Photo: Abdur Abdul-Malik, Portland Appraisal Blog

Introduction

The first quarter of 2026 was a study in contrasts across the Portland region’s attached‑home market. The three major counties—Multnomah, Washington, and Clackamas—continued to anchor the segment, each revealing its own distinct pattern of demand, pricing behavior, and builder activity. Together they formed the core of the regional story: softer prices, steady buyer engagement, and a noticeable shift in how builders are positioning new product. Beneath those broad themes, however, each county expressed the quarter differently, shaped by its inventory profile, geography, and development pipeline.

Washington County remained the region’s most uniform and predictable attached‑home market, with tight clustering in the mid‑price bands and a clear, data‑driven softening that still preserved strong absorption. Multnomah showed more variation, with affordability improving and pricing adjusting in a way that reflected both buyer sensitivity and the county’s diverse housing stock. Clackamas, by contrast, continued to operate at a higher price level, with a dense band of activity in the low‑$400s and a meaningful upper‑tier presence. Builders in Clackamas also made a notable pivot toward smaller new‑construction units—a strategic response to qualification thresholds that shaped the quarter’s pricing dynamics.

Outside the “Big Three,” the story was defined not by trends but by scale. Yamhill, Columbia, and Hood River each recorded only a handful of attached‑home sales, and their year‑over‑year changes reflected the volatility inherent in extremely small datasets. In these counties, a single closing can shift averages dramatically, and the absence of just a few transactions can reshape dollar volume.

Taken together, Q1 2026 shows a region adjusting to softer demand with realistic pricing, steady buyer participation, and builder strategies increasingly aligned with affordability constraints.

Table of Contents

- Data Housekeeping

- Residential Housing Snapshot

- Portland Region Q1 2026 Overview

- Multnomah County Q1 2026 Stats

- Washington County Q1 2026 Stats

- Clackamas County Q1 2026 Stats

- Yamhill County Q1 2026 Stats

- Columbia County Q1 2026 Stats

- Hood River Q1 2026 Stats

- Closing Thoughts

- Sources & Further Reading

- Coda

Data Housekeeping

The Portland Region in this update comprises the six Oregon counties of Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill. These counties form a contiguous housing ecosystem centered on Portland—Multnomah as the core home county, with the others tightly integrated through commuting patterns, economic ties, and shared market dynamics (e.g., Yamhill’s strong connection via Highway 99W and wine-country adjacency). Beyond Yamhill, the MLS system changes, further distinguishing this six-county area from broader geographic aggregations. For a detailed overview—including county profiles, population data, key value influencers, and why this definition differs from the official seven-county Portland–Vancouver–Hillsboro MSA—see the dedicated page: The Portland Region – Six-County Market Area Overview.

Via SunCatcherStudio

All data is sourced from RMLS and reflects open-market attached single-family residential sales. SNL (“Sold Not Listed”) entries—off-market transactions entered retroactively—have been excluded to preserve consistency with true market activity.

All figures have undergone a standard cleaning process to address common RMLS accuracy challenges, including misclassifications (such as condominiums listed as attached homes), square‑footage and price entry errors, incomplete fields, status/date mismatches, and other non‑representative entries. This post focuses exclusively on attached homes on owned land; while a condominium townhome and an attached townhome may appear similar, their ownership structures differ substantially. Condominiums are therefore carefully removed from this dataset. For a detailed overview of these issues, their impact on market analysis, and the mitigation steps used (automated flagging, cross‑verification, and manual review), see the dedicated page: RMLS Data Accuracy Challenges.

Portland Appraisal Blog Affordability Index (PABAI)

What PABAI Measures

The Portland Appraisal Blog Affordability Index (PABAI) measures how home sale prices compare to what a median‑income household can qualify for under standard lending assumptions (HUD Portland‑Vancouver‑Hillsboro MSA median income, 20% down, and a 28% DTI for principal, interest, taxes, insurance, and HOA dues).

Unlike national affordability indices, PABAI is built from actual RMLS transactions rather than a single hypothetical price point. It computes an affordability ratio for every closed sale in the Portland Region during Q1 2026 and then averages those results—that average is the reported PABAI. Each housing segment—detached, attached, condos, and manufactured—is calculated separately, ensuring that segment‑specific dynamics are preserved rather than blended together. This approach produces far more precise, locally grounded insights into Portland‑area affordability and avoids the distortions that occur when fundamentally different housing types are combined into a single regional metric.

A PABAI of 100 means the market is exactly affordable at that income level (the Q1 2026 HUD median MSA income was $124,100 for a family of four). Values above 100 indicate excess qualifying capacity (more affordable), while values below 100 indicate a shortfall (strained affordability). Full methodology and the interpretation scale are available on the PABAI explainer page.

| PABAI Range | Interpretation |

|---|---|

| 120+ | Strongly Affordable |

| 100–119 | Moderately Affordable |

| 80–99 | Strained |

| Below 80 | Severely Constrained |

Note: While every sale produces an affordability ratio, the PABAI itself requires at least 20 sales to be statistically meaningful. Counties with fewer than 20 attached sales will report affordability counts and percentages, but not a PABAI.

Residential Housing Snapshot

| Metric | Detached | Attached | Condo | Manufact. |

|---|---|---|---|---|

| Total $ Volume | $2.2B | $161.0M | $199.0M | $31.8M |

| Average Price | $659,197 | $444,672 | $389,438 | $547,486 |

| Avg PPSF (TSF) | $316.17 | $286.91 | $325.56 | $361.83 |

| Avg Total SF | 2,164 | 1,576 | 1,180 | 1,570 |

| Avg Age (Yrs) | 46.03 | 15.09 | 32.03 | 29.52 |

| Avg Lot Size (ac) | 0.655 | 0.066 | N/A | 8.228 |

| Avg PABAI | 80.47 | 104.13 | 117.08 | 110.07 |

| Highest Sale | $5,725,950 | $1,175,000 | $2,450,000 | $2,400,000 |

| Lowest Sale | $135,000 | $249,000 | $100,000 | $199,700 |

| Price Spread Ratio | 42.41 | 4.72 | 24.50 | 12.02 |

| PPSF Spread Ratio | 30.93 | 4.08 | 11.91 | 13.29 |

| SF Spread Ratio | 23.46 | 4.14 | 12.24 | 3.52 |

| Avg CDOM | 80.23 | 80.59 | 119.62 | 120.86 |

| Total # of Sales | 3,349 | 362 | 511 | 58 |

| % of Market | 78.25% | 8.46% | 11.94% | 1.36% |

Data: RMLS | PortlandAppraisalBlog.com

The four residential segments in the Portland Region continue to operate as a tightly connected ecosystem, each shaping and responding to the others in predictable ways. Detached homes remain the anchor segment—by far the largest in both sales count and dollar volume—and their scale sets the tone for regional pricing, land intensity, and buyer movement. With more than 3,300 sales and over $2.2 billion in closed volume this quarter, detached homes define the outer boundaries of what the market can deliver, from sub‑$150,000 fixers to multi‑million‑dollar estates. Their wide spread ratios across price, PPSF, and size reflect this internal diversity and underscore why detached remains the segment most buyers prefer even when affordability pushes them elsewhere.

Attached homes sit directly beneath detached in the regional hierarchy and serve as the clearest alternative when detached becomes harder to access. They are the youngest segment in the metro—averaging just over 15 years old—and the most uniform, with tight spread ratios that signal a highly consistent, commodity‑like product. Their average price of $444,672 and moderate affordability (PABAI 104.13) position them as the region’s primary safety‑net for buyers priced out of detached homes. The typical attached home is smaller, newer, and far more predictable in layout and utility than detached, and this consistency is a defining feature of the segment. In Q1 2026, attached homes represented 8.46% of all residential sales but played an outsized role in absorbing affordability‑sensitive demand.

Condos remain the most affordable segment in the region, with a PABAI of 117.08 this quarter, but affordability alone does not translate into broad appeal. They are also geographically concentrated: 67.71% of all condo sales occurred in Multnomah County, with most located in the City of Portland. This concentration reflects both historical development patterns and buyer preferences—condos are scarce or nonexistent in many suburban and rural areas where detached and attached homes dominate. Their average age is more than double that of attached homes, and HOA dues shape both buyer preferences and long‑term affordability. Condos make up nearly 12% of all Q1 sales yet contribute less than 8% of total dollar volume. Given the lower average price compared to all other segments, this gap is expected and reflects the structural role condos play in the ecosystem—an accessible option for some buyers, but not a proportional driver of regional dollar volume.

