfer—reliable today, but potentially “decaying” tomorrow.

Awareness helps everyone involved: appraisers reconcile comparables more accurately, agents counsel clients proactively, and buyers/sellers avoid surprises.

If you encounter real-world examples (anonymized comps with concessions due to reset concerns, or listings noting the risk), please share them for future updates. Documenting patterns strengthens our collective understanding.

Thank you for reading this Appraisal Deep Dive. Stay informed and precise in your work.

Quick Reference Cheat Sheet

Reset Formula

Real Market Value (RMV) × Changed Property Ratio (CPR)

Typical CPR (2025–2026, Portland Region residential)

~0.54 (updated annually each October)

Reset Trigger

Disqualification from veteran/active-duty exemption

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

CODA

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.

{kind=link}

{kind=link}