Manufactured homes represent the smallest segment by far, with only 58 sales this quarter. Their averages run high because many transactions include significant acreage—an average lot size of more than eight acres—and with such a small sample, outliers exert more influence on segment averages than in any other category. Manufactured homes share several surface‑level similarities with condos (age, CDOM, affordability), but diverge sharply in how they trade: manufactured homes trade on land, while condos trade on dues.

Across the ecosystem, three of the four segments cluster in the low–mid $300s PPSF, underscoring that structure cost is relatively consistent across the metro. It is land, size, dues, and buyer preferences that create the separation between segments. Detached homes show the widest internal variation, attached homes the tightest, condos a bimodal profile shaped by older stock and boutique new construction, and manufactured homes a land‑driven spread that reflects acreage more than dwelling characteristics. This snapshot frames the broader regional context and sets the stage for the attached‑home‑specific analysis that follows.

Portland Region Q1 2026 Overview

Overall Regional Trends

The table below summarizes key metrics for attached homes residential sales in the Portland Region (Columbia, Clackamas, Hood River, Multnomah, Washington, and Yamhill counties) for Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $154,193,082 | $160,971,196 | +4.40% |

| Average Price | $470,101 | $444,672 | -5.41% |

| Median Price | $442,425 | $420,250 | -5.01% |

| Avg SP/OLP | 97.30% | 96.31% | -1.02% |

| Avg PPSF (TSF) | $297.52 | $286.91 | -3.56% |

| Avg HOA Dues | $243.36 | $255.05 | +4.81% |

| Median HOA Dues | $215.50 | $233.00 | +8.12% |

| Avg Lot Size (ac) | 0.0621 | 0.0657 | +5.71% |

| Avg Age (Yrs) | 14.40 | 15.09 | +4.85% |

| Avg CDOM | 84.02 | 80.59 | -4.07% |

| Avg Total SF | 1,604 | 1,576 | -1.76% |

| Total # of Sales | 328 | 362 | +10.37% |

| # of New Constr. | 131 | 150 | +14.50% |

| # of REOs | 0 | 2 | — |

| # of Short Sales | 0 | 0 | — |

| Average PABAI | 88.39 | 104.13 | +15.74 pts |

| # Affordable | 67 | 222 | +155 homes |

| % Affordable | 20.43% | 61.33% | +40.90 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Key Observations From the Aggregate Data

The attached‑home segment softened meaningfully in Q1 2026, and the year‑over‑year comparison highlights a market adjusting to both price pressure and improved borrowing conditions. Average and median prices declined around five percent. This softness is not isolated—most counties saw similar declines—but Washington County’s dominance in attached‑home activity (51.38% of all regional sales) means its pricing trends exert the strongest pull on the regional averages. The ongoing impact of the Intel layoffs likely contributed to slightly faster market times, modestly lower prices, and a sharp improvement in affordability metrics.

Affordability is the standout story of the quarter. The segment flipped from strained to moderately affordable, with the PABAI jumping from 88 to 104.13. This is a substantial shift and reflects the combined effect of lower prices and better interest rates. The share of affordable attached homes surged from 20.43% to 61.33%, adding 155 more qualifying homes to the pool. This is not a compositional artifact; it is a direct response to improved lending conditions and softer pricing. When affordability improves, demand typically follows, and Q1 2026 delivered exactly that pattern.

Sales volume rose 10.37% year‑over‑year, and total dollar volume increased 4.40%. Importantly, the rise in dollar volume was driven by more sales, not higher prices. This distinction matters: it signals a market where buyers are re‑entering due to improved conditions rather than chasing rising values. The attached segment often acts as the pressure‑release valve for buyers priced out of detached homes, and this quarter’s data reinforces that role.

New construction played a meaningful part in the quarter’s dynamics. Closings increased from 131 to 150 (+14.50%), and Washington County accounted for roughly 60% of all new attached homes. This continues a multi‑year pattern in which Washington County favors new attached homes over new condos—a stark contrast to the condominium segment, which recorded zero new‑construction closings in Q1 2026. The slight increase in average age (14.40 → 15.09) despite more new construction indicates that the older resale stock still dominates the segment’s composition.

Market efficiency improved modestly. Cumulative days on market tightened from 84.02 to 80.59, and sellers yielded slightly more ground on pricing, with the average SP/OLP ratio dipping from 97.30% to 96.31%. These are small but meaningful signals of a market adjusting to softer pricing expectations. Distress remains negligible—only two REO sales and zero short sales—confirming that the segment’s softness is driven by normal market forces rather than financial stress.

Property characteristics remained stable. Square footage declined slightly (–1.76%), lot size held steady, and PPSF (based on total square footage) fell modestly (–3.56%). HOA dues increased, but only modestly (median +8.12%), far below the condominium segment’s 14% median jump. This stability reinforces that the segment’s year‑over‑year changes are driven primarily by pricing and interest‑rate dynamics rather than shifts in the underlying housing stock.

All six counties recorded attached‑home sales, though several had only a handful of closings. These counties will receive factual micro‑summaries later in the post, but the regional trends are overwhelmingly shaped by Multnomah, Washington, and Clackamas counties—with Washington County exerting the strongest influence due to its sheer volume.

Overall, Q1 2026 delivered a more affordable, more active, and slightly softer attached‑home market—one that responded predictably to improved rates and regional economic conditions. The segment’s role as the metro’s safety-net housing option is fully on display in this dataset.

Portland Region Scatter Plots

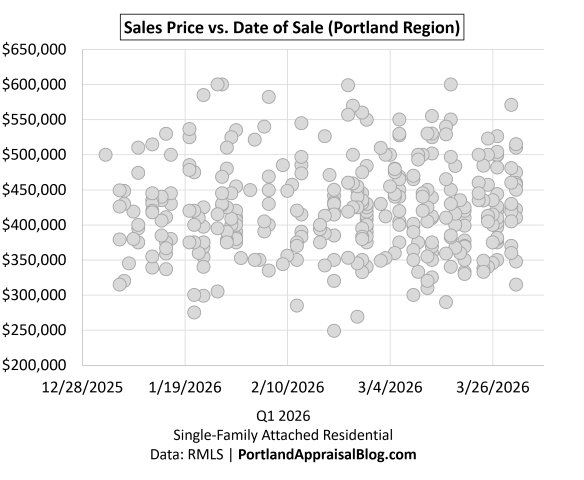

To visualize the distribution of individual attached homes sales prices across Q1 2026, the following scatter plots show sales price against date of sale:

The full‑quarter scatter plot provides a clear visual of how attached‑home prices distributed across Q1 2026. Even with normal day‑to‑day variation, the segment shows a remarkably tight mid‑market band: more than 70% of all attached sales closed between $350,000 and $499,999, and over 31% clustered specifically in the $400,000–$449,999 range. This concentration is exactly what the spread‑ratio metrics signal—attached homes are the metro’s most uniform, commodity‑like segment, with predictable layouts, consistent utility, and limited variation in size.

The scatter also shows a modest number of lower‑priced sales, but they are rare. Only eight sales closed below $300,000, and just one sale fell below $250,000. This scarcity reinforces the segment’s role in the ecosystem: attached homes are more affordable than detached, but they are not an entry‑level segment in the same way condos can be. Buyers seeking sub‑$300,000 opportunities generally must look to condominiums or manufactured homes.

At the upper end, the scatter includes a small number of premium attached homes, with roughly a dozen sales above $700,000 and three sales at or above $950,000. These outliers demonstrate that the segment can support higher‑end product in select neighborhoods, but they are too infrequent to influence regional averages or affordability metrics.

Activity is evenly distributed across the quarter, with no visible surges or drop‑offs. This aligns with the sales‑count data: closings increased year‑over‑year, driven by improved affordability and a notable rise in new‑construction deliveries. The scatter shows no abrupt price spikes or collapses—just a steady, slightly softer price environment consistent with the five‑percent decline in average and median values.

Overall, the full scatter plot reinforces the defining characteristics of the attached‑home segment: stable demand, tight pricing distribution, and a mid‑market profile that anchors the region’s affordability landscape.

Zooming in on sales priced at $600,000 or less, we have:

The zoomed‑in scatter plot sharpens what the full‑scale view already suggested: attached‑home prices in Q1 2026 were tightly concentrated in the mid‑market band. With the vertical axis capped at $650,000, the plot highlights the segment’s core range—roughly $300,000 to $550,000—where nearly 80% of all sales occurred. The clustering is dense, consistent, and evenly distributed across the quarter, reinforcing the segment’s commodity‑like profile and the stability of demand throughout Q1.

The zoomed view also makes the lower‑priced portion of the market easier to see. Only a handful of sales fell below $300,000, and just one dipped below $250,000. This scarcity underscores that attached homes are not the region’s entry‑level segment; buyers seeking sub‑$300,000 opportunities overwhelmingly turn to condos or manufactured homes instead.

At the upper end, the zoomed plot shows a small number of sales pushing into the $600,000–$650,000 range. These are the same premium outliers visible in the full scatter, but the zoomed view makes clear how infrequent they are relative to the segment’s core. They represent neighborhood‑specific product rather than a broader trend.

Overall, the zoomed‑in scatter confirms the defining characteristics of the attached‑home segment: a tight, predictable price distribution; steady activity across the quarter; and a mid‑market profile that aligns with the segment’s role as the region’s primary affordability bridge between condos and detached homes.

Sales Volume

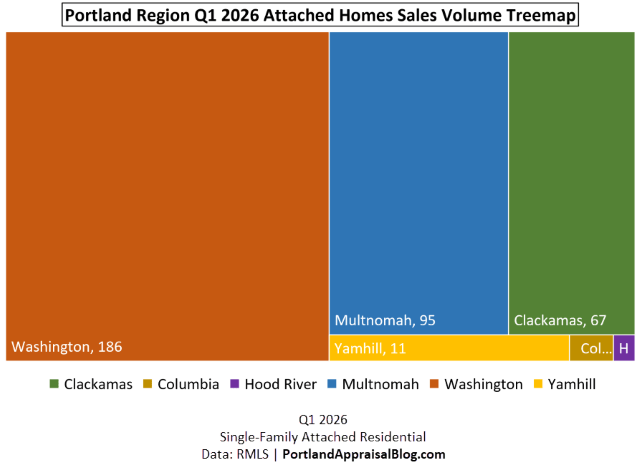

A treemap visualizing the distribution of attached homes sales by county in Q1 2026 clearly illustrates the market’s geographic concentration.

The treemap makes the geographic structure of the attached‑home market immediately clear: activity in Q1 2026 was overwhelmingly concentrated in the Big Three counties, with Washington County dominating the segment. More than half of all attached‑home closings occurred in Washington County alone, reflecting both its larger suburban housing base and its multi‑year preference for attached homes over condominiums. Multnomah and Clackamas counties round out the core, together contributing another 44% of all sales. In total, 96.13% of the region’s attached‑home activity came from the Big Three, underscoring how tightly the segment is anchored to the metro’s primary population and employment centers.

The remaining counties—Yamhill, Columbia, and Hood River—recorded only modest activity, with a combined 14 sales. These counties routinely produce small attached‑home counts due to their housing stock composition, development patterns, and buyer preferences. Their limited volume does not materially influence regional averages, but their participation confirms that attached homes are present, albeit sparsely, across the full six‑county region.

Washington County’s outsized share is especially important for interpreting regional trends. Because it accounts for 51.38% of all attached closings, its pricing, affordability, and new‑construction dynamics exert the strongest pull on the regional metrics discussed earlier. The treemap visually reinforces this influence: Washington County is not just the largest block—it is the structural center of the attached‑home market in Q1 2026.

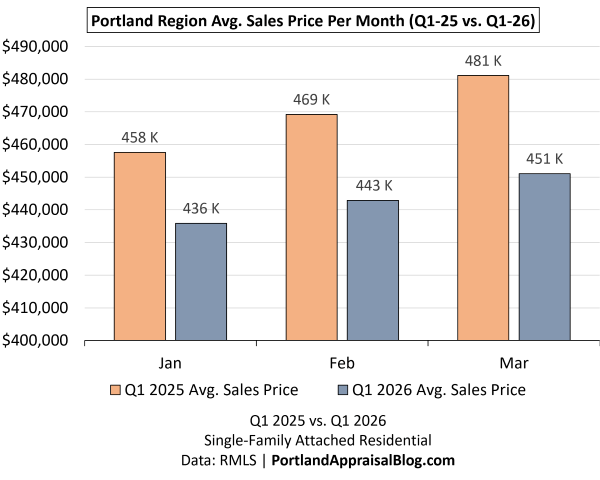

The bar chart below compares monthly sales volume across the three months of Q1 for 2025 and Q1 2026.

The month‑by‑month comparison highlights how attached‑home activity evolved across the quarter and why total sales ultimately finished higher than in Q1 2025. The pattern is uneven but intuitive: softer pricing and improved affordability brought more buyers back into the market, but the timing of that return varied by month.

January posted a modest increase, rising from 89 to 99 sales (+10). This aligns with the early‑quarter improvement in rates and the segment’s overall affordability shift. February, however, moved in the opposite direction, declining from 127 to 99 sales (–28).

March delivered the decisive shift. Sales jumped from 112 to 164 (+52), the strongest monthly gain of the quarter and the clearest signal of renewed buyer engagement. This surge is consistent with the broader Q1 narrative: affordability improved sharply, new‑construction closings increased, and the region’s core counties saw more buyers re‑enter the market.

While Washington County held nearly steady year‑over‑year, the overall increase in regional sales volume was driven by higher activity in Multnomah County, along with additional gains in Clackamas and Yamhill counties. These counties collectively tipped the scales, pushing the quarter to a 10.37% increase in total attached‑home sales.

Taken together, the monthly pattern shows a market responding predictably to improved conditions. Buyers returned gradually, then decisively, producing a strong finish to the quarter.

Sales Price

The bar chart below compares monthly average sales prices across the three months of Q1 for 2025 and Q1 2026.

Average sales prices declined across all three months of Q1 2026, and the pattern is both consistent and meaningful. January fell 4.75% year‑over‑year, February declined 5.60%, and March posted the steepest drop at 6.24%. While the magnitudes differ slightly, the direction is uniform: attached‑home prices were lower every month of the quarter compared to Q1 2025.

For buyers, this softening provided a genuine silver lining. Lower prices, paired with improved interest rates, helped push affordability sharply higher—one of the defining stories of the quarter. The attached segment flipped from strained to moderately affordable, and the monthly price declines played a direct role in that shift.

The softness was broad‑based. Every county except Hood River saw both average and median prices decline year‑over‑year. Hood River recorded only one attached sale, so its stability is not meaningful in a trend sense. The regional pattern reflects a tougher quarter for attached homes overall, and given that Washington County accounts for more than half of all attached closings, its slight year‑over‑year decline carries outsized influence. The ongoing Intel layoffs likely contributed to this pressure, adding a layer of economic uncertainty that nudged pricing expectations downward.

Even so, the segment remained active. Buyers responded predictably to improved affordability, and increased sales in Multnomah, Clackamas, and Yamhill counties helped offset Washington County’s slight decline. The result is a quarter where prices softened, affordability improved, and demand strengthened—an unusual but coherent combination that reflects the attached homes market’s multi-year trend of softening prices.

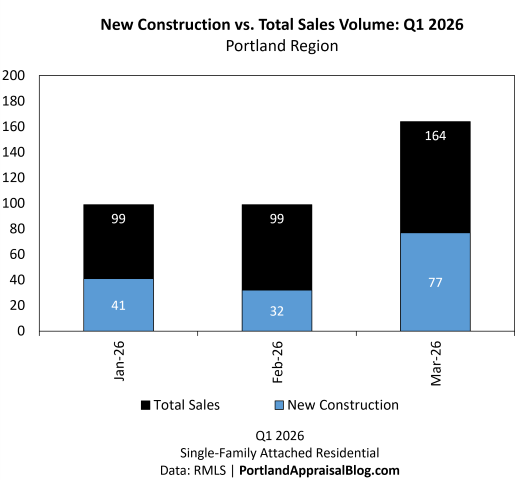

New Construction

The bar graph below shows monthly total attached homes sales in Q1 2026, with new construction volume nested within each bar to illustrate the portion of sales that were newly built.

The nested bar chart makes one point immediately clear: new construction is a defining feature of the attached‑home segment. Across Q1 2026, newly built homes accounted for 41.44% of all attached‑home closings, an unusually high share for any residential segment and fully consistent with attached homes having the lowest average age of the four major single-family housing categories.

The monthly pattern is also instructive. January and February delivered solid new‑construction activity, with 41 and 32 closings respectively—roughly one‑third to two‑fifths of all sales in each month. Then March surged. New‑construction closings jumped to 77, representing nearly 47% of all attached‑home sales that month.

Regionally, these figures underscore how central new construction is to the attached‑home ecosystem. The segment relies heavily on newly built supply to meet demand, and builders continue to deliver a substantial share of the product buyers ultimately purchase.

The bar graph below shows new construction sales broken out by county for Q1 2025 and Q1 2026.

The county‑level breakout highlights how unevenly new‑construction activity is distributed across the region and why the attached‑home segment continues to have the lowest average age of the four major housing categories.

Clackamas posted a modest gain, rising from 16 to 18 new‑construction closings (+12.50%). Washington County held essentially steady, dipping slightly from 91 to 90 (–1.10%). Multnomah, however, delivered the standout performance: new‑construction closings jumped from 24 to 40 (+66.67%), making it the fastest‑growing county in Q1 2026 for newly built attached homes. Yamhill added two new‑construction sales after recording none the prior year, while Columbia and Hood River remained at zero.

Even with Multnomah’s impressive growth, Washington County remains the structural center of new construction in the attached‑home segment. Its 90 closings represent 60% of all new‑construction activity—more than the remaining counties combined. This dominance is consistent with Washington County’s multi‑year pattern: it continues to favor new attached homes over new condos, and builders remain highly active in its suburban submarkets.

Regionally, the story is straightforward: new construction is not a supplemental source of inventory—it is a core driver of the attached‑home market. Q1 2026 reaffirmed that role with strong winter performance and a March surge, supported by notable gains in Multnomah and steady output from Washington County.

The table below shows new construction sales volume by dollar amount for Q1 2026 compared with Q1 2025.

| County | Q1 2025 $ Amount | Q1 2026 $ Amount | % Change |

|---|---|---|---|

| Clackamas | $10,129,115 | $8,256,272 | -18.49% |

| Columbia | $0 | $0 | — |

| Hood River | $0 | $0 | — |

| Multnomah | $9,839,365 | $16,203,947 | 64.68% |

| Washington | $43,283,100 | $40,248,175 | -7.01% |

| Yamhill | $0 | $859,800 | — |

| Sum | $63,251,580 | $65,568,194 | 3.66% |

Data: RMLS | PortlandAppraisalBlog.com

The following double bar chart provides the above information at a glance.

New‑construction dollar volume rose modestly at the regional level in Q1 2026, increasing 3.66% year‑over‑year. But beneath that headline, the counties moved in very different directions—and understanding those differences is essential to interpreting the segment accurately.

Clackamas is the clearest example of a compositional reset rather than a pricing decline. Even though new‑construction sales increased from 16 to 18, total dollar volume fell sharply. The reason is straightforward: Q1 2025 included two exceptionally high‑end attached homes in Lake Oswego, each selling for more than $1.7M. Nothing in Q1 2026 exceeded the mid‑$500Ks. With those two luxury sales gone, the average price dropped significantly, but the median moved only modestly, reflecting a shift toward smaller, more affordable homes rather than a collapse in values.

Multnomah’s story is much simpler. New‑construction closings jumped from 24 to 40, and dollar volume rose accordingly. This is a clean volume‑driven increase, consistent with the county’s broader surge in attached‑home activity and its growing share of the region’s new‑construction market.

Washington County presents the opposite dynamic: sales were essentially unchanged, yet dollar volume declined. This signals genuine price softening, not a change in product mix. Builders conceded more on original list prices, average and median prices fell, price‑per‑square‑foot declined, and market times lengthened. Given Washington County’s outsized role in the attached‑home segment—and the economic backdrop created by the Intel layoffs—this softening resulted in builders netting roughly $3M fewer dollars year‑over‑year.

Taken together, these county‑level dynamics explain why regional dollar volume still managed a modest increase. Multnomah’s growth offset Washington County’s softening, and Clackamas’s compositional reset simply returned the county to its typical mid‑market profile. The result is a quarter where new construction remained a central driver of the attached‑home ecosystem, even as pricing pressures and product shifts varied sharply by county.

The following map shows the distribution of new construction sales.

The map of new‑construction closings reinforces a pattern that has been consistent for years: attached‑home new construction is overwhelmingly an urban and suburban phenomenon. The clusters concentrate along the westside and southside growth corridors—places like Hillsboro, Beaverton, Tigard, Sherwood, and Happy Valley—with smaller pockets extending into Gresham and the inner eastside.

What stands out is how tightly new construction hugs existing infrastructure, employment centers, and established development patterns. These aren’t rural builds or fringe‑market experiments; they’re infill projects, master‑planned communities, and suburban expansions in areas already primed for attached‑home demand. The distribution mirrors the segment’s identity: younger housing stock, smaller lots, and builder activity concentrated where land availability and zoning make attached homes feasible.

This spatial pattern also aligns with the county‑level dynamics discussed earlier. Washington County’s dominance is visible in the dense westside clusters, Multnomah’s growth shows up in the eastside and inner‑Portland pockets, and Clackamas’s contributions appear in the Happy Valley corridor.

Cumulative Days on Market

The bar chart below compares average cumulative days on market (CDOM) across the three months of Q1 for 2025 and Q1 2026.

The bar chart comparing average cumulative days on market across Q1 shows a clear and consistent pattern: the first two months of 2026 moved faster than the prior year, and those gains more than offset the slight lengthening in March.

January improved from 84 to 77 days (–8.32%), and February followed the same trajectory, dropping from 92 to 85 days (–7.62%). These early‑quarter improvements reflect stronger buyer engagement and quicker decision cycles at a time when mortgage rates were trending downward—moving from 6.16% to 5.98%. While rates aren’t the only factor influencing market tempo, this alignment likely contributed to the faster absorption we observed in January–February.

March, by contrast, saw average CDOM rise from 74 to 80 days (+7.21%). This coincided with a noticeable rate reversal, with mortgage rates climbing up 6.38% by month‑end. That shift likely introduced a bit of buyer hesitation and modestly slowed absorption. The increase wasn’t large enough to erase the momentum established earlier in the quarter, but it did slow the segment down.

Taken together, Q1 2026 still moved faster overall. The segment benefited from quicker early‑quarter absorption, and the modest recalibration in March reflects a market responding to short‑term rate movement rather than signaling a broader slowdown.

HOA Dues

While not all attached homes are located in an HOA with mandatory dues, they are a defining feature of the attached homes residential market:

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| # of HOA Sales | 260 | 279 | +19 homes |

| Total Sales | 328 | 362 | +34 homes |

| % of Market | 79.27% | 77.07% | -2.77 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

The Q1 data shows just how central HOA‑based living is to the attached‑home segment. Out of 362 sales in Q1 2026, 279 reported nonzero HOA dues, meaning more than three‑quarters of all attached‑home closings occurred within dues‑bearing communities.

The increase in HOA‑dues sales—from 260 to 279—reinforces the stability of this pattern. Attached homes continue to be built, marketed, and purchased within communities where shared maintenance, common‑area amenities, and community standards shape both monthly payment profiles and long‑term ownership costs. HOA dues remain a defining financial component of the segment, influencing affordability calculations and distinguishing attached homes from their detached counterparts, which have much lower dues—averaging about $70 per month in the Big Three counties—and only 26% of sales occurring within HOAs.

In short, the attached‑home market continues to operate as a dues‑anchored ecosystem—HOA communities aren’t the exception; they’re the norm.

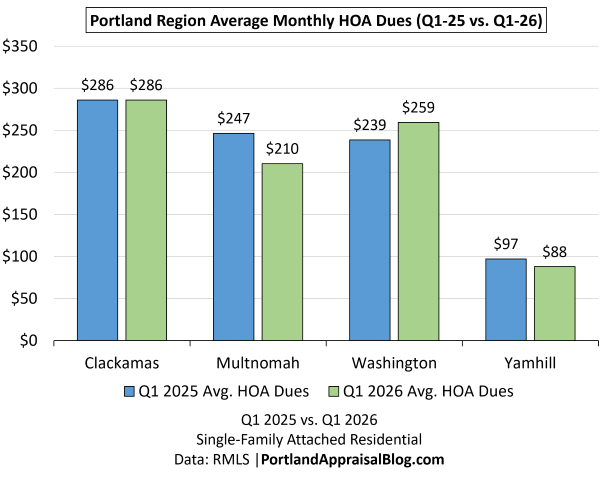

The bar chart below compares average monthly HOA dues (for reporting sales) for Q1 2025 and Q1 2026 broken out by county:

The county‑level comparison of average monthly HOA dues shows a mix of modest declines, one notable increase, and two counties that are omitted from the bar chart due to little or no attached‑home HOA activity in the period. Columbia had only a single dues‑bearing sale in Q1 2025 and none in Q1 2026, while Hood River’s dues figures are based on extremely limited sales and therefore aren’t included in the visual.

Clackamas, Multnomah, and Yamhill all posted year‑over‑year declines, while Washington County saw an increase from $238.66 to $259.44 (+8.71%). These shifts are meaningful, but interpretation requires attention to reporting behavior—especially in counties with active new‑construction pipelines.

Multnomah’s decline from $246.69 to $210.49 (–14.68%) should be read cautiously. The county saw a strong boost in new‑construction sales in Q1 2026, and it’s common for new‑construction listings to report zero HOA dues in MLS when dues haven’t been finalized at the time of listing. This can temporarily depress the average even when underlying dues are stable. Washington County, by contrast, had steady new‑construction activity year‑over‑year, making its increase more reliable and less affected by non‑reporting.

Yamhill’s decline is modest and should also be interpreted cautiously due to a small number of sales. Clackamas remains stable, with only a slight decrease.

Taken together, the county‑level data reinforces a familiar pattern: HOA dues vary across the region, but accurate interpretation requires accounting for reporting dynamics—especially in markets with active new construction.

Miscellaneous Statistics & Standout Transactions

Here are some of the most notable outliers and extremes from the 2026 Portland Region attached homes residential market—numbers that illustrate the full range of the data and the extremes buyers and appraisers encounter.

Lowest Sales Price: $249,000—This home is located in Wilkes Portland neighborhood. The unit is 1,114 sq. ft. and has two bedrooms and two bathrooms. Photos of this property are currently available online.

Highest Sales Price: $1,175,000—This home is located in Hood River, Oregon. The unit is 1,819 sq. ft. and has three bedrooms and three bathrooms. This property also has the highest price per square foot for the quarter ($645.95). Photos of this property are currently available online.

Lowest Price Per Square Foot: $158.13—This home is located in Lake Oswego, Oregon. The unit is 1,992 sq. ft., has three bedrooms and 2.1 bathrooms; it closed for $315,000. Photos of this property are currently available online.

Longest CDOM: 501 days—This home is located in the Northwest Heights Portland neighborhood. The unit is 1,431 sq. ft. and has two bedrooms and two bathrooms. Initially listed September 2024 for $450,000, it finally closed for $350,000 in late-February 2026. Photos of this property are currently available online.

Smallest Attached Home: 794 sq. ft.—This attached home is located in Newberg, Oregon. The one-bedroom, one-bathroom home is located in the 55+ community of Crestview Manor. Photos of this property are currently available online.

Largest Attached Home: 3,284 sq. ft.—The largest townhome of the quarter is located in West Linn, Oregon. The home has four bedrooms and 3.1 bathrooms. The unit closed for $897,500. Photos of this property are currently available online.

Highest Monthly HOA Dues: $793.00—This home is located in Lake Oswego, Oregon. The unit closed for $455,000 and is 1,314 sq. ft and has two bedrooms and two bathrooms. The HOA dues include a community pool, recreation facility as well as coverage of water, sewer, and exterior maintenance. Photos of this property are currently available online.

With the regional aggregate trends, graphs, monthly patterns, and notable outliers covered, the remainder of this update turns to a county-level breakdown. The following sections present year-over-year comparisons for each of the six counties in the Portland Region—Multnomah, Washington, Clackamas, Yamhill, Columbia, and Hood River. Each county snapshot includes key metrics, commentary on local drivers, and any segment-specific observations that help explain broader regional patterns.

Multnomah County Q1 2026 Stats

The table below summarizes key metrics for Multnomah County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $28,855,250 | $40,935,465 | +41.86% |

| Average Price | $450,863 | $430,900 | -4.43% |

| Median Price | $410,000 | $395,000 | -3.66% |

| Avg SP/OLP | 96.50% | 97.17% | +0.70% |

| Avg PPSF (TSF) | $319.62 | $294.07 | -8.00% |

| Avg HOA Dues | $246.69 | $210.49 | -14.68% |

| Median HOA Dues | $187.00 | $178.00 | -4.81% |

| Avg Lot Size (ac) | 0.0566 | 0.0602 | +6.41% |

| Avg Age (Yrs) | 14.50 | 13.84 | -4.54% |

| Avg CDOM | 92.83 | 73.34 | -21.00% |

| Avg Total SF | 1,467 | 1,513 | +3.12% |

| Total # of Sales | 64 | 95 | +48.44% |

| # of New Constr. | 24 | 40 | +66.67% |

| # of REOs | 0 | 2 | — |

| # of Short Sales | 0 | 0 | — |

| Average PABAI | 93.48 | 112.87 | +19.39 pts |

| # Affordable | 29 | 71 | +42 homes |

| % Affordable | 45.31% | 74.74% | +29.42 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Multnomah County delivered a high‑volume quarter shaped overwhelmingly by new‑construction activity. Total dollar volume rose 41.86%, nearly proportional to the 48.44% increase in closed sales, confirming that the quarter’s strength came from more units selling, not higher prices.

Prices moved lower year‑over‑year despite slightly larger homes on slightly larger lots. Average price fell 4.43%, median price declined 3.66%, and average PPSF dropped 8.00%. This pattern reflects a clear compositional shift: new‑construction units averaged 1,350 square feet, compared with 1,631 square feet for resale units. Smaller homes enter the market at lower total prices even when their PPSF is strong, and Multnomah’s 40 new‑construction closings (up from 24) pulled the county’s pricing metrics downward.

Market tempo improved sharply. Average cumulative days on market fell from 92.83 to 73.34—a nearly 20‑day reduction. Builders tend to price new units to move, and the county’s elevated new‑construction share helped accelerate absorption. Sellers also gained a bit of ground relative to their initial list prices, with SP/OLP rising to 97.17%, indicating realistic initial pricing and responsive buyer demand.

HOA dues declined on both an average and median basis, but this drop is almost certainly illusory. New‑construction listings frequently report zero dues when HOA budgets are not finalized at the time of listing, and Multnomah’s surge in brand‑new inventory makes this reporting dynamic the most likely explanation for the decline.

Affordability expanded dramatically. The county’s PABAI rose to 112.87, and 74.74% of all sales qualified as affordable—nearly three‑quarters of the market. This reflects both the influence of smaller, lower‑priced new‑construction units and the rate environment that supported stronger buyer access during the quarter. Builders are striving to meet the market where effective demand exists, and the Q1 delivery mix shows they were targeting price points buyers could actually reach.

Overall, Multnomah County’s Q1 2026 performance was defined by a large influx of smaller new‑construction homes, reshaping pricing, dues, affordability, and market tempo. The result was a fast‑moving, highly accessible quarter with strong buyer engagement and realistic seller pricing.

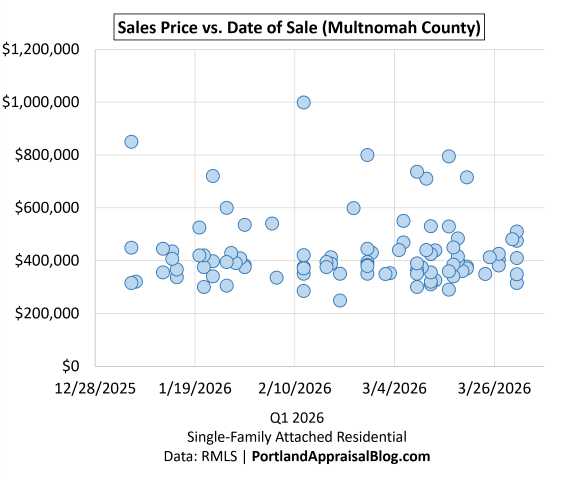

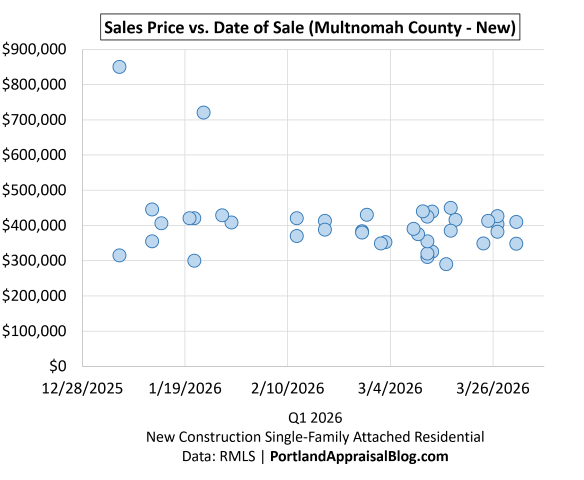

The following is a scatter plot of all Multnomah County attached homes sales in Q1 2026:

The scatter plot for Q1 2026 shows a market that is tightly concentrated in a very narrow price band. 76.84% of all Multnomah attached‑home sales closed between $300,000 and $500,000, which is an unusually compressed range compared with the detached‑home market. There is very little activity below $300,000 and only a small number of sales above $600,000, reinforcing just how centered this segment is around the mid‑market tiers.

The distribution is especially dense in the $350,000–$399,000 and $400,000–$449,000 brackets, which together account for more than half of all sales. The scatter reflects this visually: most points cluster in a tight vertical band, with only a few outliers pushing toward the upper end of the market.

The plot also shows a noticeable flurry of closings in the final stretch of March. At first glance, this might look like a demand‑side surge, but rates were climbing during that period—not the kind of environment that typically produces a sudden buyer rush. The timing instead reflects new‑construction deliveries closing out at quarter‑end, which becomes clear when isolating just the new‑construction sales.

When viewed alongside the main scatter, the new‑construction plot makes the pattern unmistakable: the late‑March cluster is a supply‑timed closing wave, not a rate‑driven spike in demand. Builders brought units online and pushed to finish the quarter strong, and those closings landed in a tight sequence at the end of March.

Together, the two scatters confirm a mid‑tier‑dominated market with minimal lower‑end activity, a thin upper tail, and a late‑quarter wave of new‑construction closings that helped lift overall volume.

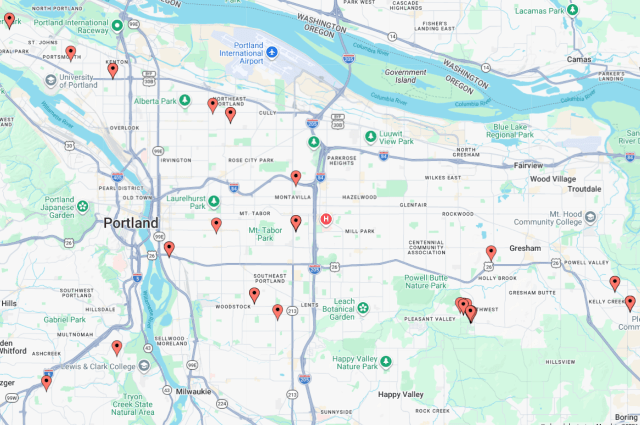

The following map shows the distribution of new construction sales during Q1 2026:

The map of new‑construction sales shows a clear eastside concentration, and that pattern reflects the underlying development realities of Multnomah County. The eastside offers more flexible land availability, more accommodating zoning, and gentler topography, all of which support attached‑home projects at mid‑market price points. Builders can deliver units efficiently and at scale, and the result is the tight $300,000–$450,000 band seen in the new‑construction scatter.

The westside, by contrast, presents a very different development environment. Large portions of the westside are shaped by steep topography, constrained parcels, and higher‑priced neighborhoods where land costs and existing built form make attached‑home development less feasible. The economics simply don’t align with the mid‑tier price points where effective demand is strongest. As a result, new‑construction attached homes are far less common west of the Willamette, and the map reflects that imbalance clearly.

Together, the map and scatter plots show that new construction shaped not only the pricing and timing of Q1 2026, but also its spatial footprint—concentrated east of the river, aligned with the corridors where attached‑home development is most viable.

Washington County Q1 2026 Stats

The table below summarizes key metrics for Washington County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $86,314,512 | $80,863,943 | -6.31% |

| Average Price | $459,120 | $434,752 | -5.31% |

| Median Price | $444,177 | $425,000 | -4.32% |

| Avg SP/OLP | 97.55% | 95.70% | -1.89% |

| Avg PPSF (TSF) | $289.69 | $277.49 | -4.21% |

| Avg HOA Dues | $238.66 | $259.44 | +8.71% |

| Median HOA Dues | $232.00 | $248.00 | +6.90% |

| Avg Lot Size (ac) | 0.0588 | 0.0623 | +6.03% |

| Avg Age (Yrs) | 13.84 | 13.98 | +1.04% |

| Avg CDOM | 76.13 | 86.90 | +14.15% |

| Avg Total SF | 1,609 | 1,588 | -1.35% |

| Total # of Sales | 188 | 186 | -1.06% |

| # of New Constr. | 91 | 90 | -1.10% |

| # of REOs | 0 | 0 | — |

| # of Short Sales | 0 | 0 | — |

| Average PABAI | 88.23 | 102.54 | +14.32 pts |

| # Affordable | 25 | 105 | +80 homes |

| % Affordable | 13.30% | 56.45% | +43.15 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Washington County’s attached‑home market softened in Q1 2026, and the declines are genuine. With total sales down by only two homes and new‑construction volume essentially unchanged (91 → 90), the year‑over‑year comparison reflects real demand‑side cooling rather than a shift in unit mix. Average price, median price, SP/OLP, and PPSF all moved lower, while CDOM rose by about ten days—a pattern consistent with buyers becoming more cautious. The ongoing fallout from the Intel layoffs likely contributed to this softer environment, especially in the resale segment.

Despite only two fewer sales, sellers took in $5.45 million less this quarter compared to last year. That’s a meaningful drop in total dollar volume, and it underscores how broad the softening was: lower prices, lower PPSF, and slightly weaker negotiation outcomes all combined to pull revenue down.

Affordability, however, surged. More than half the market (56.45%) qualified as affordable under the PABAI framework, up from just 13.30% a year earlier. PABAI jumped by 14.32 points, reflecting how rate movements and softer pricing intersected to dramatically expand buyer qualification. And because new‑construction volume was nearly identical year over year, the usual issue of under‑reported HOA dues is effectively a wash—meaning the affordability trend is directionally reliable for Washington County, even though new‑construction dues remain understated in RMLS.

A side‑by‑side look at new construction versus resale in Q1 2026 shows a market that is almost perfectly split by both dollar volume and number of sales. New homes delivered slightly more square footage and larger lots, but the median price difference between new ($449,945) and resale ($410,500) was only about $40,000, indicating that Washington County does not impose a large premium for new attached homes.

Overall, Washington County’s attached‑home segment in Q1 2026 reflects a stable mix, softer demand, expanded affordability, and a nearly even split between new and resale activity. The declines are real, the affordability gains are meaningful, and the market’s performance is best understood as a demand‑side cooling rather than a structural or compositional shift.

The following is a scatter plot of all Washington County sales in Q1 2026:

The scatter plot shows a market operating within an exceptionally tight price band. Nearly the entire quarter’s activity falls between $300,000 and $500,000, and more than half the market (54.84%) is concentrated in the $350,000–$449,999 range. This mid‑tier clustering is the defining feature of Washington County’s attached‑home segment in Q1 2026, and the scatter makes it visually unmistakable: a dense horizontal band with very few outliers above $550,000 and almost nothing below $300,000.

There is a modest uptick in closings during March, reflecting two overlapping dynamics. First, Washington County saw a slight increase in new‑construction closings toward the end of the quarter, which naturally produces a small late‑March cluster. Second, the attached‑home market typically warms as spring approaches, and the scatter shows that familiar seasonal lift. Even so, the March activity remains firmly within the same mid‑tier band, reinforcing how stable and price‑disciplined the segment was throughout Q1.

Overall, the scatter confirms a highly concentrated mid‑market, minimal lower‑end activity, and only a thin upper tail. Washington County’s attached‑home market in Q1 2026 operated within one of the narrowest price distributions in the region, and the scatter plot visually mirrors the softness and affordability expansion seen in the county‑level metrics.

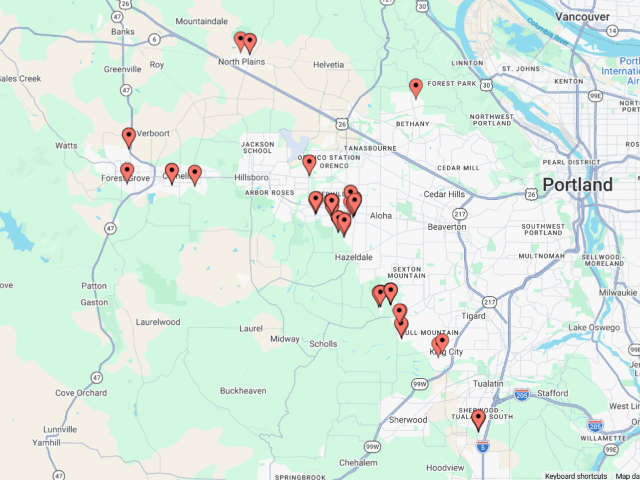

The following map shows the distribution of new construction sales during Q1 2026:

The new‑construction map for Washington County shows a development pattern that’s almost textbook for the westside: clusters of new attached‑home activity sitting right at the edges of cities, aligned with the urban growth boundary (UGB). The visual cue is unmistakable—the red markers concentrate precisely where the map transitions from urban coloration into green, signaling rural reserve, agricultural land, or forested areas. That boundary line is where Washington County’s attached‑home development has historically been most viable, and Q1 2026 continues that pattern.

Most of the new‑construction activity appears around Hillsboro, Aloha, Cornelius, and Forest Grove, with additional pockets near Bethany and South Beaverton. These are areas where land is still assemblable, topography is gentle, and zoning supports higher‑density formats. Builders gravitate to these UGB‑adjacent zones because they offer the combination of flat terrain, infrastructure access, and development‑friendly entitlements needed to deliver attached homes at mid‑tier price points.

What’s equally notable is where new construction isn’t happening. The interior of established neighborhoods—Cedar Hills, Sexton Mountain, Bull Mountain, central Beaverton—shows very few markers. These areas have higher land costs, fragmented parcels, and steeper topography in places, all of which make attached‑home development more difficult. The map’s pattern reflects that reality: new construction hugs the green edges rather than filling in the urban core.

Clackamas County Q1 2026 Stats

The table below summarizes key metrics for Clackamas County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $32,731,115 | $33,201,588 | +1.44% |

| Average Price | $536,576 | $495,546 | -7.65% |

| Median Price | $467,500 | $440,000 | -5.88% |

| Avg SP/OLP | 97.43% | 96.35% | -1.11% |

| Avg PPSF (TSF) | $299.00 | $294.75 | -1.42% |

| Avg HOA Dues | $286.20 | $286.19 | -0.00% |

| Median HOA Dues | $225.50 | $243.00 | +7.76% |

| Avg Lot Size (ac) | 0.07 | 0.08 | +6.16% |

| Avg Age (Yrs) | 14.56 | 17.91 | +23.03% |

| Avg CDOM | 106.95 | 76.82 | -28.17% |

| Avg Total SF | 1,762 | 1,692 | -3.98% |

| Total # of Sales | 61 | 67 | +9.84% |

| # of New Constr. | 16 | 18 | +12.50% |

| # of REOs | 0 | 0 | — |

| # of Short Sales | 0 | 0 | — |

| Average PABAI | 80.42 | 92.29 | +11.88 pts |

| # Affordable | 6 | 33 | +27 homes |

| % Affordable | 9.84% | 49.25% | +39.42 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Clackamas County posted a mixed performance in Q1 2026, with rising sales activity but clear price erosion. Total sales increased nearly 10% year over year (61 → 67), yet total dollar volume rose only 1.44%, meaning sellers collectively earned just $470,473 more than last year. That gap between unit growth and revenue growth is the clearest sign of softening prices: average price fell 7.65%, median price declined 5.88%, and PPSF slipped modestly. Some of this decline reflects a shift toward smaller units—average total square footage dropped by nearly 4%—but the price reductions exceed what size alone would explain, indicating genuine market cooling.

Affordability expanded sharply, rising from 9.84% to 49.25%, yet Clackamas still remains the least affordable of the three major counties. Larger average square footage, higher HOA dues, and an older attached‑home stock all contribute to this structural reality. The average age of sold units jumped from 14.6 to 17.9 years, reinforcing that Clackamas has fewer new attached‑home projects and a more mature inventory profile compared with Multnomah and Washington counties.

One of the more notable improvements was in market efficiency: CDOM fell dramatically, dropping from 107 days to 77 days. Even with lower prices, homes sold significantly faster, suggesting sellers adjusted expectations and buyers responded to more realistic pricing. This is consistent with a market that is softening but still liquid.

A closer look at new construction versus resale in Q1 2026 shows that builders and resale sellers operated in distinctly different segments. New construction accounted for 18 sales, while resale represented 49, and the two cohorts diverged sharply in size. New homes averaged 1,572 sq. ft., compared with 1,736 sq. ft. for resale—a 164 sq. ft. difference that explains most of the pricing gap. Builders are clearly delivering smaller new units to keep average prices down—1,920 sq. ft. in Q1 2025 to 1,572 sq. ft. in Q1 2026—and when adjusting for square footage, the new‑construction premium essentially disappears. PPSF is nearly identical between the two groups, and a back‑of‑the‑envelope calculation shows that equal‑sized units would have nearly the same implied value.

Overall, Clackamas County’s attached‑home market in Q1 2026 reflects higher sales activity, lower prices, faster absorption, and a meaningful shift toward smaller new‑construction units. The county remains the least affordable of the Big Three, but the quarter shows a market adjusting efficiently to softer demand and delivering product that aligns with buyer qualification thresholds.

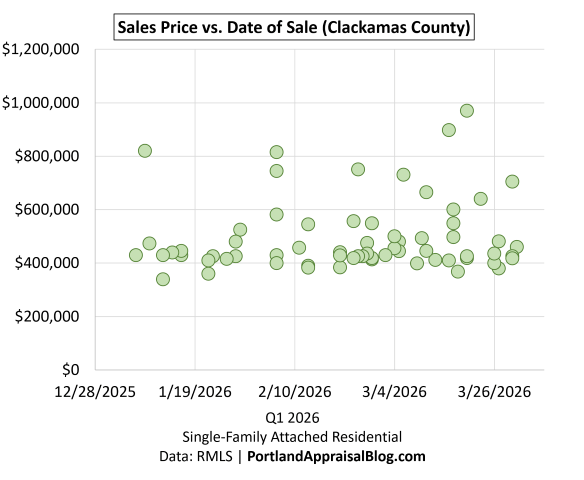

The following is a scatter plot of all Clackamas County sales in Q1 2026:

The scatter plot for Clackamas County shows a price distribution that is both tightly concentrated in the mid‑market and meaningfully stretched into the upper tiers, a pattern that distinguishes the county from both Multnomah and Washington. The densest portion of the quarter’s activity sits between $400,000 and $449,999, and when combined with the adjacent $450,000–$499,999 tier, these two ranges account for nearly three‑quarters of all sales. This narrow mid‑market band is the defining feature of Clackamas attached‑home pricing in Q1 2026.

What’s equally notable is what the scatter doesn’t show: almost no activity below $350,000. Only one sale fell into the 300–349K range, and nothing transacted below that. This absence of lower‑priced units is a structural characteristic of Clackamas County’s attached‑home stock—larger average square footage, higher HOA dues, and older inventory all push the market upward compared with the other major counties. The scatter makes this visually obvious: the lower end is essentially missing.

Above the mid‑market band, Clackamas shows a meaningful upper tail. Several sales closed between $600,000 and $1,000,000, including one above $950,000. This upper‑tier activity is far more pronounced than in Washington County, where attached‑home pricing is tightly uniform and rarely reaches these levels. In contrast, Clackamas supports a wider range of attached‑home formats and sizes, and the scatter reflects that diversity with a broader vertical spread.

Taken together, the scatter plot illustrates why Clackamas remains the least affordable of the Big Three counties. While all three counties struggle to produce units under $300,000, Multnomah’s densest band sits lower (350–399K), and Washington has substantial activity in the 300–399K range. Clackamas, by contrast, clusters higher and shows more upper‑tier sales, reinforcing the county’s structurally elevated pricing profile.

The following map shows the distribution of new construction sales during Q1 2026:

The new‑construction map for Clackamas County shows a pattern that’s immediately recognizable once you’ve looked at Multnomah and Washington: activity generally clusters right at or just inside the edges of major cities, where zoning, infrastructure, and parcel configuration make attached‑home development feasible. Every red marker sits in or near an incorporated area—Happy Valley, Milwaukie, Oregon City—and even the outlier in Molalla is still within the city’s built‑up footprint rather than in rural reserve or agricultural land. This is the same development logic we saw in Washington County, but expressed through Clackamas’ geography.

Yamhill County Q1 2026 Stats

The table below summarizes key metrics for Yamhill County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $1,996,000 | $4,026,200 | +101.71% |

| Average Price | $399,200 | $366,018 | -8.31% |

| Median Price | $400,000 | $377,900 | -5.53% |

| Avg SP/OLP | 100.22% | 97.45% | -2.77% |

| Avg PPSF (TSF) | $323.68 | $311.36 | -3.81% |

| Avg HOA Dues | $97.17 | $87.92 | -9.52% |

| Median HOA Dues | $65.00 | $45.00 | -30.77% |

| Avg Lot Size (ac) | 0.09 | 0.09 | -1.65% |

| Avg Age (Yrs) | 25.60 | 24.91 | -2.70% |

| Avg CDOM | 23.20 | 76.91 | +231.50% |

| Avg Total SF | 1,262 | 1,201 | -4.81% |

| Total # of Sales | 5 | 11 | +120.00% |

| # of New Constr. | 0 | 2 | — |

| # of REOs | 0 | 0 | — |

| # of Short Sales | 0 | 0 | — |

| # Affordable | 3 | 11 | +8 homes |

| % Affordable | 60.00% | 100.00% | +40.00 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Yamhill County saw a sharp increase in attached‑home activity in Q1 2026, though the small sample size limits interpretation. Total sales rose from 5 to 11, a 120% increase, and total dollar volume more than doubled, netting sellers an additional $2.03M. With only a handful of transactions in each quarter, this jump reflects the addition of a few more closings rather than a structural shift in the market.

Two new‑construction units closed during the quarter, both from the same small infill project in Lafayette. This was the only new‑construction activity in the county for Q1 2026.

Overall, Yamhill County’s attached‑home market remains extremely low‑volume, and the quarter’s results reflect the sensitivity of small datasets to individual sales. The doubling of dollar volume and sales count is notable, but not indicative of a broader trend. The presence of two new units in Lafayette is the only structural change worth noting; otherwise, the quarter’s metrics should be interpreted cautiously due to limited activity.

The following is a scatter plot of all Yamhill County sales in Q1 2026:

Most activity is concentrated between $350,000 to under $450,000.

Columbia County Q1 2026 Stats

The table below summarizes key metrics for Columbia County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $2,811,205 | $769,000 | -72.65% |

| Average Price | $401,601 | $384,500 | -4.26% |

| Median Price | $405,000 | $384,500 | -5.06% |

| Avg SP/OLP | 95.55% | 98.81% | +3.41% |

| Avg PPSF (TSF) | $248.84 | $246.68 | -0.87% |

| Avg HOA Dues | $21.25 | — | — |

| Median HOA Dues | $21.25 | — | — |

| Avg Lot Size (ac) | 0.08 | 0.08 | +6.25% |

| Avg Age (Yrs) | 19.86 | 27.00 | +35.97% |

| Avg CDOM | 45.86 | 13.00 | -71.65% |

| Avg Total SF | 1,633 | 1,560 | -4.45% |

| Total # of Sales | 7 | 2 | -71.43% |

| # of New Constr. | 0 | 0 | — |

| # of REOs | 0 | 0 | — |

| # of Short Sales | 0 | 0 | — |

| # Affordable | 4 | 2 | – 2 homes |

| % Affordable | 57.14% | 100.00% | +42.86 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Columbia County had very limited attached‑home activity in Q1 2026, with only two sales recorded for the quarter. This represents a decline of five sales year‑over‑year, and total dollar volume fell accordingly—from $2.81M to $769,000, a reduction of $2.04M. With such a small dataset, these changes reflect the absence of a few transactions rather than any meaningful shift in market conditions. There were no new‑construction units this quarter.

Overall, Columbia County’s attached‑home market remains extremely low‑volume, and the quarter’s results should be interpreted cautiously. The decline in sales and dollar volume is notable, but not indicative of a structural change; it simply reflects the sensitivity of small datasets to individual transactions.

Hood River County Q1 2026 Stats

The table below summarizes key metrics for Hood River County attached homes residential sales in Q1 2026 compared with Q1 2025.

| Category | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total $ Volume | $1,485,000 | $1,175,000 | -20.88% |

| Average Price | $495,000 | $1,175,000 | +137.37% |

| Median Price | $460,000 | $1,175,000 | +155.43% |

| Avg SP/OLP | 95.85% | 106.82% | +11.44% |

| Avg PPSF (TSF) | $356.60 | $645.95 | +81.14% |

| Avg HOA Dues | $36.46 | $401.91 | +1002.48% |

| Median HOA Dues | $36.46 | $401.91 | +1002.48% |

| Avg Lot Size (ac) | 0.0533 | 0.0300 | -43.78% |

| Avg Age (Yrs) | 12.67 | 21.00 | +65.79% |

| Avg CDOM | 114.00 | 25.00 | -78.07% |

| Avg Total SF | 1,501 | 1,819 | +21.16% |

| Total # of Sales | 3 | 1 | -66.67% |

| # of New Constr. | 0 | 0 | — |

| # of REOs | 0 | 0 | — |

| # of Short Sales | 0 | 0 | — |

| # Affordable | 0 | 0 | 0 homes |

| % Affordable | 0.00% | 0.00% | 0 pts |

Single-Family Attached Residential | Q1 2025 & Q1 2026

Data: RMLS | PortlandAppraisalBlog.com

Hood River County had only one attached‑home sale in Q1 2026, down from three the year before. With such a small dataset, year‑over‑year comparisons are not meaningful. Total dollar volume declined from $1.49M to $1.18M, a net difference of $310,000. There were no new‑construction units this quarter.

Overall, Hood River County’s attached‑home market remains extremely low‑volume, and the quarter’s results should be interpreted cautiously. The decline in sales and dollar volume is notable, but not indicative of a structural change; it simply reflects the sensitivity of small datasets to individual transactions.

Closing Thoughts

Q1 2026 showed a region adjusting through lower prices, slightly improved interest rates, and builder‑driven shifts in product size, all of which combined to make attached homes more accessible to buyers. With softer pricing, overall activity increased: regional sales rose 10%, and total dollar volume edged up 4.4%, signaling steady demand as buyers responded to more attainable price points.

Affordability was the standout change. The share of affordable attached‑home sales jumped from 20% to 61%, adding 155 more affordable units compared with last year. This improvement was driven primarily by lower prices, better mortgage rates, and a clear builder pivot toward smaller units in counties like Washington and Clackamas. New construction rose 14.5%, and much of that growth came from projects intentionally designed to meet buyer qualification thresholds.

The county distribution remained familiar: Washington County accounted for just over half of all attached‑home sales, Multnomah contributed about a quarter, and Clackamas nearly a fifth. The remaining counties—Yamhill, Columbia, and Hood River—continued to show extremely low volumes, where individual sales can shift averages dramatically and trend analysis is not meaningful.

Taken together, the quarter reflects a market that is re‑calibrating rather than contracting. Prices softened, affordability expanded, and builders adapted quickly to buyer needs.

What trends do you expect to see in Q2 2026? I’d love to hear your thoughts—feel free to reply here or reach out directly.

Sources & Further Reading

All data presented in this quarterly update is sourced directly from RMLS and has been subjected to a rigorous cleaning and validation process to ensure reliability for attached homes residential analysis in the six-county Portland Region. The trends, comparisons, and commentary are the result of original appraisal expertise and independent analysis—not aggregated from secondary sources or news summaries.

- RMLS Data Challenges: Portland Appraisal Blog

- The Portland Region – Six-County Market Area Overview: Portland Appraisal Blog

- Portland Affordability Index – PABAI: A Realistic Housing Qualification Metric for the Portland Region: Portland Appraisal Blog

- HUD Portland-Vancouver-Hillsboro, OR-WA MSA: Median Household Income

- Mortgage Rates & the Portland Region Housing Market: Portland Appraisal Blog

- The 2025 Portland Region Attached Homes Market in Review: Portland Appraisal Blog

- The 2024 Portland Region Attached Housing Market in Review: Portland Appraisal Blog

- External Obsolescence in Hillsboro — Residential Market Response to Intel’s 2024–2025 Workforce Reductions: Portland Appraisal Blog

Coda

Thanks for reading—I hope you found a useful insight or an unexpected nugget along the way. If you enjoyed the post, please consider subscribing for future updates.

Are you an agent in Portland who wonders why appraisers always do “x”?

A homeowner with questions about appraiser methodology?

If so, feel free to reach out—I enjoy connecting with market participants across Portland and the surrounding counties, and am always happy to help where I can.

And if you’re in need of appraisal services in Portland or anywhere in the Portland Region, we’d be glad to assist.